Personal Loan vs Credit Card: Which Should You Use?

Need cash for a home repair, medical bill, or to consolidate debt? You're not alone—millions of Americans face this choice every year between grabbing their credit card or applying for a personal loan...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Need cash for a home repair, medical bill, or to consolidate debt? You're not alone—millions of Americans face this choice every year between grabbing their credit card or applying for a personal loan. The right pick can save you hundreds in interest and keep your budget on track, but the wrong one might drag you deeper into debt. Let's break down personal loan vs credit card to help you decide what's best for your situation in 2026.

Understanding Personal Loans and Credit Cards

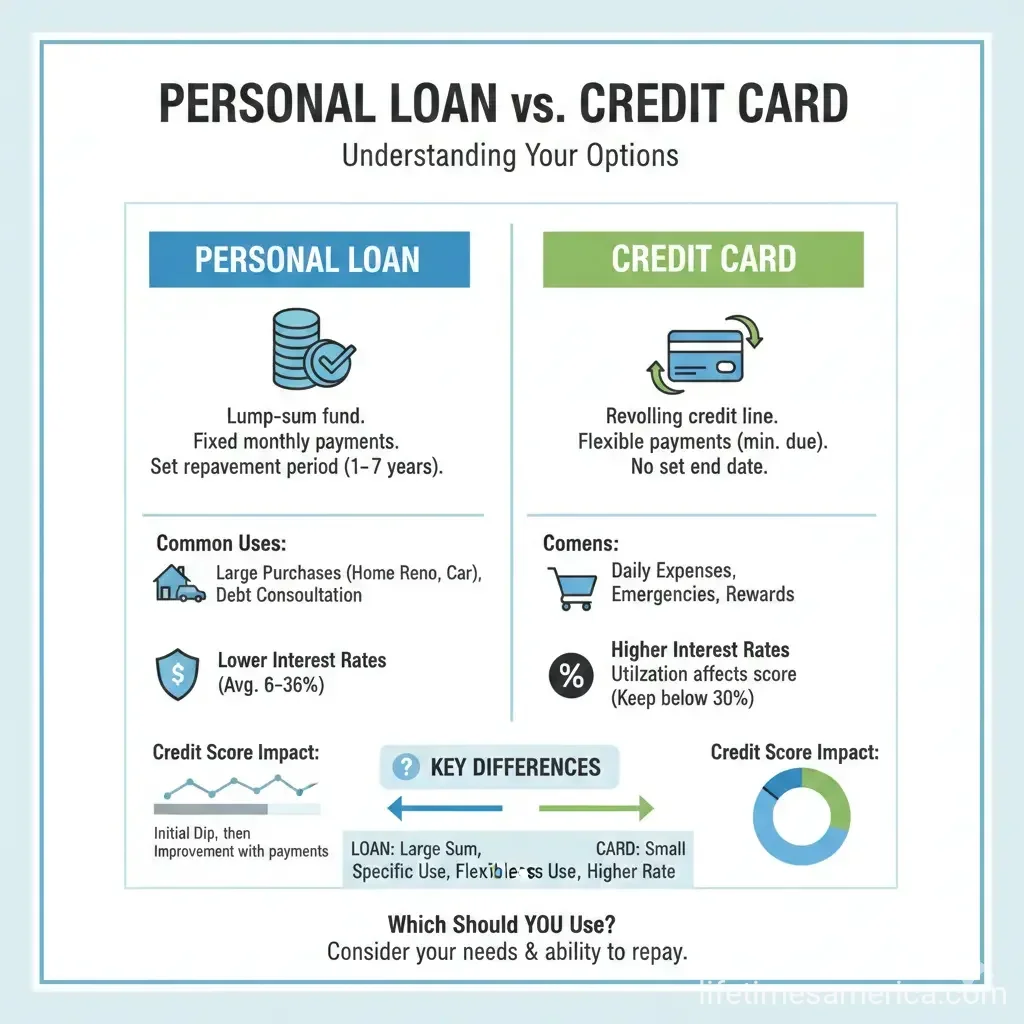

Both options let you borrow money, but they work differently. A personal loan is an installment loan: you get a lump sum upfront and repay it in fixed monthly payments over a set term, usually 1 to 7 years. Credit cards offer revolving credit—you borrow up to a limit, pay it back, and borrow again, with minimum payments due each month.

Key Features of Personal Loans

- Fixed payments: Same amount each month, including principal and interest, for easy budgeting.

- Fixed interest rates: Typically 6% to 36% APR, lower for good credit (mid-600s FICO score or higher).

- Lump sum access: Funds deposited quickly, often same-day from online lenders like SoFi or PenFed Credit Union.

- Higher limits: Up to $100,000, ideal for big expenses.

Key Features of Credit Cards

- Revolving credit: Use as needed up to your limit, perfect for everyday spending.

