What Is a Deductible in Insurance? (Health, Home, and Auto)

Imagine getting into a fender bender, facing a surprise medical bill, or dealing with storm damage to your roof—only to discover you owe hundreds or thousands before your insurance steps in. That's th...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine getting into a fender bender, facing a surprise medical bill, or dealing with storm damage to your roof—only to discover you owe hundreds or thousands before your insurance steps in. That's the reality of a deductible, a core part of most insurance policies in the U.S. Understanding what a deductible in insurance is for health, home, and auto coverage can save you money, stress, and surprises when you need protection most.

In this guide, we'll break down deductibles across these key areas, explain how they work with 2026 numbers, and share practical tips to choose the right one for your budget. Whether you're shopping on the ACA Marketplace, bundling home and auto policies, or navigating Medicare, you'll walk away ready to make smart decisions.

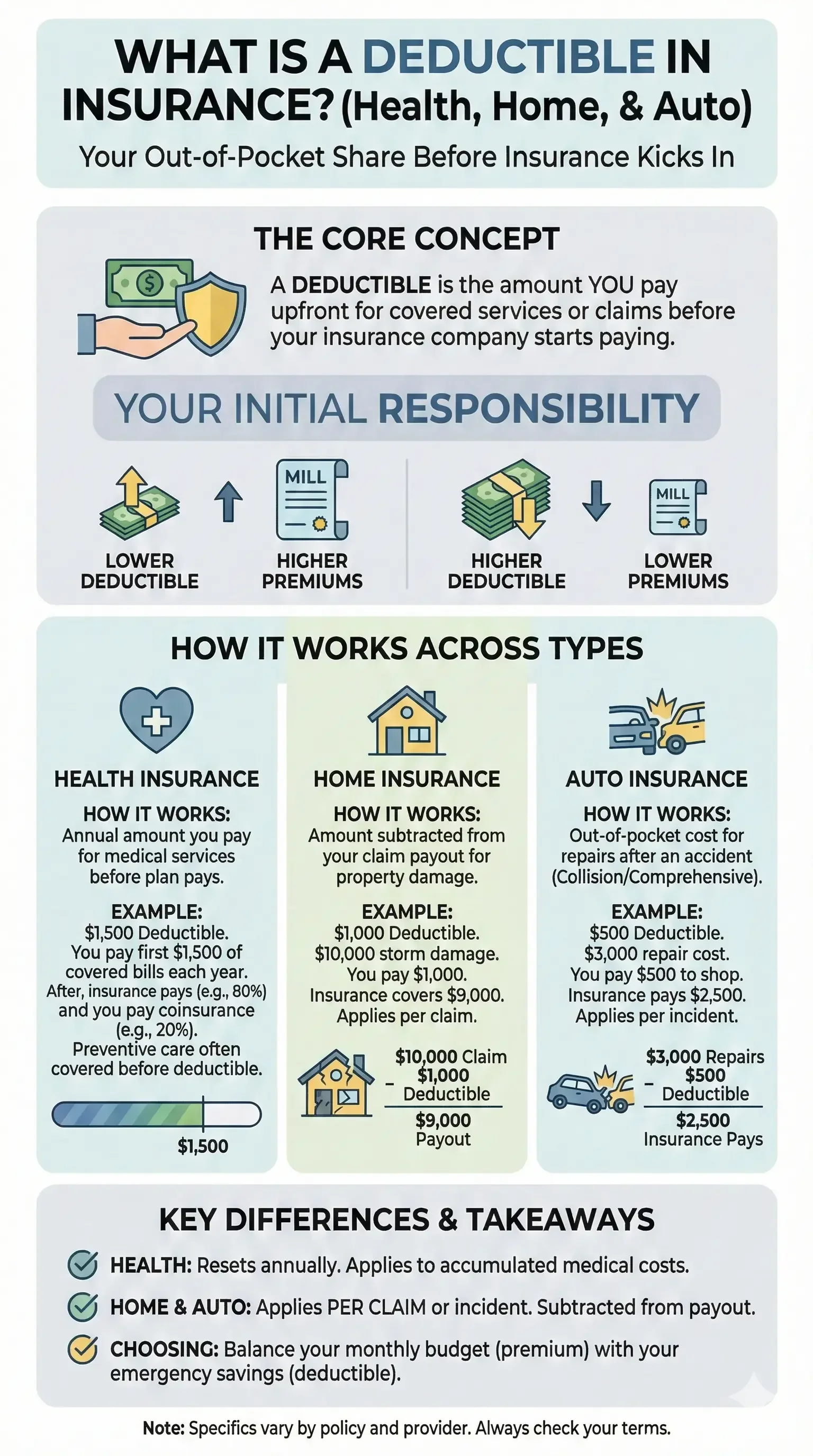

What Is a Deductible in Insurance?

A deductible is the amount you pay out of pocket for a covered loss or service before your insurance company starts covering costs. It's a form of cost-sharing designed to keep premiums affordable while encouraging policyholders to handle smaller claims themselves.

Deductibles come in two main types:

- Dollar deductibles: A fixed amount, like $500 or $1,000, subtracted from your claim payout.

- Percentage deductibles: Common in homeowners insurance, calculated as a percent of your home's insured value (e.g., 2% of $300,000 = $6,000).

State regulations govern how deductibles appear in policies and are applied, varying by location—for instance, hurricane-prone states like Florida often mandate higher percentage deductibles for wind damage. You'll find your deductible listed on the declarations page of your policy.

How Deductibles Affect Your Premiums

Higher deductibles mean lower monthly premiums, and vice versa. For example:

- Raising your auto deductible from $200 to $500 can cut collision and comprehensive premiums significantly.

