What Is Life Insurance and Do You Really Need It?

Imagine this: You're the primary breadwinner in your family, and one unexpected day, you're no longer there to provide. Bills pile up, the mortgage looms, and your loved ones struggle to make ends mee...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine this: You're the primary breadwinner in your family, and one unexpected day, you're no longer there to provide. Bills pile up, the mortgage looms, and your loved ones struggle to make ends meet. That's where life insurance steps in—a financial safety net that pays out to your beneficiaries when you pass away, helping them cover essentials like funeral costs, debts, and daily living expenses.Life insurance is a contract between you and an insurer, promising a death benefit in exchange for your premiums, but do you really need it? Let's break it down for Americans navigating 2026's economic landscape, where inflation and rising costs make protection more crucial than ever.

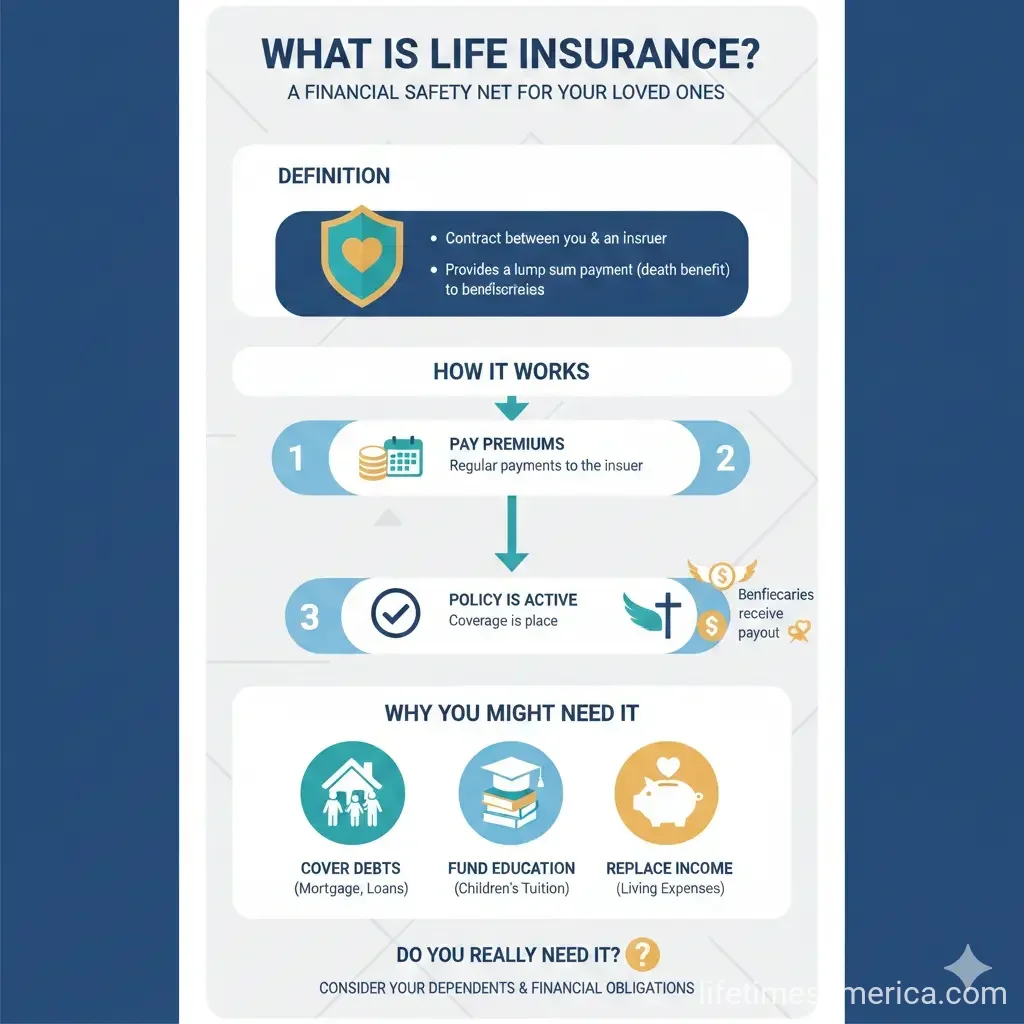

What Is Life Insurance?

At its core, life insurance provides a lump-sum payment, known as the death benefit, to your designated beneficiaries upon your death while the policy is active. This money is typically tax-free and can replace lost income, pay off debts, or fund education and retirement. Policies fall into two main categories: term life insurance (temporary coverage for a set period) and permanent life insurance (lifelong coverage with cash value buildup).

In the United States, life insurance is regulated at the state level, with organizations like the National Association of Insurance Commissioners (NAIC) setting model guidelines to protect consumers. Premiums—the amount you pay to keep the policy active—vary based on age, health, lifestyle, and coverage amount. For context, a healthy 30-year-old non-smoker might pay as little as $30 per month for basic term coverage in 2026.

How Does Life Insurance Work?

