How Much House Can You Afford? The Rules Explained

Ever dreamed of finding the perfect home, only to wonder if your budget can stretch that far? You're not alone—figuring out how much house you can afford is one of the biggest questions for American h...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever dreamed of finding the perfect home, only to wonder if your budget can stretch that far? You're not alone—figuring out how much house you can afford is one of the biggest questions for American homebuyers in 2026. With mortgage rates fluctuating and home prices varying by city, understanding the rules like the classic 28/36 guideline can help you shop confidently without overextending your finances.

This guide breaks down the key rules, calculators, and real-world examples tailored for U.S. households. Whether you're a first-time buyer in Detroit or a growing family in Cincinnati, you'll walk away with actionable steps to determine your ideal home price.

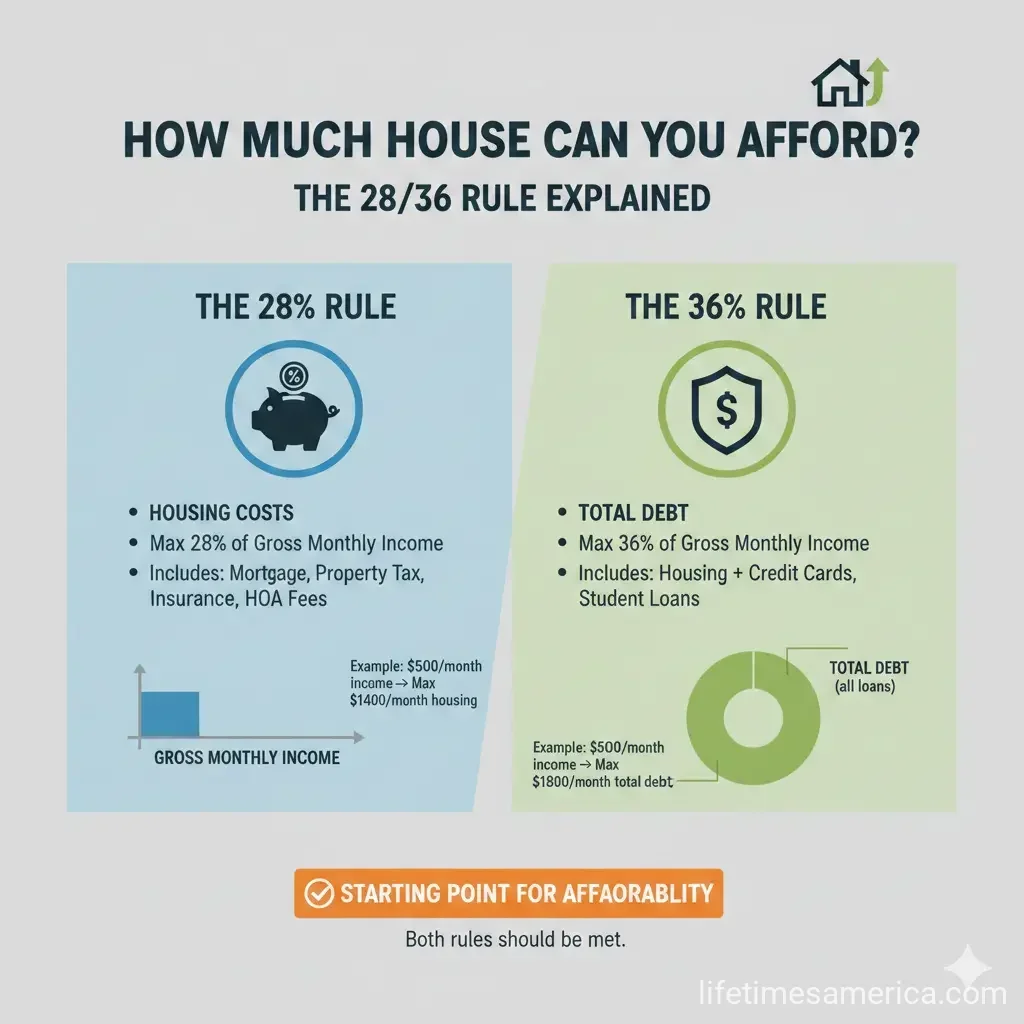

The 28/36 Rule: Your Starting Point for Affordability

The 28/36 rule is a time-tested benchmark used by lenders and financial experts to gauge housing affordability. It suggests you shouldn't spend more than 28% of your gross monthly income on housing costs—like your mortgage principal, interest, property taxes, homeowners insurance, and HOA fees—and no more than 36% on total debt payments, including housing plus credit cards, car loans, and student debt.

For example, if your household earns $5,500 monthly before taxes, your housing budget caps at $1,540 (5,500 x 0.28). Total debt, including that housing payment, shouldn't exceed $1,980 (5,500 x 0.36). Lenders often use a slightly stricter version, like 36/43, where housing is 36% and total debt is 43% of gross income.

