The 50/30/20 Budget Rule Explained for Americans

Struggling to make your paycheck stretch further in today's economy? The 50/30/20 budget rule offers a straightforward path to financial control, helping Americans balance essentials, fun, and future...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Struggling to make your paycheck stretch further in today's economy? The 50/30/20 budget rule offers a straightforward path to financial control, helping Americans balance essentials, fun, and future security without complex spreadsheets.

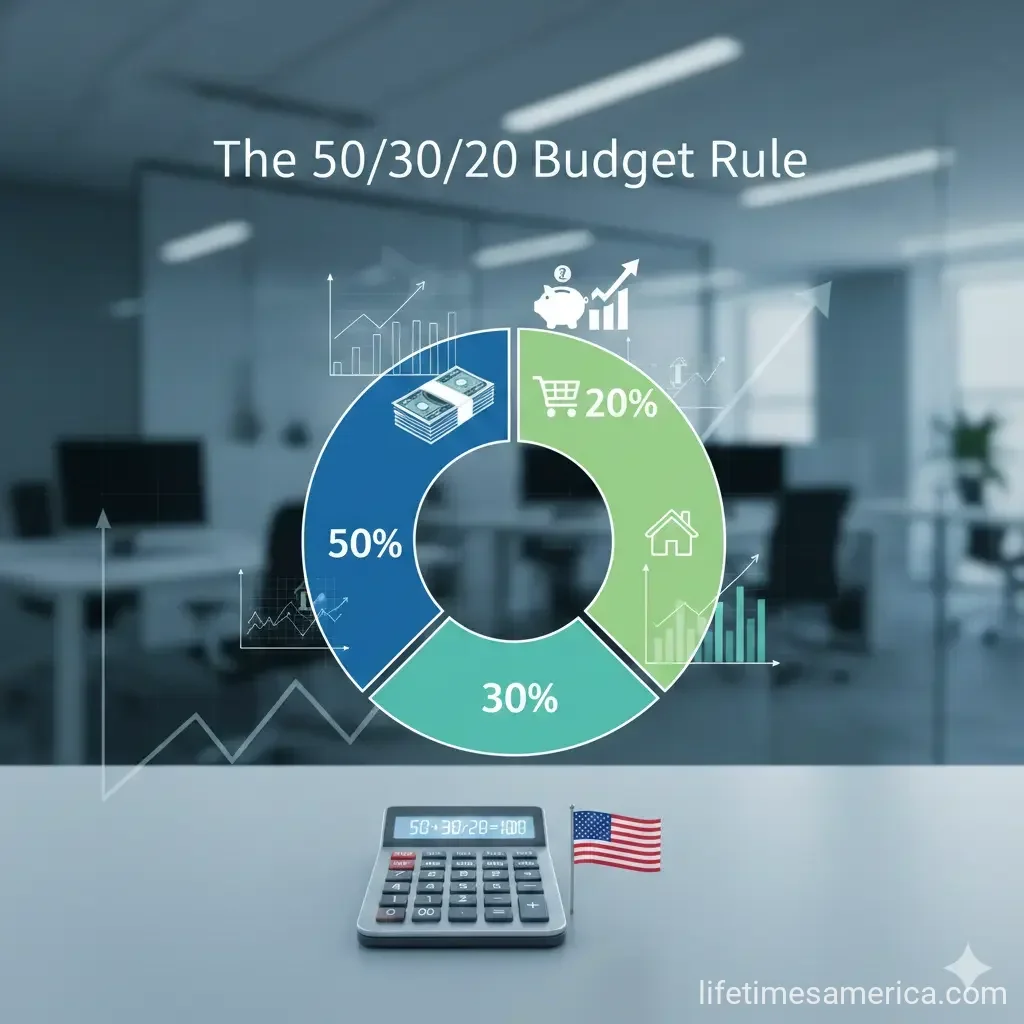

Popularized by financial experts, this rule divides your after-tax income into three simple buckets: 50% for needs, 30% for wants, and 20% for savings and debt payoff. It's flexible, beginner-friendly, and adaptable to rising costs like housing and groceries in 2026. Whether you're in a high-cost city or saving for retirement, let's break it down with real-world U.S. examples.

What Is the 50/30/20 Budget Rule?

