How to Lower Your Car Insurance Premium

Car insurance premiums hitting your wallet harder than expected? You're not alone—average full coverage rates for Americans reached $2,543 annually in 2026, up from previous years due to rising repair...

Car insurance premiums hitting your wallet harder than expected? You're not alone—average full coverage rates for Americans reached $2,543 annually in 2026, up from previous years due to rising repair costs and claims.[1] But here's the good news: simple, proven steps can slash your bill by hundreds or even thousands without skimping on protection. This guide walks you through actionable ways to lower your car insurance premium right now, tailored for U.S. drivers.

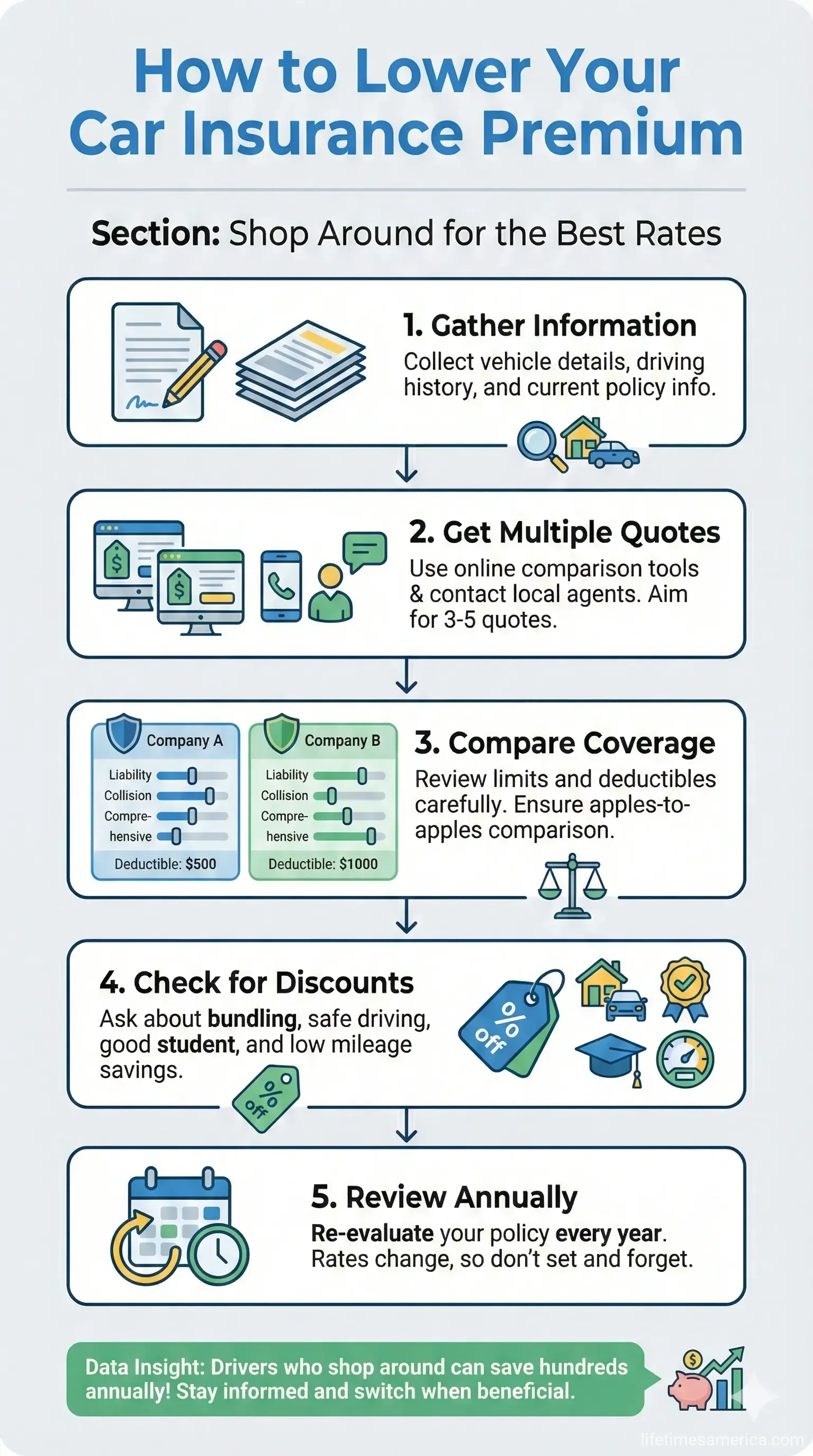

Shop Around for the Best Rates

Don't stick with your current insurer out of loyalty—rates vary widely between companies based on your age, location, driving record, and vehicle.[1] Switching alone can save $200–$500+ yearly.[1]

Compare Quotes Annually

Make it a habit to get fresh quotes every renewal. Standardize comparisons by using identical coverage limits, deductibles, and add-ons—otherwise, you're comparing apples to oranges.[2] Tools from sites like Insurance Information Institute (iii.org) or state insurance departments help you benchmark fairly.

- Request quotes from at least three insurers, including national players like State Farm, Geico, and Progressive, plus regional options.

- Check independent agents via Trusted Choice network for multi-carrier access.

- Time your shop around 21–30 days before renewal to avoid lapses that flag you as high-risk.[1]

Pro tip: Use online aggregators but verify directly with carriers, as some discounts don't show up in preliminary quotes.

Bundling Policies: The Easiest Big Win

Combine your auto insurance with home, renters, or even motorcycle coverage for multi-policy discounts of 15–25% on both.[1][3] Liberty Mutual and others report bundling as one of the top savers, simplifying your life with one login and payment.[3]

Who Qualifies and How Much?

