What Is the Difference Between a W-2 and a 1099?

Ever received a stack of tax forms at year-end and wondered why some coworkers got a W-2 while you held a 1099-NEC? You're not alone—this distinction shapes everything from your paycheck to your retir...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever received a stack of tax forms at year-end and wondered why some coworkers got a W-2 while you held a 1099-NEC? You're not alone—this distinction shapes everything from your paycheck to your retirement savings, and getting it wrong can cost thousands in penalties. The core difference between a W-2 and a 1099 boils down to employee status versus independent contractor, dictating who handles taxes, benefits, and control over your work.

In 2026, with IRS reporting thresholds rising to $2,000 for most 1099 forms, understanding these forms is more crucial than ever for Americans navigating the gig economy or traditional jobs. Whether you're a freelancer scaling your side hustle, a business owner hiring talent, or an employee eyeing contractor gigs, this guide breaks it down with real-world examples, tax math, and steps to stay compliant.

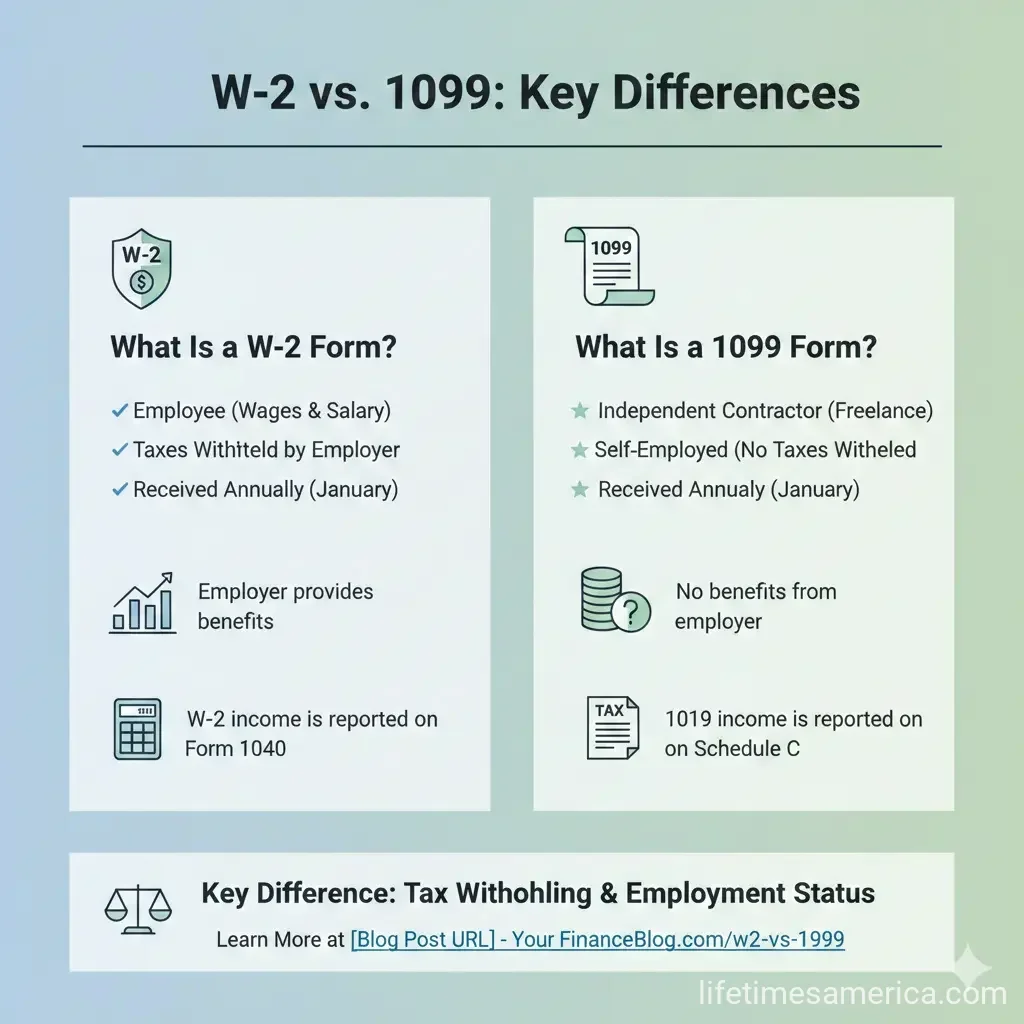

What Is a W-2 Form?

