How to Retire Early: The FIRE Movement (Financial Independence; Retire Early)

Imagine waking up at 40 without an alarm clock, free to hike national parks, launch a passion project, or simply sip coffee on your porch— all without worrying about the next paycheck. That's the prom...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine waking up at 40 without an alarm clock, free to hike national parks, launch a passion project, or simply sip coffee on your porch— all without worrying about the next paycheck. That's the promise of the FIRE movement (Financial Independence, Retire Early), a strategy that's helping thousands of Americans ditch the 9-to-5 grind decades ahead of schedule.FIRE isn't about winning the lottery; it's a disciplined path to build wealth aggressively through saving, investing, and smart planning tailored to U.S. realities like 401(k)s, Roth IRAs, and Social Security gaps.

In 2026, with inflation cooling and stock markets rewarding patient investors, more millennials and Gen Zers are embracing FIRE variants like Coast FIRE or Barista FIRE to fit real-life needs. This guide breaks down how to retire early step-by-step, with practical tips, U.S.-specific tools, and pitfalls to avoid. Whether you're starting from scratch or tweaking your portfolio, you'll find actionable steps to launch your FIRE journey today.

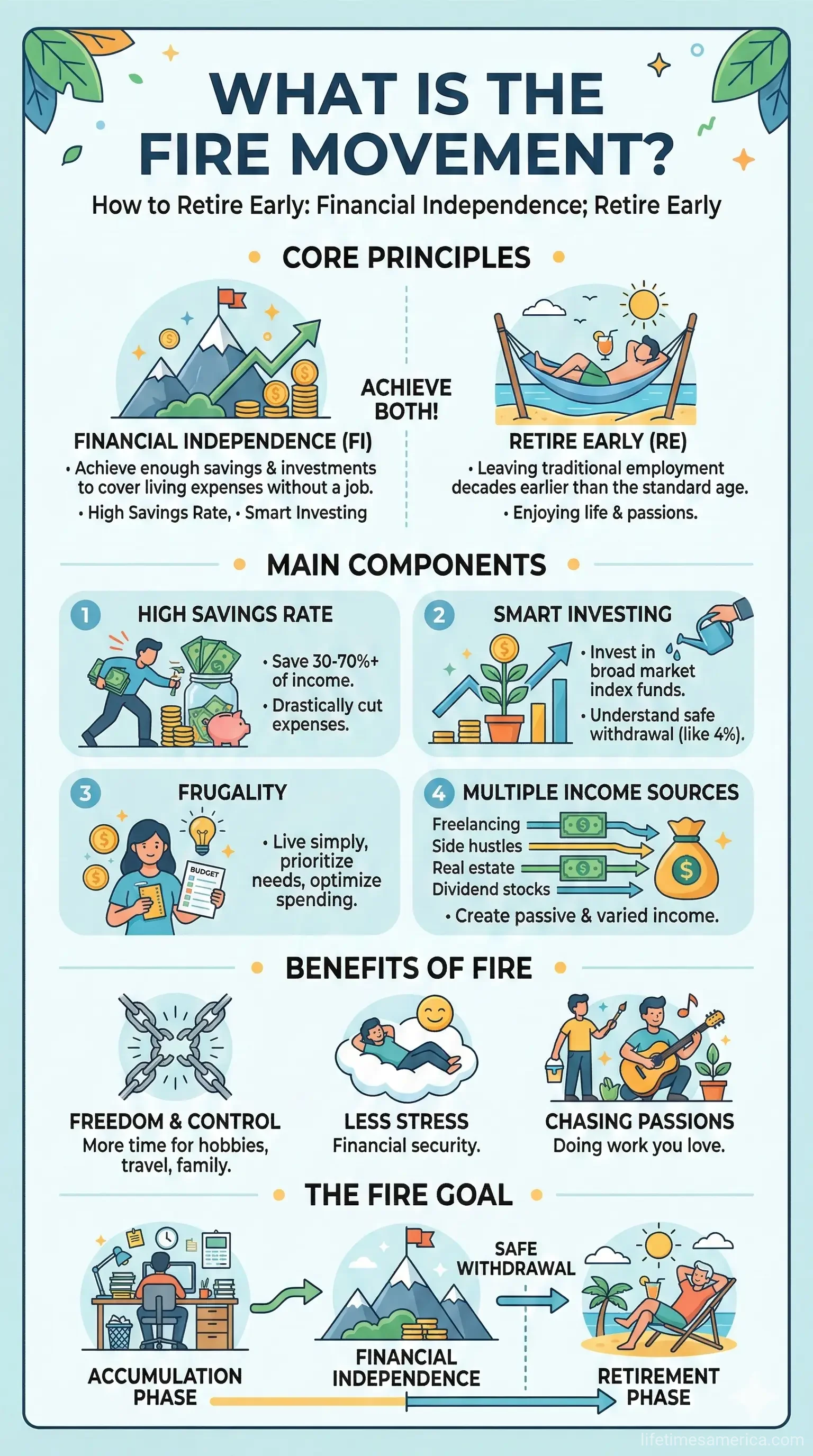

What Is the FIRE Movement?

The FIRE movement, short for Financial Independence, Retire Early, empowers Americans to save and invest so fiercely that their assets generate enough passive income to cover living expenses—often before age 50. Popularized in the 1990s by books like Your Money or Your Life and blogs such as Mr. Money Mustache, FIRE has evolved beyond extreme frugality into flexible lifestyles.