You select a policy, undergo a medical exam (for most types), and pay premiums. If you die during the coverage period, your beneficiaries receive the death benefit. No death during the term? Coverage ends (for term policies), or you can access cash value (for permanent ones). Many policies include riders—like accelerated death benefits for terminal illness—to customize protection.

Types of Life Insurance: Term vs. Permanent

Choosing the right type depends on your needs, budget, and goals. Here's a breakdown of the main options available in 2026.

Term Life Insurance

Term life offers pure protection for a specific duration, usually 10, 20, or 30 years—perfect for covering a mortgage or kids' college years. It's the most affordable, with no cash value; if you outlive the term, coverage simply expires. Variants include:

- Convertible term: Switch to permanent without a new exam.

- Increasing term: Death benefit rises with inflation.

Best for young families or those on a budget. Example: A $500,000, 20-year term policy for a 35-year-old might cost $25–$40 monthly.

Permanent Life Insurance

Permanent policies last your lifetime (as long as premiums are paid) and build cash value—a savings component that grows tax-deferred. They're pricier but offer lifelong security and investment potential. Key subtypes:

- Whole life: Fixed premiums, guaranteed cash value growth, and death benefit. Starts around $380/month; safest for predictability.

- Universal life: Flexible premiums and death benefits; cash value tied to interest rates. Cheaper than whole but adjustable for changing needs.

- Variable life: Cash value invested in stocks/mutual funds for higher growth potential, but with market risk.

- Variable universal life and indexed universal life: Combines flexibility and investment options.

- Final expense/burial insurance: Small policies ($5,000–$25,000) for funeral costs; no exam needed for simplified/guaranteed issue.

- Group life: Often employer-provided, low-cost term coverage.

| Type | Coverage Duration | Cash Value? | Avg. Monthly Cost (2026 est.) | Best For |

|---|---|---|---|---|

| Term | 10–30 years | No | $30+ | Temporary needs |

| Whole | Lifetime | Yes, guaranteed | $380+ | Long-term security |

| Universal | Lifetime | Yes, flexible | $200+ | Adjustable budgets |

| Variable | Lifetime | Yes, market-linked | $250+ | Investment-savvy |

Data synthesized from 2026 quotes; actual rates vary.

Do You Really Need Life Insurance? Key Factors for Americans

Not everyone needs it, but most do—especially if others depend on your income. Consider these U.S.-specific scenarios:

- Dependents: Spouses, kids, or aging parents relying on you.

- Debts: Mortgage (average U.S. home: $400,000+), student loans, or credit cards.

- Stay-at-home parents: Coverage for childcare/replacement services ($100,000+ value).

- Business owners: Key person or buy-sell agreements.

- Singles: Maybe not, unless for funeral costs (~$9,000 average) or debts.

Rule of thumb: Aim for 10–15x your annual income, per financial experts. In 2026, with Social Security's projected shortfalls and Medicare gaps, private life insurance fills critical voids. Employer group plans are a start, but they're not portable—supplement with personal coverage.

Pros and Cons

Pros: Financial security, tax advantages (death benefit tax-free under IRC Section 101), estate planning tool.

Cons: Costly if over-insured; permanent types have fees/surrender charges.

"The golden rule is to get the coverage amount correct so the family is taken care of." – Patrick Blevins, State Farm agent

How to Buy Life Insurance in the U.S. in 2026: Practical Steps

- Assess needs: Use online calculators from NAIC or insurers.

- Compare quotes: Shop via marketplaces like Policygenius or directly from carriers (State Farm, Guardian).

- Health check: Quit smoking, exercise—premiums drop 50%+ for healthy habits.

- Choose riders: Add waiver of premium for disability.

- Review annually: Life changes (marriage, kids) mean adjustments.

State laws require clear policy disclosures; check your state's insurance department via NAIC.org for complaints.

Next Steps: Secure Your Family's Future Today

Life insurance isn't just a policy—it's peace of mind in an unpredictable world. Start by calculating your needs (try free tools at usa.gov or irs.gov for estate basics), gather quotes from 3–5 insurers, and consult a licensed agent. In 2026, with rates at historic lows for healthy buyers, there's no better time. Protect what matters—your family's tomorrow depends on it.

Frequently Asked Questions

Sources & References

-

1

4 Different Types of Life Insurance & How to Choose in 2026 — www.nerdwallet.com

-

2

Types of Life Insurance in 2026 (Compare Coverage Options!) — www.quote.com

-

3

Life insurance - Wikipedia — en.wikipedia.org

-

4

Types of Life Insurance Explained and How to Choose | Guardian — www.guardianlife.com

-

5

What Is Life Insurance? Types, Benefits & How It Works — www.westernsouthern.com

-

6

Life Insurance Basics: What It Is, How It Works and Types - State Farm — www.statefarm.com

-

7

Understanding the Three Basic Types of Life Insurance: Term, Universal and Whole Life — www.kramerwealth.com

-

8

What Type of Life Insurance Is Right for You? - NAIC — content.naic.org

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...