- Opting for a $1,000+ homeowners deductible often saves 10-25% on premiums.

This trade-off suits those with emergency savings but can backfire if you're cash-strapped during a claim.

Deductibles in Health Insurance

Health insurance deductibles are annual amounts you pay for covered services before your plan pays its share (except for preventive care, which is often free under the ACA). In 2026, many ACA Marketplace plans—especially Bronze and some Silver tiers—feature high deductibles paired with low premiums, ideal for healthy individuals but risky for frequent care needs.

2026 Health Deductible Examples

Average deductibles in ACA plans have evolved, with many families facing $3,000-$5,000 annually. Here's how it works:

- If your deductible is $3,000, you pay 100% of covered services until reaching that threshold. Then, coinsurance (e.g., 20%) kicks in until you hit your out-of-pocket maximum.

- Plans may have separate medical and prescription deductibles.

For Medicare in 2026:

- Part A inpatient hospital deductible: $1,736 per benefit period (up $60 from prior year).

- Part B annual deductible: Tied to income via IRMAA (Income-Related Monthly Adjustment Amount). Base is around $121.60 extra for higher earners, scaling up to $649.20 for individuals over $205,000 MAGI.

| Income Bracket (Individual) | Joint Filer Equivalent | Part B IRMAA (2026) |

|---|---|---|

| ≤ $109,000 | ≤ $218,000 | $0 |

| $109,001-$137,000 | $218,001-$274,000 | $81.20 |

| $137,001-$171,000 | $274,001-$342,000 | $202.90 |

| $171,001-$205,000 | $342,001-$410,000 | $324.60 |

| $205,001-$500,000 | $410,001-$750,000 | $446.30 |

Note: IRMAA affects premiums based on MAGI from two years prior. Check IRS.gov for updates.

Practical Tips for Health Deductibles

- Compare plans on Healthcare.gov during Open Enrollment (Nov 1-Jan 15 for 2026 coverage).

- Build an HSA (Health Savings Account) if eligible—contributions are tax-deductible up to $4,300 individual/$8,550 family in 2026.

- Track expenses with apps to meet deductibles efficiently.

Deductibles in Homeowners Insurance

Homeowners deductibles apply per claim, often $500-$2,500 for standard policies, or 1-5% for perils like hurricanes. If your home is insured for $400,000 with a 2% deductible, you'd pay $8,000 before coverage on a $20,000 roof repair claim.

In 2026, with rising home values and climate risks, insurers in states like California and Texas push higher deductibles to manage costs. All perils typically share one deductible, but wind/hail may have a separate percentage one.

Choosing the Right Home Deductible

- Low ($500): Higher premiums; best if low savings.

- Medium ($1,000): Balances cost; common choice.

- High ($2,500+): Saves up to 20% on premiums; requires $5,000+ emergency fund.

Tip: Bundle with auto for discounts up to 25% via providers like Allstate.

Deductibles in Auto Insurance

Auto deductibles apply separately to collision (at-fault accidents) and comprehensive (theft, weather) coverages, typically $500 or $1,000. Unlike health, they reset per claim—not annually.

Example: $3,000 repair with $500 deductible = you pay $500, insurer pays $2,500. No-fault states like Michigan may have medical deductibles too.

2026 Auto Trends and Savings

With EV repairs costing more, 2026 policies trend toward $1,000 deductibles for premium relief. Raising from $500 to $1,000 can save 15-30% on full coverage.

Actionable advice:

- Shop via sites like Insurify or directly with Geico, Progressive.

- Pay deductibles via credit card for rewards (pay off immediately).

- Waive for glass claims if offered (common in FL, TX).

Deductibles Across Policies: Key Comparisons

| Insurance Type | Typical 2026 Deductible | Resets | Premium Impact |

|---|---|---|---|

| Health | $1,500-$5,000 (ACA); $1,736 Part A Medicare | Annually | High deductible = low premium |

| Home | $1,000 dollar or 1-5% | Per claim | $2,500 saves 15-25% |

| Auto | $500-$1,000 per coverage | Per claim | $1,000 saves 20%+ |

Common Mistakes and How to Avoid Them

- Underestimating needs: Test affordability—could you pay $2,000 tomorrow?

- Ignoring multiples: Auto has separate collision/comprehensive; health may split Rx.

- Forgetting resets: Health annual; others per incident.

- Skipping reviews: Reassess yearly at renewal.

Next Steps to Optimize Your Coverage

Review your policies today: Log into your insurer portal or call for a deductible quote comparison. Use Healthcare.gov for health, or tools from the NAIC (naic.org) for home/auto benchmarks. Aim for a deductible you can cover 2-3x over in savings. Consult a licensed agent for personalized bundles, and set calendar reminders for 2026 Open Enrollment. Smart choices now mean peace of mind later.

Frequently Asked Questions

Sources & References

-

1

2026 Medicare Parts A & B Premiums and Deductibles - CMS — www.cms.gov

-

2

Understanding your insurance deductibles | III — www.iii.org

-

3

What Is a Deductible? | Allstate — www.allstate.com

- 4

-

5

Deductibles in ACA Marketplace Plans, 2014-2026 - KFF — www.kff.org

-

6

What is An Insurance Deductible? A Simple Guide for 2026 - Breeze — www.meetbreeze.com

-

7

Premiums, Deductibles, Coinsurance & Copays Explained | Aetna — www.aetna.com

-

8

How do deductibles, coinsurance and copays work? - BCBSM — www.bcbsm.com

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...