- Variable rates: Average 20%-25% APR in 2026, but 0% intro offers available if paid off quickly.

- Minimum payments: Flexible but risky—can stretch debt for years with high interest.

- Rewards: Cash back, points, or perks on purchases.

Personal Loan vs Credit Card: Head-to-Head Comparison

Here's how they stack up in a quick table for 2026 borrowing needs:

| Personal Loan | Credit Card | |

|---|---|---|

| Best For | Large one-time purchases, debt consolidation | Small, ongoing expenses |

| Interest Rate | Fixed, avg. 12% (6%-36% range) | Variable, avg. 20%-25% |

| Repayment | Fixed term (1-7 years) | Minimum due, ongoing |

| Funds Access | Lump sum | Revolving line |

| Fees | Origination possible (1-8%) | Annual, late, cash advance |

Interest Rates and Total Costs

Personal loans often win on cost. With average credit card APR at 20%-25%, a $5,000 balance paid at minimums racks up $1,670 in interest over time. Switch to a 12% personal loan, and it's just $979—with a clear end date. Borrowers with strong credit (FICO 670+) snag rates under 10% on loans from lenders like PenFed (6.74%-17.99%).

In 2026, personal loans average 12% interest with payoff in 2-7 years, beating credit cards' high-APR revolving debt.

Impact on Your Credit Score

Both affect your score, but differently. Personal loans diversify your credit mix (installment debt) and shorten credit utilization once paid off. Credit cards hit utilization harder if balances creep up—aim to keep under 30%. Check your free annual credit reports at AnnualCreditReport.com, authorized by federal law.

Pros and Cons of Each Option

Personal Loan Pros and Cons

Pros:

- Lower rates for qualified borrowers

- Predictable payments

- Fast funding for large sums

- Great for debt consolidation

Cons:

- High rates if credit is fair (below mid-600s)

- No flexibility—fixed amount

- Origination fees up to 8%

Credit Card Pros and Cons

Pros:

- Flexible for daily use

- 0% APR promos (12-21 months)

- Rewards and protections (fraud liability $50 max)

- Build credit with on-time payments

Cons:

- High ongoing APR

- Minimum payments prolong debt

- Temptation to overspend

When to Choose a Personal Loan Over a Credit Card

Opt for a personal loan for known, large expenses like $10,000 home repairs or consolidating $15,000 in card debt. If your cards average 23% APR and you qualify for 11% on a loan, you'll save big—especially with fixed payments fitting your budget. In 2026, lenders like MoneyLion offer up to $100,000 at 6.74%-25.99% for terms to 84 months.

Pro tip: Use a loan calculator on sites like Bankrate or NerdWallet to compare your scenario. Prequalify without a hard credit pull to shop rates.

When a Credit Card Makes More Sense

Grab the card for groceries, gas, or emergencies under $1,000 if you pay in full monthly—avoid interest entirely. Rewards cards from Chase or Capital One give 1-5% cash back, turning spending into savings. Grace periods (21-25 days) let you float purchases interest-free.

Watch for balance transfer cards with 0% APR for 15-21 months to tackle debt short-term.

Debt Consolidation: Personal Loans Shine

Americans owe $1.13 trillion in credit card debt in 2026. A personal loan can roll it into one lower-rate payment. Example: $5,000 at 20% card APR vs. 12% loan saves $691 in interest. Ensure your debt-to-income ratio stays under 36% for approval—calculate at ConsumerFinance.gov.

Practical Tips for Americans in 2026

- Check your credit: Free weekly reports at AnnualCreditReport.com. Boost score by paying down utilization.

- Compare rates: Prequalify with LendingTree or Credible for multiple offers.

- Avoid fees: Skip cash advances (25-30% APR); choose no-fee loans.

- Budget first: Use 50/30/20 rule—needs, wants, savings/debt.

- Seek help if needed: Non-profits like NFCC.org for credit counseling; avoid payday loans.

Federal protections under the CARD Act cap fees and require clear terms. Report issues to CFPB.gov.

Next Steps to Decide: Personal Loan vs Credit Card

Crunch your numbers: List expenses, rates, and payments. Prequalify for a personal loan today if consolidating or funding big buys—many approve in minutes. For flexibility, pick a rewards card but pay fully. Track spending with apps like Mint. Build emergency savings (3-6 months expenses) to borrow less. Your choice shapes your financial future—choose wisely for less stress and more control.

Frequently Asked Questions

Sources & References

- 1

-

2

Personal Loan vs. Credit Card: When Each Is Best — nerdwallet.com — www.nerdwallet.com

- 3

- 4

-

5

When should you use a personal loan vs. a credit card? — oldnational.com — www.oldnational.com

-

6

Comparing Personal Loans & Credit Cards — theabcbank.com — theabcbank.com

Useful Tools

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...