What Is a HELOC and How Does It Work?

Imagine tapping into the value you've built in your home without selling it or taking out a rigid lump-sum loan. That's the power of a HELOC, or home equity line of credit—a flexible financing tool th...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine tapping into the value you've built in your home without selling it or taking out a rigid lump-sum loan. That's the power of a HELOC, or home equity line of credit—a flexible financing tool that's helped countless American homeowners fund renovations, pay for college, or consolidate debt in 2026.

In today's housing market, with median home prices hovering around $420,000 and many owners sitting on substantial equity, a HELOC offers a revolving credit line backed by your property.What is a HELOC and how does it work? It's essentially a credit card secured by your home's equity, letting you borrow as needed up to a limit, pay interest only on what you use, and redraw funds as you repay.

What Is a HELOC?

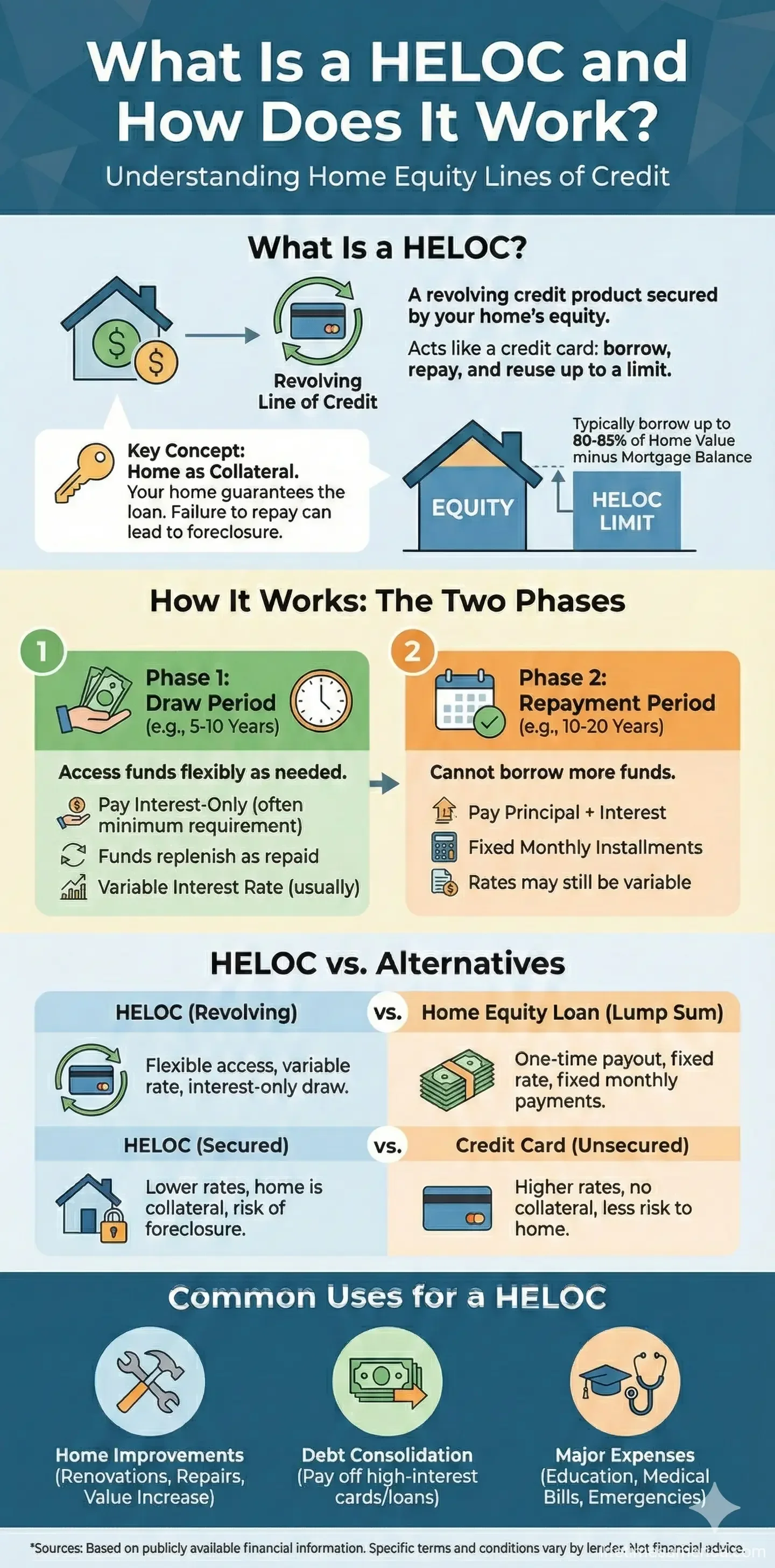

A home equity line of credit (HELOC) is a second mortgage that allows you to borrow against the equity in your home—the difference between your property's current market value and what you still owe on your primary mortgage. Unlike a traditional home equity loan, which disburses a one-time lump sum with fixed payments, a HELOC provides ongoing access to funds during a "draw period," much like a credit card.

Secured by your home as collateral, HELOCs typically carry lower interest rates than unsecured options like personal loans or credit cards—often several percentage points below, thanks to the reduced risk for lenders. In 2026, with variable rates averaging around 8-9% for qualified borrowers, they're a smart choice for flexible borrowing.

Key Features of a HELOC

- Revolving Credit: Borrow, repay, and borrow again up to your approved limit without reapplying.

- Variable Rates: Interest fluctuates with market indexes like the prime rate, so payments can change.

