What Is a Debt-to-Income Ratio and Why Do Banks Care?

Imagine you're eyeing your dream home, but the bank turns you down—not because of your credit score, but because your monthly bills are eating up too much of your paycheck. That's where your debt-to-i...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine you're eyeing your dream home, but the bank turns you down—not because of your credit score, but because your monthly bills are eating up too much of your paycheck. That's where your debt-to-income ratio (DTI) comes into play. Banks scrutinize this number to decide if you can handle a new mortgage alongside your existing debts, and understanding it can make or break your path to homeownership or other big loans in 2026.

In the United States, where average household debt hit record levels last year, keeping your DTI in check is more crucial than ever—especially with mortgage rates hovering around 6-7% and rising living costs. This guide breaks down what a debt-to-income ratio is and why banks care, with step-by-step calculations, real-world examples, and tips tailored for Americans chasing financial stability.

What Is a Debt-to-Income Ratio?

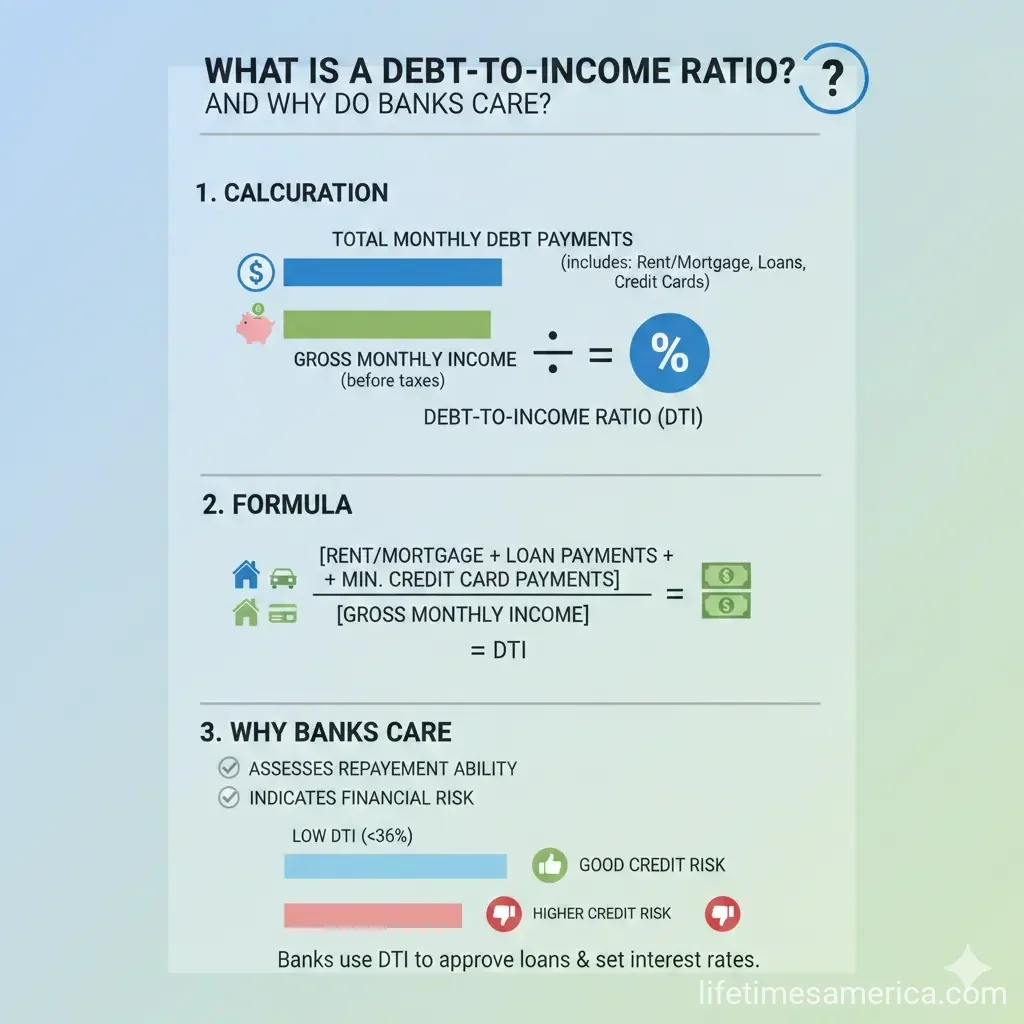

Your debt-to-income ratio (DTI) is a simple percentage that compares your total monthly debt payments to your gross monthly income—before taxes and deductions. Lenders use it as a snapshot of your financial health, showing how much of your income is already tied up in debt.

Think of DTI as a lender's way to gauge if adding a new loan, like a mortgage or auto loan, will stretch you too thin. It's not about your everyday expenses like groceries or utilities—those don't count. Instead, it focuses on recurring debts reported on your credit, such as credit cards, student loans, and car payments.

Front-End vs. Back-End DTI: The Two Types Lenders Watch

Lenders often calculate two versions of DTI:

- Front-end DTI: Measures housing costs only, like your potential mortgage payment, property taxes, homeowners insurance, and HOA fees, divided by gross income. Ideal front-end ratios stay under 28-31%.

- Back-end DTI: The big one—includes all monthly debts (housing plus everything else). This is what most banks emphasize for overall affordability.

For instance, Fannie Mae guidelines stress that back-end DTI, combining the new mortgage with other obligations, is key for loan approval.

How to Calculate Your Debt-to-Income Ratio

Calculating DTI is straightforward and takes just minutes. Follow these steps using your most recent pay stubs and debt statements:

- List all monthly debt payments: Include minimum credit card payments, auto loans, student loans, personal loans, alimony, child support, and current housing (rent or mortgage PITI—principal, interest, taxes, insurance).

