The Best 529 Plans for Your Child’s Future College Education

Imagine watching your child open that college acceptance letter, knowing you've already set them up for success without the crushing weight of student debt. That's the power of a 529 plan—a tax-advant...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine watching your child open that college acceptance letter, knowing you've already set them up for success without the crushing weight of student debt. That's the power of a 529 plan—a tax-advantaged savings tool designed specifically for education expenses. As college costs continue to climb, with average in-state public tuition hitting $11,610 for the 2025-2026 academic year, starting early with the right 529 plan can make all the difference for American families.

In this guide, we'll break down the best 529 plans for your child’s future college education, drawing from top 2026 ratings by Morningstar and other experts. Whether you're a Utah resident chasing tax credits or a New Yorker seeking low fees, you'll find actionable advice tailored to U.S. savers. Let's dive in and find the plan that fits your family's goals.

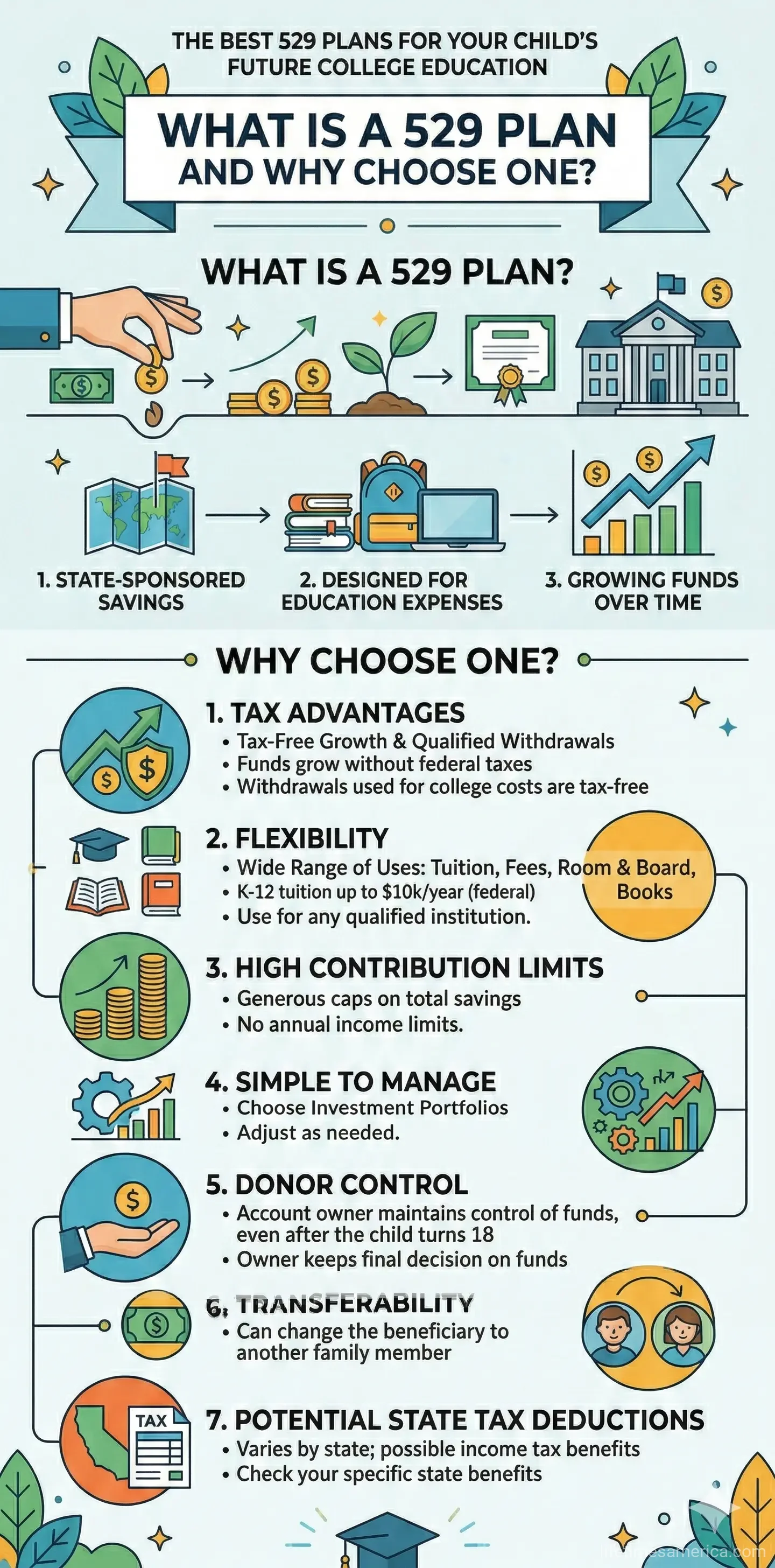

What Is a 529 Plan and Why Choose One?

A 529 plan is a state-sponsored investment account that grows tax-free when used for qualified education expenses like tuition, books, and even up to $10,000 in K-12 tuition or student loan repayments under federal rules. Earnings are exempt from federal income tax, and most states offer additional tax breaks.

Unlike a 401(k) or IRA, 529 plans have high contribution limits—often over $500,000 per beneficiary—and no income restrictions. You can open a plan in any state, regardless of residency, making it flexible for military families or those who move. In 2026, with inflation pushing education costs higher, these plans remain a cornerstone of college funding, as noted by financial experts.

Key Benefits for American Families

- Tax advantages: Federal tax-free growth; 35+ states offer deductions or credits for contributions.