- Two Phases: Draw period (5-10 years) for accessing funds, followed by repayment (10-20 years).

- Interest-Only Payments: During the draw period, you often pay just interest on the borrowed amount.

How Does a HELOC Work?

Understanding how a HELOC works starts with qualification. Lenders assess your home's appraised value, your outstanding mortgage balance, credit score (typically 620+ FICO), debt-to-income ratio (under 43%), and combined loan-to-value (CLTV) ratio.

Step-by-Step Process

- Appraisal and Approval: Your home is appraised. Lenders cap HELOCs at 80-90% of your home's value minus your mortgage. Example: For a $400,000 home with $240,000 owed and an 85% CLTV limit, max HELOC = ($400,000 × 0.85) - $240,000 = $100,000.

- Draw Period (5-10 Years): Access funds via checks, transfers, or a debit card. Borrow only what you need—pay interest solely on the outstanding balance. Repay principal to free up credit.

- Repayment Period (10-20 Years): No more draws; repay principal plus interest in fixed installments. Payments rise as you tackle the full balance.

- Closing: Expect fees like appraisals ($300-500), closing costs (1-5% of limit), and possible annual fees.

Here's a quick comparison of HELOCs versus alternatives:

| Option | Collateral | Approval Time | Avg. Rate (2026) | Repayment |

|---|---|---|---|---|

| HELOC | Yes (Home) | 4-7 weeks | 8-9% variable | Draw + Repay periods |

| Home Equity Loan | Yes (Home) | 4-7 weeks | 7.5-8.5% fixed | 5-30 years fixed |

| Cash-Out Refi | Yes (Home) | 30-60 days | 6.5-7.5% | 15-30 years |

| Personal Loan | No | 1-5 days | 7-36% | 1-7 years |

Pros and Cons of a HELOC

Advantages

- Flexibility: Borrow only what you need, ideal for ongoing projects like home remodels.

- Lower Rates: Collateral keeps costs down compared to credit cards (20%+ APR).

- Tax Benefits: Interest may be deductible if used for home improvements (consult IRS Publication 936).

- No Refinancing Needed: Keeps your low-rate primary mortgage intact.

Disadvantages and Risks

- Variable Rates: Payments can spike if rates rise—prime rate has climbed 0.5% in early 2026.

- Home at Risk: Default could lead to foreclosure.

- Balloon Payments: Some HELOCs require full repayment at end of term.

- Fees: Origination, appraisal, and inactivity charges add up.

HELOC Qualification Requirements in 2026

To qualify, you'll need at least 15-20% equity post-HELOC, a credit score of 620-680+, stable income, and DTI under 43%. Shop lenders via Bankrate or LendingTree, and check credit reports for free at AnnualCreditReport.com weekly.

Pro Tip: Use the CFPB's mortgage calculator at consumerfinance.gov to estimate affordability.

Common Uses for HELOC Funds

- Home improvements (boosting resale value)

- Debt consolidation (lower rates than cards)

- Education expenses

- Emergency funds or major purchases

Practical Tips for Using a HELOC Wisely

- Borrow Conservatively: Aim for no more than 50% of available equity to buffer home value drops.

- Lock in Rates if Possible: Some lenders offer fixed-rate conversions during draw period.

- Track Payments: Use apps like Mint to monitor variable rates.

- Plan for Repayment: Build an emergency fund covering 6 months of payments.

- Compare Lenders: Credit unions often have lower fees than big banks.

Next Steps: Is a HELOC Right for You?

A HELOC shines for disciplined borrowers needing flexibility, but it's not for everyone—especially if rates are rising or your job is unstable. Calculate your equity today, pull your credit report, and compare quotes from at least three lenders. Tools like the Federal Reserve's rate monitor at federalreserve.gov can keep you informed. Consult a financial advisor or use HUD-approved counseling at hud.gov for personalized guidance. With smart use, a HELOC can unlock your home's value without the full commitment of selling.

Frequently Asked Questions

Sources & References

-

1

How Does a HELOC Work? Complete Guide for 2026 — trussfinancialgroup.com

-

2

What You Need to Know About HELOCs in 2026 - Experian — www.experian.com

-

3

What Is a HELOC? Benefits, How It Works, and Key Insights — www.pfcu.com

-

4

What Is A HELOC (Home Equity Line Of Credit)? | Bankrate — www.bankrate.com

-

5

Understanding HELOCs for Homeowners | Comerica — www.comerica.com

-

6

What is a HELOC and how does it work? - Fidelity Bank — www.bankatfidelity.com

-

7

What Is Home Equity Line Of Credit Or HELOC? - HSBC Bank USA — www.us.hsbc.com

Related Articles

The Best "Personal Loans" for Home Improvements in 2026

Planning a kitchen remodel, backyard makeover, or energy-efficient upgrade in 2026? A personal loan can get your project off the ground fast without tapping home equity. These unsecured loans offer qu...

How to Apply for "Disaster Relief" Loans After a Major US Storm

When a major storm devastates your community, the road to recovery can feel overwhelming. But disaster relief loans from U.S. federal agencies offer a vital lifeline, providing low-interest funds to r...

How to Get a "Portfolio Line of Credit" (SBLOC) instead of a Personal Loan

Imagine needing quick cash for home repairs or a family emergency without selling your prized stock portfolio or racking up high-interest credit card debt. A Portfolio Line of Credit (SBLOC) could be...

What Is a Down Payment and How Much Do You Need?

When you're ready to buy a home, one of the first questions you'll face is: how much money do you need upfront? That upfront cash is your down payment, and it's one of the most important decisions you...