The Ultimate Guide to 401(k) vs. Roth IRA: Which is Better for You?

Planning for retirement can feel overwhelming, but choosing between a 401(k) and a Roth IRA is one of the smartest moves you can make as an American saver. Both offer tax-free growth and withdrawals i...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Planning for retirement can feel overwhelming, but choosing between a 401(k) and a Roth IRA is one of the smartest moves you can make as an American saver. Both offer tax-free growth and withdrawals in retirement, yet they differ in key ways that could determine thousands in your future nest egg—let's break it down to find the best fit for your situation.

Understanding the Basics: 401(k) vs. Roth IRA

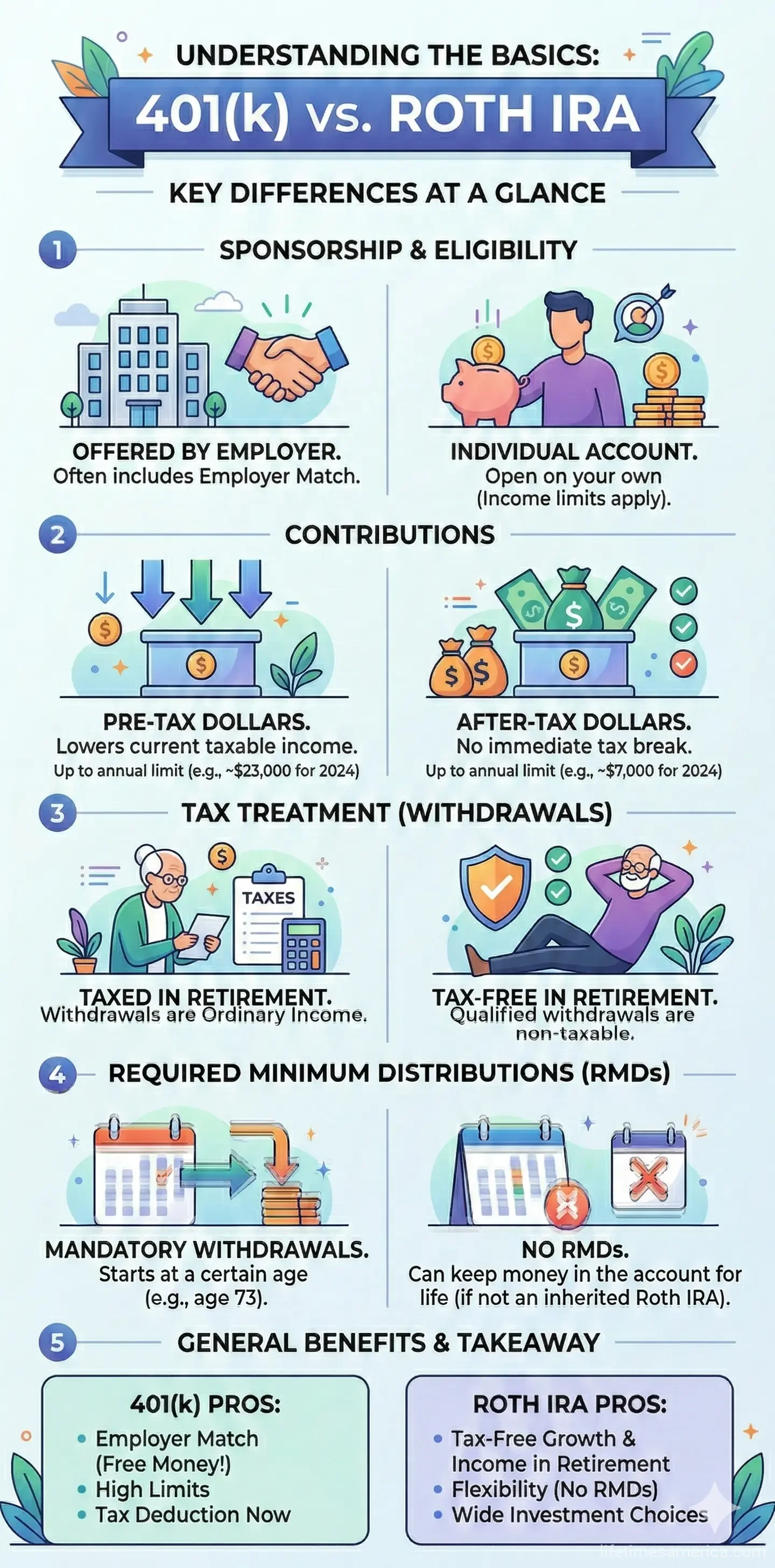

Traditional 401(k)s and Roth IRAs serve as cornerstones of U.S. retirement savings, but they handle taxes differently. A 401(k) lets you contribute pre-tax dollars, reducing your taxable income now, with taxes due on withdrawals later. In contrast, a Roth IRA uses after-tax dollars upfront, allowing tax-free qualified withdrawals in retirement. This fundamental difference makes the choice hinge on your current tax bracket versus your expected one in retirement.

Employer-sponsored 401(k)s often include matching contributions—free money you shouldn't ignore—while Roth IRAs are individual accounts you open yourself through brokers like Fidelity or Vanguard. Both grow tax-deferred, but Roth accounts shine for tax-free income later, especially if rates rise or Social Security gets taxed more heavily.