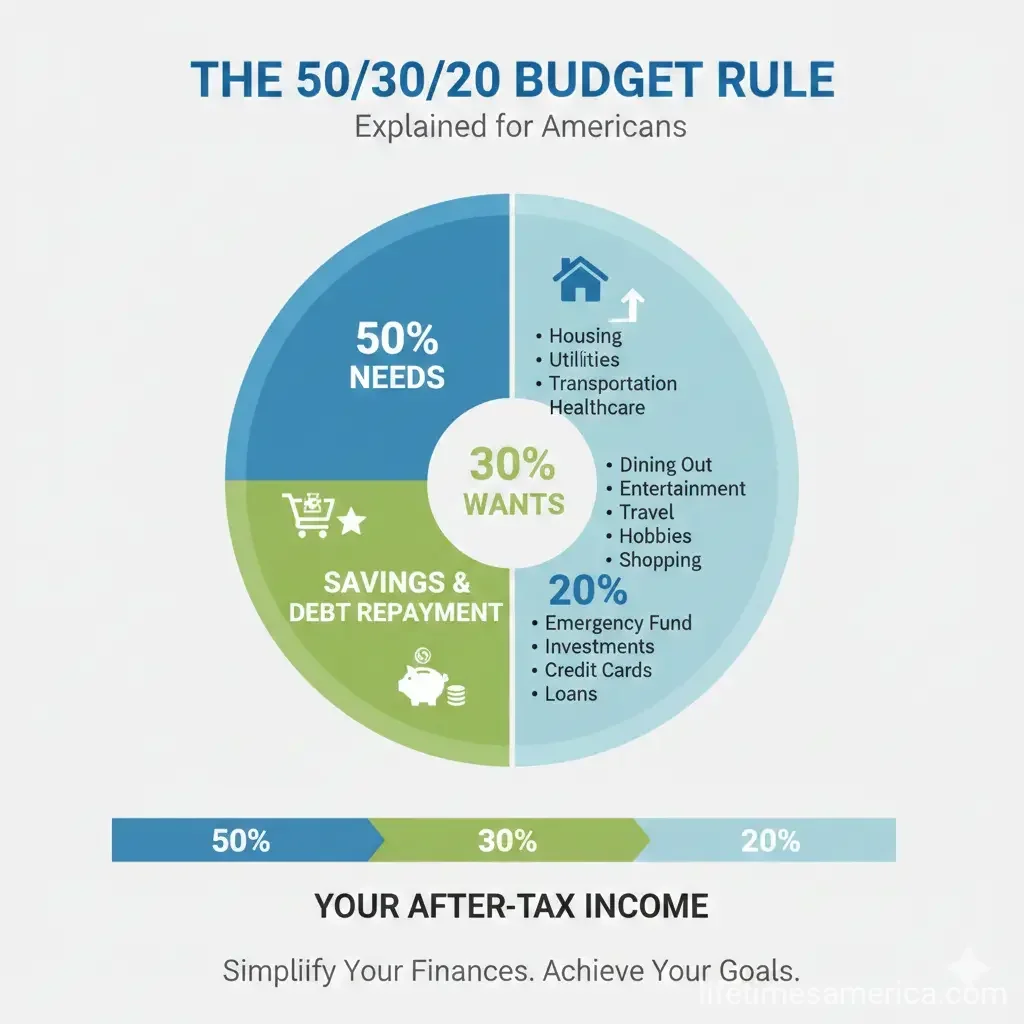

The 50/30/20 budget rule is a percentage-based framework that categorizes your monthly take-home pay—after federal, state, and local taxes but before other deductions like 401(k) contributions or health premiums. Here's the breakdown:

- 50% on needs: Must-have expenses to keep your life running.

- 30% on wants: Discretionary spending for enjoyment and lifestyle.

- 20% on savings and debt: Building wealth and financial freedom.

This approach prioritizes balance over restriction, making it ideal for Americans facing inflation pressures. Unlike zero-based budgets, it doesn't require tracking every penny—just broad category awareness.

Why It Works for Americans in 2026

With median household income around $74,580 annually (about $4,700 monthly after taxes for many), the rule scales easily. It aligns with U.S. financial goals like funding 401(k)s, paying student loans, or building emergency funds amid economic shifts.

Breaking Down the Categories

Needs: 50% of Your Take-Home Pay

Needs are non-negotiables—expenses you'd face severe consequences for skipping. Aim to keep these under half your income. Common U.S. examples include:

- Housing: Rent, mortgage, or property taxes (average U.S. rent hit $1,700 in 2026).

- Utilities: Electricity, water, internet, and heating.

- Food: Groceries, not dining out.

- Transportation: Car payments, gas, public transit, or insurance.

- Minimum debt payments: Credit cards, student loans, or auto loans.

- Healthcare: Premiums, copays, or Medicare/Medicaid costs.

- Childcare or eldercare if essential.

If needs exceed 50%—common in pricey areas like California or New York—it's a signal to cut back or boost income.

Wants: 30% for Life's Enjoyments

Wants fuel happiness without survival stakes. This bucket covers choices that enhance your lifestyle. Think:

- Dining out or takeout.

- Entertainment: Streaming services, concerts, or sports tickets.

- Travel and vacations.

- Hobbies: Gym memberships, crafts, or gaming.

- Shopping: Clothing, gadgets, or home upgrades beyond basics.

In 2026, with entertainment costs up 5%, track these to avoid creep into needs.