At its core, FIRE splits into two phases: Financial Independence (FI), where investments like index funds or rental properties replace your salary, and Retire Early (RE), where you choose how to spend your time—be it travel, volunteering, or side gigs without financial stress. Unlike traditional retirement tied to Medicare at 65 or Social Security full benefits at 67, FIRE lets you exit the workforce in your 30s, 40s, or 50s.

Types of FIRE for Different Lifestyles

- Classic FIRE: Save 50-70% of income to fully retire ASAP. Ideal for high earners in tech or finance.

- Lean FIRE: Target $1M nest egg for minimalist living under $40K/year.

- Fat FIRE: Build $2.5M+ for comfortable lifestyles over $100K/year.

- Coast FIRE: Save aggressively early, then coast on compound growth while working lightly.

- Barista FIRE: Combine investments with part-time gigs for health insurance pre-Medicare.

These options make FIRE adaptable—Amberly Grant, a mid-30s mom, adjusted her plan for family expenses, proving it's not one-size-fits-all.

Step 1: Calculate Your FIRE Number

Your FIRE number is the savings needed to sustain your lifestyle forever. Use the 4% rule: Multiply annual expenses by 25. If you need $50,000/year post-tax, aim for $1.25 million. Vanguard notes this assumes a 30-year retirement, but FIRE often spans 50+ years, so adjust to 3-3.5% for safety (e.g., $1.67M for $50K).

Practical Calculation Tools

- Track expenses for 3 months using apps like Mint or YNAB to find your "FI number" baseline.

- Factor U.S. costs: Housing (30% of budget), healthcare ($300/month pre-Medicare), taxes on withdrawals.

- Use online calculators from Vanguard or IRS.gov for Roth/401(k) projections.

Pro tip: Build in guardrails—cut spending if markets dip, or boost withdrawals in bull markets.

Step 2: Boost Savings to 50%+ of Income

FIRE demands aggressive saving: 50% or more of net income, far above the typical 10-15% for traditional retirement. Start by slashing housing (under 25% income), ditching new cars, and meal-prepping.

U.S.-Specific Savings Hacks

- Max 401(k) to $23,500 (2026 limit) + employer match—free money!

- Fund Roth IRA ($7,000 limit) for tax-free growth; ideal for early withdrawals penalty-free after 59½.

- Use HSA ($4,150 individual limit) for pre-Medicare healthcare—triple tax-advantaged.

- Side hustles: Drive Uber, freelance on Upwork, or rent space on Airbnb to hit 50%+ savings.

A $80K earner saving $40K/year at 7% returns could hit $1M in 17 years. Track progress quarterly.

Step 3: Invest Like a FIRE Pro

Invest savings in low-cost index funds (Vanguard VTI, expense ratio 0.03%) for broad market exposure. The "order of operations": Debt payoff first (except low-rate mortgages), then emergency fund (6-12 months), taxable brokerage, then real estate.

Top FIRE Investments for 2026

| Asset | Why It Works for FIRE | U.S. Example |

|---|---|---|

| Index Funds/ETFs | Historical 7-10% returns; passive. | Vanguard S&P 500 (VOO) |

| Rental Properties | Cash flow + appreciation; tax deductions. | Roofstock for turnkey homes |

| Dividend Stocks | Passive income streams. | Schwab U.S. Dividend Equity ETF (SCHD) |

| REITs | Real estate without management. | Vanguard REIT ETF (VNQ) |

Diversify: 60-80% stocks early, shift conservative near retirement. Avoid high-fee advisors unless complex.

Step 4: Tackle Healthcare and Taxes

Pre-65 healthcare is FIRE's biggest hurdle—expect $10K+/year without employer coverage. Options: Marketplace plans (ACA subsidies if income low), spouse's plan, or mini-med via part-time work.

Taxes: Roth conversions ladder to fill low brackets pre-Social Security. IRS Rule 72(t) allows penalty-free 401(k)/IRA access via SEPP. Claim credits like Saver's Credit (up to $1,000) on irs.gov.

Pros, Cons, and Pitfalls

Pros: Time freedom, reduced anxiety from fat portfolios, pursuit of passions.

Cons: Market crashes, sequence risk, boredom, or family changes like kids' college (use 529 plans).

Avoid: Lifestyle creep, high-interest debt, or solo planning—consult a CFP® for personalized advice.

Your Next Steps to FIRE

Start today: Calculate your number, audit expenses, max tax-advantaged accounts, and invest weekly. Join communities like Reddit's r/financialindependence or ChooseFI podcast for motivation. Track milestones—$100K saved, 25% FI—and celebrate. With discipline, you'll trade golden handcuffs for true freedom. Your early retirement awaits—let's make 2026 your launch year.

Frequently Asked Questions

Sources & References

-

1

How to Achieve FIRE: Financial Independence, Retire Early in 2026 — www.mintos.com

-

2

The FIRE movement: Making early retirement an achievable goal — www.plantemoran.com

-

3

The FIRE Movement: Guidance for CFP®s — www.bostonifi.com

-

4

Millennials on their way to early retirement share the formulas they... — www.businessinsider.com

-

5

The Ultimate Guide to FIRE in 2026 (Step-by-Step) - YouTube — www.youtube.com

-

6

Fire investing & the 4% rule for early retirement - Vanguard — investor.vanguard.com

-

7

The Final Countdown to Retire Early in 2026: A Monthly Guide — www.kiplinger.com