A **W-2 form**, officially Wage and Tax Statement, reports your earnings as an employee to both you and the IRS. Employers issue it by January 31 (or February 2, 2026, for 2025 wages due to weekend shift) for any amount paid—no minimum threshold applies.

It details:

- Taxable wages: Your gross pay minus pre-tax deductions like 401(k) contributions.

- Withheld taxes: Federal, state, local income taxes, plus your share of Social Security (6.2%) and Medicare (1.45%)—totaling 7.65% FICA.

- Employer-paid portions, like their FICA match, though not shown on your copy.

For example, if you earn $100,000 as a W-2 marketing coordinator in California, your employer withholds about $7,650 in FICA (your half), plus income taxes, sending you a W-2 by early February. You use it to file your return, often getting a refund if over-withheld.

Who Gets a W-2?

W-2s go to traditional employees under IRS control: behavioral (you follow their instructions), financial (they provide tools), and relationship (indefinite term, benefits offered). Think full-time office workers, salaried pros, or even part-timers with set schedules.

What Is a 1099 Form?

A **1099 form**—primarily 1099-NEC for non-employee compensation in 2026—reports payments to independent contractors, freelancers, or vendors. No taxes withheld; you're on the hook for everything, including quarterly estimates via Form 1040-ES.

Key 2026 updates:

- Threshold jumps from $600 to $2,000 for 1099-NEC and 1099-MISC (payments after Dec. 31, 2025).

- 1099-K for third-party payments (like Venmo business) rises to $20,000 + 200 transactions.

Clients issue it if you earn $2,000+ in a year. On $100,000 as a 1099 graphic designer, you pay full 15.3% self-employment tax ($15,300), but deduct half ($7,650) on Schedule SE, netting $7,650—still $6,480 more than a W-2 peer after adjustments.

Who Gets a 1099?

Contractors control their methods, use own tools, work project-based, and handle business expenses. Examples: Uber drivers, consultants, or one-off web developers.

Key Differences: W-2 vs. 1099 Side-by-Side

Here's a clear comparison for 2026:

| Factor | W-2 Employee | 1099 Contractor |

|---|---|---|

| Tax Withholding | Employer withholds income, FICA (7.65% split) | None—you pay quarterly + full 15.3% SE tax |

| Cost to Employer | Salary + 20-30% (FICA match 7.65%, FUTA/SUTA, benefits) | Just the fee (20-30% savings) |

| Benefits | Health insurance, 401(k), paid leave (often) | None—buy your own |

| Control | Employer directs how/when/where | You decide methods, schedule |

| Flexibility | Fixed role, long-term | Project-based, scale as needed |

| Legal Protections | FLSA overtime, unemployment, workers' comp | Limited—own insurance needed |

| Tax Deductions | Standard/itemized + 401(k) | Schedule C: home office, mileage (67¢/mile 2026 est.), supplies |

For a $50,000 worker: W-2 costs employer ~$65,000+ (FICA $3,825 + benefits); 1099 is $50,000 flat. Workers: 1099 pays more tax but deducts business costs W-2 can't.

Tax Implications for Workers and Businesses

For Employees (W-2)

Simpler: Taxes auto-withheld, employer matches FICA (Social Security up to $176,100 wage base 2026 est., Medicare unlimited). Eligible for Earned Income Tax Credit, Child Tax Credit. Use W-2 for free file via IRS Direct File or TurboTax.