Who Qualifies? Eligibility Rules

Anyone with earned income can open a Roth IRA, but income limits apply. For 2026, full contributions phase out at modified adjusted gross income (MAGI) of $153,000 for singles and $242,000 for joint filers. High earners can use a backdoor Roth strategy: contribute to a traditional IRA and convert it.

401(k)s are available through your employer—no income limits. If your plan offers a Roth 401(k) option, you can contribute after-tax dollars directly, regardless of earnings.

Contribution Limits and Catch-Ups in 2026

One major edge for 401(k)s is higher limits. In 2026, you can contribute up to $24,500 to a 401(k) if under 50, far exceeding the Roth IRA's $7,500 cap. Age 50+ get catch-ups: $8,000 for 401(k)s (total $32,500), boosting to $11,250 for ages 60-63 (total $35,750).

Roth IRA catch-up is modest: $1,100 extra for 50+, totaling $8,600. Remember, IRA limits are shared across all your IRAs, while 401(k) is per plan. Employer matches don't count toward your limit but raise the total plan cap to $72,000.

Practical Tip: Maximize Both

- First, contribute enough to your 401(k) to get the full employer match—it's essentially a 50-100% immediate return.

- Then, fund your Roth IRA up to its limit for flexibility.

- Finally, add more to your Roth 401(k) if available.

Tax Treatment: Pay Now or Later?

With a traditional 401(k), contributions lower your 2026 taxable income—vital if you're in the 24% bracket. Withdrawals are taxed as ordinary income, potentially at 22% or higher in retirement. Roth IRA contributions don't deduct now, but qualified withdrawals (after age 59½ and 5-year holding) are entirely tax-free, ideal if you expect higher taxes later or want to leave tax-free inheritance.

Both allow tax-free growth, but Roths protect against future IRS hikes. Starting 2026, high earners (prior-year wages over $145,000, inflation-adjusted) must make 401(k) catch-ups as Roth contributions in most plans.

Withdrawals, RMDs, and Early Access

Roth IRAs offer ultimate flexibility: withdraw contributions anytime tax- and penalty-free. Earnings need age 59½ and 5 years. No required minimum distributions (RMDs) in your lifetime—perfect for legacy planning.

Traditional 401(k)s impose 10% penalty plus taxes on early withdrawals before 59½, unless you're 55+ and separated from your employer (Rule of 55). RMDs start at age 73, but Roth 401(k)s now match Roth IRAs: no lifetime RMDs since 2024.

Early Withdrawal Comparison

| Feature | 401(k) | Roth IRA |

|---|---|---|

| Contributions Access | Penalty + taxes (pre-59½) | Tax/penalty-free anytime |

| Rule of 55 | Penalty-free if job separation | N/A |

| RMDs | Age 73 (traditional); None (Roth) | None |

Investment Options and Fees

401(k)s limit you to your plan's menu—often 10-20 funds—with potentially higher fees (0.5-1%). Roth IRAs give full control: stocks, ETFs, bonds via any brokerage, often at rock-bottom costs (e.g., Vanguard's 0.03% expense ratios).

Check your 401(k)'s expense ratio via your plan administrator or tools on irs.gov. Low fees compound hugely: 1% saved yearly adds 20%+ to your balance over 30 years.

Employer Match: The Game-Changer

Up to 6% match is common—e.g., $1,200 free on $20,000 salary. Matches go into traditional 401(k), even if you choose Roth. No Roth IRA equivalent, so prioritize 401(k) first.

Which is Better for You? Scenarios

Choose 401(k) if:

- You get an employer match.

- High current tax bracket (e.g., 32%).

- Want to save more than $7,500/year.

- No Roth IRA income eligibility.

Choose Roth IRA if:

- Low current bracket (12-22%), expecting rise.

- Want investment freedom and low fees.

- Plan tax-free inheritance (no RMDs).

- Need contribution access flexibility.

Many do both: 401(k) for match and volume, Roth IRA for diversification. Use IRS calculators at irs.gov/retirement-plans to model scenarios.

Next Steps to Supercharge Your Retirement

Review your paystub—boost 401(k) to match max today. Open a Roth IRA at fidelity.com or schwab.com if eligible. Use free tools: IRS withholding estimator (irs.gov) and SSA's quick calculator (ssa.gov). Reassess yearly as limits rise and life changes. You're building wealth that lasts generations—start now for tax-smart freedom tomorrow.

Frequently Asked Questions

Sources & References

-

1

Roth IRA vs. Roth 401(k): A Comprehensive Comparison for 2026 — abaretirement.com

-

2

Roth 401(k) vs. Roth IRA — www.schwab.com

-

3

Roth 401(k) vs Roth IRA: A Comparison — www.nerdwallet.com

-

4

Roth 401(k) vs. Roth IRA: Which is right for you? — www.fidelity.com

-

5

Roth IRA vs. 401(k): What's the difference? — www.fidelity.com

-

6

401(k) vs Roth IRA: A Retirement Savings Guide — www.guideline.com

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...