Whether you own or rent, bundling works. Allstate and Geico often sweeten deals for multi-vehicle households too.[5] Expect $300–$800 annual savings on average, per 2026 data.[2]

- Homeowners: Pair with auto for max discount.

- Renters: Still eligible—don't overlook this.

- Multiple cars: Insure all with one carrier for per-vehicle perks.[1]

"Combining your home and auto policies to one insurance carrier is one of the easiest ways to lower your insurance rate."[3]

Increase Your Deductible Wisely

Raising your deductible—the amount you pay out-of-pocket before coverage kicks in—from $200 to $500 can drop premiums 15–30%.[4] Bumping to $1,000 might save $100–$400 yearly, but only if you have savings to cover it.[1][6]

Calculate Your Risk

Before adjusting, stash the deductible amount in a high-yield savings account. For a family sedan, this tweak alone pays off quick if you're claim-free.[6]

| Current Deductible | New Deductible | Potential Annual Savings |

|---|---|---|

| $200 | $500 | $150–$300[4] |

| $500 | $1,000 | $200–$400[1][6] |

State laws require minimum liability, but deductibles are flexible—check your policy via NAIC.org for guidelines.

Maximize Discounts You Qualify For

Stack discounts like good student (10–25% for B-average or better), defensive driving courses (5–15%), and low-mileage perks.[1] Claiming all can net $150–$300 yearly.[1]

Top Discounts for 2026

- Good Driver/Safe Driving: 3–5 accident-free years qualify; programs like Liberty Mutual's RightTrack® track habits for more.[3]

- Good Student: For teens away at college too.[3]

- Military/Employer: Active, retired, or group rates via work/school.[3]

- Paperless/Pay-in-Full: 3–5% off, plus upfront payment skips billing fees.[2]

- Safety Features: Airbags, anti-theft, ABS—$100–$300 savings.[1][6]

Electric/hybrid owners: Some get green vehicle discounts, offsetting higher repair costs.[6]

Right-Size Coverage for Your Needs

For older cars worth under $4,000, drop collision/comprehensive for liability-only—halving premiums while meeting state minimums.[1][5] Saves $200–$600 yearly.[1]

When to Trim Extras

- Paid-off vehicles: Focus on liability if replacement cost is low.[2]

- Remove off-nest drivers: Kids at college? Drop them if not using your car.[1]

- Usage-Based Insurance (UBI): Track miles/habits via apps like Allstate's Drivewise for $100–$500 off safe drivers.[1][6]

Boost Your Insurance Score and Habits

Your insurance score (tied to credit) influences rates in most states—improve it for $300–$1,000+ savings.[1] Avoid lapses, small claims, and build credit steadily.

Daily Habits That Pay Off

- Maintain continuous coverage—no gaps.[1]

- Pay minor repairs yourself to dodge surcharges.[1]

- Drive less? Report low mileage for discounts.[6]

- Complete defensive driving online (AAA or AARP courses, $20–$40).[1]

Usage-Based and Low-Mileage Options

Remote workers or public transit users: Low-mileage or pay-per-mile plans reward you. Insurers like Mile Auto charge by tracked miles, ideal for under 10,000/year.[6]

FAQ

How much can I save by shopping around?

Average savings hit $200–$500+ annually by comparing quotes.[1]

Is bundling worth it if I rent?

Yes—renters qualify for 15–25% off auto when bundled.[1][3]

Will raising my deductible affect claims?

Only out-of-pocket costs rise; ensure savings cover an emergency fund first.[4][6]

Do electric vehicles lower premiums?

Safety features often do, netting $100–$300, though repairs may offset.[6]

What's the best discount for students?

Good student: 10–25% for B average or better.[1][3]

Can I lower rates after a DUI?

Yes, via safe driving courses, higher deductibles, and clean records over time.[4]

Take Control of Your Premiums Today

Start with a quick quote comparison and discount audit—many changes take effect next billing cycle. Track savings in a 401(k) or emergency fund to compound wins. Contact your insurer or visit iii.org for state-specific minimums. Lowering your car insurance premium isn't luck; it's smart action for your family's financial security.

Sources & References

- 10 Proven Ways to Lower Your Auto Insurance Premiums in 2026 — gettia.com

- 5 Ways to Lower Your Car Insurance in 2026 - Finhabits — finhabits.com

- 13 Ways to Lower Your Car Insurance Rate | Liberty Mutual — libertymutual.com

- 11 Ways to Lower Car Insurance Costs in 2026 — insurify.com

- When Does Car Insurance Go Down? - Allstate — allstate.com

- How to lower car insurance premiums in 2026 - The Baldwin Group — baldwin.com

Useful Tools

Related Articles

The Truth About Term Life vs. Whole Life Insurance

Choosing the right life insurance can feel overwhelming, but understanding the core differences between term life and whole life insurance empowers you to protect your family's future without overpayi...

The Best Term Life Insurance for Parents with Young Kids

As parents with young kids, you're juggling diapers, daycare drop-offs, and dreams for their future—all while knowing one unexpected event could upend everything. Term life insurance steps in as your...

How to Save Money on Homeowners Insurance in 2026

With home insurance premiums climbing due to inflation, climate risks, and rising rebuilding costs, American homeowners are feeling the pinch in 2026.Saving money on homeowners insurance doesn't mean...

How to Lower Your Car Insurance Premiums in 2026

Car insurance premiums have surged in recent years, with national rates jumping about 20% from 2024 to 2025 alone, leaving even safe drivers stunned by renewal notices.But in 2026, you can fight back...