- Add your gross monthly income: Pretax earnings from wages, salaries, bonuses, or side gigs used for qualification.

- Divide and multiply: (Total monthly debts ÷ Gross monthly income) × 100 = Your DTI percentage.

Real-World Example for Americans

Say you're a teacher in Texas earning $6,000 gross monthly ($72,000 yearly). Your debts: $450 car loan, $300 student loan, $200 credit cards, $1,500 rent. Total debts: $2,450.

DTI = ($2,450 ÷ $6,000) × 100 = 40.8%. If you're applying for a $300,000 mortgage adding $2,000 monthly PITI, your back-end DTI jumps to about 75%—a red flag for most lenders.

"Your debt-to-income ratio (DTI) is all your monthly debt payments divided by your gross monthly income."

Use free online calculators from CFPB or Bank of America to double-check.

Why Do Banks Care About Your DTI?

Banks aren't just number-crunchers—they're protecting their investments. A high DTI signals risk: if too much income goes to debts, you're more likely to miss payments during job loss or emergencies. In 2026, with inflation at 2.5% and unemployment steady at 4.2%, lenders are extra cautious per Federal Reserve data.

DTI helps predict default risk. Government-backed loans like FHA allow up to 50% DTI with compensating factors (e.g., strong savings), while conventional loans cap at 36-43% via Fannie Mae. Auto loans and credit cards also check DTI, often preferring under 36%.

DTI Thresholds: What Counts as Good in 2026?

| DTI Range | Rating | Lender View |

|---|---|---|

| Under 36% | Excellent | Prime candidate for best rates and approval. |

| 36-43% | Good | Approved, but may need stronger credit or reserves. |

| 43-50% | Risky | Possible with FHA/VA or exceptions; higher rates. |

| Over 50% | Poor | Financial distress; denials common. |

These thresholds vary: VA loans are more flexible (no strict DTI cap), while jumbo mortgages demand under 43%.

How DTI Impacts Your Financial Life in the US

Beyond mortgages, DTI affects renting (landlords check it), credit limits, and even job offers requiring security clearances. High DTI can tank your credit score indirectly by maxing utilization.

In 2026, with student debt averaging $38,000 per borrower and auto loans surging, millennials and Gen Z face DTI hurdles. CFPB reports 30% of Americans exceed 40% DTI, complicating home buys amid housing shortages.

9 Practical Tips to Lower Your DTI Ratio

Ready to improve? Here's actionable advice for US households:

- Pay down high-interest debt: Target credit cards first using debt snowball or avalanche methods.

- Increase income: Side hustle via Uber, freelance on Upwork, or negotiate a raise—report all to lenders.

- Refinance loans: Lower car or student loan rates via SoFi or federal programs.

- Consolidate debts: Personal loans from LightStream can simplify payments.

- Cut non-debt expenses: Though not in DTI, freeing cash helps pay debts faster.

- Dispute errors: Check credit reports at AnnualCreditReport.com (free weekly).

- Avoid new debt: No big purchases pre-application.

- Co-sign wisely: Add a spouse's income, but their debts count too.

- Seek programs: FHA Streamline Refinance or IRS debt relief if taxes are an issue.

Track progress monthly; aim for 36% before applying. Tools like Mint or YNAB integrate DTI tracking.

Take Control of Your DTI Today

Your DTI isn't destiny—it's a lever you can pull for better loans and peace of mind. Start by calculating yours now, then chip away at debts while boosting income. In 2026's economy, a strong DTI opens doors to 401(k) matching jobs, Medicare planning, or that forever home. Visit CFPB.gov for free tools, consult a HUD-approved counselor, or prequalify with lenders like Rocket Mortgage. Small steps today build big financial freedom tomorrow.

Frequently Asked Questions

Sources & References

-

1

Debt-to-Income Ratio (DTI): What is it and how is it calculated? — rocketmortgage.com — www.rocketmortgage.com

-

2

What is Debt-to-Income (DTI) Ratio & Why is It Important — bettermoneyhabits.bankofamerica.com — bettermoneyhabits.bankofamerica.com

-

3

Debt-to-Income Ratio (DTI) - Municipal Credit Union — nymcu.org — www.nymcu.org

-

4

How To Get A Loan With A High Debt-To-Income Ratio [2026] — themortgagereports.com — themortgagereports.com

-

5

What is a debt-to-income ratio? — consumerfinance.gov — www.consumerfinance.gov

-

6

What Debt-to-Income Ratio Means and Why it's Important — salliemae.com — www.salliemae.com

-

7

Debt-to-Income Ratios | Fannie Mae Selling Guide — selling-guide.fanniemae.com — selling-guide.fanniemae.com

-

8

How much debt Is too much? | DTI ratio targets — citizensbank.com — www.citizensbank.com

Useful Tools

Related Articles

What Is a Credit Report and How Is It Different from a Credit Score?

Ever wondered why your loan application got approved with a great rate—or denied outright? It often boils down to two key pieces of your financial puzzle: your credit report and credit score. While pe...

How to Build Credit from Scratch in the USA

Imagine landing your dream apartment in a bustling American city, only to hear "sorry, we need a credit score of at least 650." Or applying for that first car loan after college and getting denied bec...

How to Increase Your Credit Score by 100 Points in 6 Months

Imagine unlocking lower mortgage rates, snagging that dream car loan without sky-high interest, or even qualifying for a premium credit card—all because your credit score jumped 100 points in just six...

What Is a Good Credit Score in the USA?

Imagine landing your dream home or snagging that low-interest auto loan, only to watch it slip away because of one number on your credit report. That number—your credit score—holds more power over you...