Why This Rule Matters in 2026

With average 30-year fixed mortgage rates hovering around 6.5-7.5% this year, the 28/36 rule keeps you from biting off more than you can chew. It accounts for not just the mortgage but ongoing costs that eat into your paycheck. Sticking to it helps avoid the trap of qualifying for a big loan but struggling with everyday expenses like groceries or retirement savings into a 401(k).

Key Factors That Determine How Much House You Can Afford

Beyond the rules, several variables shape your buying power. Online calculators from trusted sources like Rocket Mortgage, Zillow, and NerdWallet factor these in for personalized estimates.

Your Income and Debt-to-Income Ratio (DTI)

Gross monthly income is the foundation. Lenders divide your debts by income to get your DTI—a key metric. Aim for under 36% housing DTI and 43% total DTI for the best rates. On a $100,000 annual salary ($8,333 monthly), you might afford a $277,742 home with a 15% down payment.

- Higher income equals more house: $200K salary? Up to $630,709.

- DTI tip: Pay down debts first to lower your ratio and boost borrowing power.

Down Payment and Interest Rates

A bigger down payment reduces your loan amount and monthly payments. For a $300,000 home:

| Down Payment % | Amount | Monthly Payment (at ~6.5% rate) |

|---|---|---|

| 20% | $60,000 | $1,179 |

| 10% | $30,000 | $1,327 |

| 5% | $15,000 | $1,401 |

| 0% | $0 | $1,474 |

Interest rates amplify this: At 7.5% vs. 6.5%, a $50,000 income buyer might afford $186,800 instead of $209,500 with $1,167 max payment. Shop around—rates can vary by credit score and lender.

Property Taxes, Insurance, and Location

These "PITI" costs (principal, interest, taxes, insurance) add up. In affordable spots like Oklahoma City, a 28% DTI buys $230,466; in Birmingham, AL, it's $247,509. Use local estimates: Expect 1-2% of home value annually for taxes in most states.

Credit Score and Loan Type

A score above 740 unlocks the lowest rates. FHA loans allow DTIs up to 50% for qualified buyers, while conventional caps at 43-50%. Wells Fargo emphasizes verifying income, assets, credit, and property value.

Home Affordability Calculators: Get Your Custom Number

Don't guess—plug your numbers into free tools. Rocket Mortgage's calculator uses DTI starting at 36% and adjusts for rates and down payments. Zillow tailors by location and debts. Fannie Mae and Freddie Mac offer official versions aligned with U.S. lending standards.

Quick examples for 2026 incomes:

| Annual Salary | Gross Monthly | Est. Home Price (15% down) |

|---|---|---|

| $90K | $7,500 | $245,983 |

| $300K | $25,000 | $986,203 |

| $500K | $41,666 | $1,697,190 |

Chase and NerdWallet let you reverse-engineer: Input desired payment to see required income.

Real-World Examples: How Much House on Common U.S. Salaries

Let's apply the rules. For a $60,000 household income ($5,000 monthly):

- 28% housing: $1,400 max PITI.

- At 6.5% rate, 10% down: Around $250,000 home.

On $40,000 ($3,333 monthly): Housing cap at $933, pointing to $150,000-$200,000 homes depending on location and debts.

In high-cost areas, stretch wisely—Detroit buyers at 28% DTI afford $248,126. Always factor closing costs (2-5% of price) and reserves for repairs.

Practical Tips to Maximize Your Buying Power

- Boost your down payment: Save in a high-yield account or use FHA (3.5% min).

- Improve credit: Pay debts on time; aim for under 30% utilization.

- Shop multiple lenders: Prequalify with no credit hit via Wells Fargo or Chase tools.

- Consider loan terms: 15-year saves interest but raises payments ($2,255 vs. $1,474 on $300K).

- Budget for extras: Maintenance (1% of home value/year), utilities, and emergencies.

"Using a percentage of your income can help determine how much house you can afford."

Next Steps to Buy Your Dream Home

Run the numbers today with a calculator, then get prequalified. Talk to a lender about 2026 programs like FHA or conventional loans. Track your credit via AnnualCreditReport.com and save aggressively. By following the 28/36 rule and these tips, you'll confidently know how much house you can afford—and land a home that fits your life.

Frequently Asked Questions

Sources & References

-

1

Rocket Mortgage: Home Affordability Calculator — www.rocketmortgage.com

-

2

Zillow: Affordability Calculator - How Much House Can I Afford? — www.zillow.com

-

3

NerdWallet: How Much House Can I Afford? Affordability Calculator — www.nerdwallet.com

-

4

Chase: Mortgage Affordability Calculator — www.chase.com

-

5

Wells Fargo: How Much House Can I Afford Calculator — www.wellsfargo.com

-

6

Redfin: How Much House Can I Afford? — www.redfin.com

-

7

Fannie Mae: Mortgage Affordability Calculator — yourhome.fanniemae.com

-

8

Freddie Mac: Homebuying Budget Calculator — myhome.freddiemac.com

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...