- Control: You stay the owner, even after your child turns 18.

- Flexibility: Use for college, trade schools, or apprenticeships nationwide.

- Gift tax perks: Contribute up to $19,000 per person ($38,000 for couples) in 2026 without triggering gift taxes, or front-load five years' worth.

Types of 529 Plans: Savings vs. Prepaid

There are two main types: savings plans (investment-based, most popular) and prepaid tuition plans (lock in today's rates). Savings plans dominate due to portability—funds work at any eligible school. Prepaid options suit in-state public college attendees.

Direct-Sold vs. Adviser-Sold Savings Plans

- Direct-sold: No sales fees; manage yourself online. Ideal for hands-on parents.

- Adviser-sold: Higher fees but professional guidance. Best if you want personalized advice.

The Best 529 Plans for 2026: Top-Rated Picks

Morningstar's November 2025 report (still guiding 2026 choices) awarded Gold ratings to five direct-sold plans for their low costs, strong management, and performance. Bankrate and SmartAsset echo these, prioritizing fees under 0.15%, proven funds from Vanguard and Fidelity, and state perks. Here's our roundup of the best 529 plans.

Gold-Rated Direct-Sold Standouts

These five shine for everyday Americans saving for college.

- Utah's my529: Perennial leader with ultra-low fees (as low as 0.10%), Vanguard index funds, and customizable portfolios. Utah residents get a 4.55% tax credit up to limits; $574,000 max balance. No minimum to start.

- Illinois' Bright Start Direct-Sold: Upgraded to Gold in 2025 for diverse, low-cost index options and top management. Fees around 0.09%; strong age-based tracks that shift conservative as college nears.

- Alaska's T. Rowe Price College Savings Plan: Actively managed by T. Rowe Price pros; excels in long-term growth. Low fees and robust research backing.

- Massachusetts' U.Fund: Fidelity-managed with rock-bottom index funds (fees ~0.07%). Age-based options auto-adjust risk.

- Pennsylvania's PA 529 Investment Plan: Vanguard passive funds at minimal cost. Excellent for buy-and-hold savers.

Top Silver-Rated and Other Strong Contenders

For adviser-sold or state-specific perks:

- Ohio's CollegeAdvantage (direct and adviser versions): BlackRock funds, low fees, and Ohio tax deduction up to $4,000.

- New York's Direct Plan: Solid performance, no minimums, New York deduction up to $5,000 single/$10,000 joint.

- Wisconsin's Edvest: TIAA-CREF and Vanguard funds; Wisconsin deduction up to $5,130 (2025, similar for 2026).

- West Virginia's Smart529 WV Direct: Lowest fees with Vanguard/Invesco; uncapped WV deduction.

- California's ScholarShare 529: TIAA-CREF management, $529,000 limit, 4.5/5 performance rating despite no CA tax break.

- Michigan Education Savings Program: Silver-rated, $500,000 limit, $10,000 annual MI deduction.

Best Prepaid 529 Plans

Lock in tuition rates if betting on in-state publics:

- Florida Prepaid: Flexible for in/out-of-state; popular and guaranteed.

- Massachusetts U.Plan: Covers tuition/fees at MA schools; tax perks.

- Michigan Education Trust (MET): Contract-based for MI publics.

- Nevada Prepaid: Statewide coverage.

| Plan | State Tax Benefit | Best For |

|---|---|---|

| Florida Prepaid | No | Flexible use |

| MA U.Plan | Yes | MA schools |

| MI MET | Yes | MI publics |

| NV Prepaid | No | NV residents |

How to Choose the Best 529 Plan for Your Family

Don't pick based on your state alone—many offer no residency perks. Prioritize:

- Fees: Aim under 0.15% expense ratio.

- Performance: Check Morningstar ratings and 5-10 year returns.

- Investments: Age-based tracks auto-shift from stocks to bonds.

- State taxes: Deductions/credits add 3-5% effective return. Use SavingforCollege.com comparator.

- Minimums/limits: Most have $0 minimum, $300K-$500K+ max.

Pro tip: You can roll over to a better plan once every 12 months tax-free. Non-residents: Utah or NY often win for pure quality.

Practical Steps to Open and Maximize Your 529 Plan

Getting started takes 15 minutes online.

- Compare plans at CollegeSavings.org.

- Open via state site (e.g., my529.org for Utah).

- Fund via bank transfer, payroll, or UGMA/UTMA rollover.

- Automate contributions: $100/month grows to $20K+ in 18 years at 6% return.

- Match employer 529 programs if offered.

For 2026, watch SECURE 2.0 expansions allowing Roth IRA rollovers of unused funds after 15 years. Consult IRS Publication 970 for qualified expenses.

Start Building Your Child's Future Today

The best 529 plans like Utah's my529 or Illinois' Bright Start offer low-cost paths to tax-free college savings. Pick one matching your risk tolerance and tax situation, fund consistently, and watch your investment compound. Open an account this week—your future college grad will thank you. Visit your top plan's site or CollegeSavings.org to compare and enroll now.

Frequently Asked Questions

Sources & References

-

1

Best 529 Plans of 2026 - Kiplinger — www.kiplinger.com

-

2

5 Best 529 Plans To Help Save For College | Bankrate — www.bankrate.com

-

3

10 Best 529 Plans for 2026 and Beyond - SmartAsset — smartasset.com

-

4

The Best 529 Plans for 2025 | Morningstar — www.morningstar.com

-

5

529 Plans by State: Benefits of a College Savings Plan - NerdWallet — www.nerdwallet.com