Savings and Debt: 20% for Your Future

This powerhouse category builds long-term security. Allocate to:

- Emergency fund: 3-6 months' expenses in a high-yield savings account.

- Retirement: 401(k) matches or IRA contributions (IRS 2026 limit: $24,000 for 401(k)).

- Debt payoff: Extra on student loans, credit cards (beyond minimums).

- Goals: Home down payment, college savings via 529 plans, or investments.

Prioritize high-interest debt first, then savings. Tools like the IRS withholding estimator help maximize take-home pay.

A Real-World 50/30/20 Budget Example for Americans

Meet Sarah, a teacher in Texas earning $4,000 monthly after taxes (common for mid-level U.S. jobs).

| Category | Percentage | Amount | Examples |

|---|---|---|---|

| Needs | 50% | $2,000 | $1,200 rent, $300 groceries, $200 utilities, $150 car insurance/gas, $150 student loan minimum |

| Wants | 30% | $1,200 | $400 dining/entertainment, $300 shopping, $300 travel, $200 hobbies |

| Savings/Debt | 20% | $800 | $400 emergency fund, $300 extra debt payoff, $100 401(k) |

If rent spikes to $1,500, Sarah trims wants to $1,000 and boosts savings to $500—showing the rule's adaptability.

Benefits of the 50/30/20 Rule

- Simplicity: Easy to remember and apply, perfect for budgeting newbies.

- Balance: Ensures fun alongside saving, reducing burnout.

- Flexibility: Adjust for high-cost living (e.g., 60/20/20 if needs overrun).

- Goal-Oriented: Forces progress on debt and retirement, key for Americans with $1.7 trillion in student loans.

- Awareness: Highlights overspending without daily tracking.

Common Challenges and How to Overcome Them

Not everyone fits perfectly—here's how to tweak for U.S. realities in 2026.

When Needs Exceed 50%

In expensive metros, housing alone can hit 40%. Solutions:

- Refinance mortgages via FHA programs.

- Downsize or get roommates.

- Shop utilities through state marketplaces.

- Adjust to 60/20/20 temporarily.

Irregular Income? Adapt It

For gig workers or freelancers (20% of Americans), base on average monthly take-home. Use apps like Mint or YNAB for tracking.

High Debt Loads

Shift more to the 20% bucket for payoff. Check student loan forgiveness via StudentAid.gov.

Practical Tips to Implement the 50/30/20 Rule Today

- Calculate take-home pay: Use IRS Withholding Estimator at irs.gov.

- Track for one month: Categorize expenses with free tools like Excel or PocketGuard.

- Automate: Set up direct deposits to savings/high-yield accounts (FDIC-insured up to $250,000).

- Review quarterly: Adjust for life changes like raises or inflation.

- Scale up savings: Once stable, aim for 25% in savings per BLS guidelines.

Start small—many see savings grow 20% in the first year.

Take Control with the 50/30/20 Rule

The 50/30/20 budget rule empowers you to spend wisely, save aggressively, and enjoy life—tailored for American realities like taxes and rising costs. Start today: Grab last month's bank statements, run the numbers, and automate transfers. Track progress monthly, and you'll build habits for lasting financial health. Your future self—and wallet—will thank you.

Frequently Asked Questions

Sources & References

-

1

50/30/20 Rule Explained: How It Works and Why It Matters - Gotrade — www.heygotrade.com

-

2

Understanding the 50-30-20 Budget Rule - Mutual of America — www.mutualofamerica.com

-

3

What Is The 50/30/20 Budget Rule? - Chase — www.chase.com

-

4

What is the 50/30/20 Budget Rule, and Is it Right for You? - Citizens Bank — www.citizensbank.com

-

5

Revisiting 50/30/20 for 2026 - Maps Credit Union — www.mapscu.com

-

6

50-30-20 Budgeting Framework - Harvard FCU Blog — blog.harvardfcu.org

-

7

Budgeting basics: The 50-30-20 rule - UNFCU — www.unfcu.org

Related Articles

How to Build a 6-Month Emergency Fund on a Minimum Wage

Building a six-month emergency fund on minimum wage might feel impossible, but it's more achievable than you think. With the right strategy and consistent effort, you can create a financial safety net...

The Best "Financial Literacy" Books Every American Should Read in 2026

Imagine standing at the edge of financial freedom, armed with knowledge that turns everyday dollars into lifelong security. In 2026, with inflation hovering around 2.5% and retirement accounts like 40...

How to Avoid "Lifestyle Creep" After a 2026 Promotion

Picture this: You've just landed that well-deserved promotion in 2026, your salary jumps by 20% or more, and suddenly you're eyeing a sleeker car, fancier dinners out, or that home upgrade you've alwa...

The Best Cashback Apps for Grocery Shopping in 2026

Imagine slashing your grocery bill by hundreds of dollars each year without clipping coupons or hunting for sales. In 2026, cashback apps make it simple for Americans to earn real money back on everyd...