For Contractors (1099)

Pay quarterly estimates to avoid underpayment penalties (90% prior year or 110% current). Deduct half SE tax, plus business expenses—potentially lowering taxable income below W-2 levels. Track via QuickBooks Self-Employed.

"On $100,000, a 1099 worker pays roughly $7,065 more in employment taxes than a W-2 employee."

For Businesses

W-2: Higher costs but control, loyalty. 1099: Cheaper, flexible—but misclassification risks back taxes, 40% FICA penalties, $1,000+ fines per worker.

IRS Classification Rules: Avoid Misclassification

IRS uses a 3-factor test:

- Behavioral: Does employer control what, how, when?

- Financial: Who bears profit/loss, provides tools?

- Relationship: Benefits, permanency?

Tip: Document contracts clearly. Converting 1099 to W-2? Update payroll, get W-4/I-9, start withholding. Check IRS SS-8 form for ruling.

Pros and Cons: Which Is Right for You?

W-2 Pros

- Steady pay, benefits (e.g., employer-sponsored Medicare supplements pre-65).

- Less tax hassle, unemployment via state like California's EDD.

- Team culture, training.

W-2 Cons

- Less flexibility, income capped.

- Fewer deductions.

1099 Pros

- Set rates, multiple clients, big deductions (e.g., home office $5/sq ft).

- Autonomy, scalability.

1099 Cons

- No safety net—buy health via Marketplace (ACA subsidies possible).

- Higher taxes, irregular income.

Business choice: 1099 for short gigs; W-2 for core roles.

Practical Tips for Americans

- Workers: Save 25-30% of 1099 income for taxes. Use apps like Keeper Tax for deductions.

- Businesses: Use payroll like ADP for W-2 compliance. Track 1099s over $2,000 via IRS FIRE system.

- File on time: W-2 by Feb 2026; 1099 by Jan 31.

- Consult IRS.gov or CPA—this isn't advice; rules vary by state (e.g., CA ABC test stricter).

Next Steps to Stay Compliant

Review your 2025 forms now. Businesses: Audit classifications quarterly. Workers: Set up quarterly payments at IRS.gov/payments. For personalized help, visit IRS.gov/forms or consult a CPA/enrolled agent via NAEA.org. Proper classification saves money and stress—act before April 15!

Disclaimer: This guide uses 2026 rates; tax laws change. Seek professional advice for your situation.

Frequently Asked Questions

Sources & References

- 1

- 2

-

3

1099 vs. W-2 in 2026: Key differences for businesses - QuickBooks — quickbooks.intuit.com — quickbooks.intuit.com

- 4

- 5

-

6

1099 vs W-2: What Business Owners Must Know Before Tax Season ... — gtaaccountinggroup.com — gtaaccountinggroup.com

- 7

-

8

The Difference Between a 1099 and a W-2 Tax Form - TurboTax — turbotax.intuit.com — turbotax.intuit.com

Useful Tools

Related Articles

How to Avoid the "Marriage Penalty" in the 2026 US Tax Code

Imagine tying the knot and then discovering your tax bill just skyrocketed—thousands of dollars higher than if you'd stayed single. That's the harsh reality of the marriage penalty in the US tax code,...

The Best "Side-Hustle" Tax Software for 2026 Filers

Running a side hustle in 2026 means juggling gigs like Uber driving, freelance graphic design, or selling handmade crafts on Etsy while keeping your day job. But come tax time, tracking those 1099-NEC...

How to Use "Tax-Loss Harvesting" to Offset Your 2026 Stock Gains

Imagine locking in hefty stock gains in 2026 only to watch a big chunk vanish to capital gains taxes. What if you could slash that tax bill without derailing your investment strategy? That's the power...

The Gig Economy Tax Guide: How to Deduct Your Car; Internet; and Office

If you're earning money through gig work—whether you're driving for a rideshare company, freelancing, delivering groceries, or running a side hustle—you're probably wondering how to keep more of what...