What Does FDIC Insurance Mean and Why Does It Matter?

Imagine waking up to news that your bank has failed overnight, wiping out your life savings. For millions of Americans, this nightmare became a real fear during the 2008 financial crisis and recent ba...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine waking up to news that your bank has failed overnight, wiping out your life savings. For millions of Americans, this nightmare became a real fear during the 2008 financial crisis and recent bank collapses. But here's the good news: FDIC insurance steps in to protect your deposits, ensuring you get your money back up to specific limits. Understanding what FDIC insurance means can safeguard your finances and give you peace of mind in an unpredictable economy.

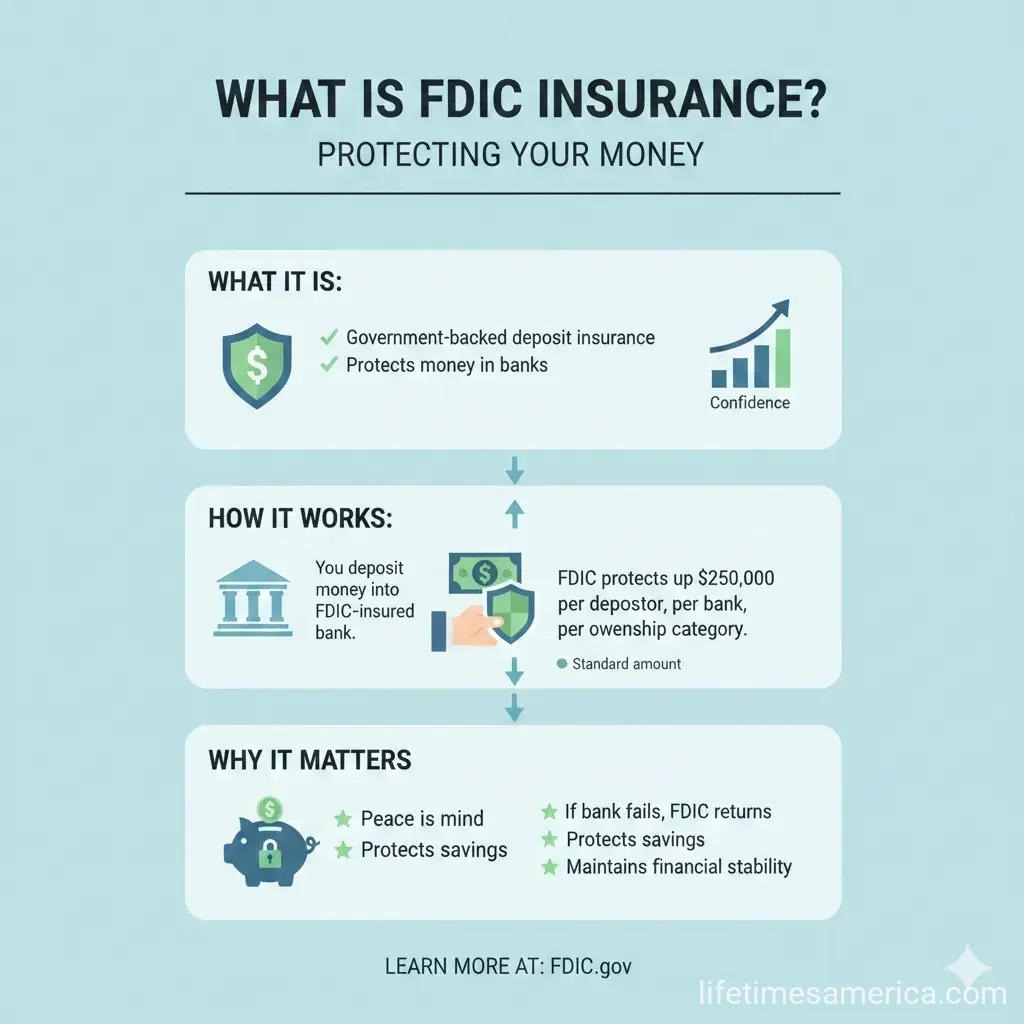

What Is FDIC Insurance?

The Federal Deposit Insurance Corporation (FDIC) is an independent U.S. government agency that protects depositors at FDIC-insured banks and savings associations. Created in 1933 during the Great Depression, it prevents bank runs by guaranteeing deposits if a bank fails.

FDIC insurance is automatic for eligible accounts at member banks—no application needed. It covers principal and accrued interest up to the limit, paid out quickly after a failure, often within days. In 2026, this protection remains a cornerstone of financial stability for everyday Americans managing checking, savings, and retirement funds.

How FDIC Insurance Works in a Bank Failure

When an FDIC-insured bank fails, the agency steps in immediately. It either transfers accounts to a healthy bank or issues checks/debit cards for insured amounts. For example, during the 2023 failures of Silicon Valley Bank and Signature Bank, the FDIC ensured depositors accessed funds swiftly, though some exceeded standard limits due to special measures.

Bank failures are rare—only a handful occur yearly—but FDIC coverage has protected over $17 trillion in deposits as of 2026.

FDIC Insurance Limits in 2026

In 2026, FDIC insurance covers up to $250,000 per depositor, per FDIC-insured bank, per ownership category. This limit has held steady since 2008, despite inflation and calls for increases.

The key is "ownership category," which separates coverage. Multiple accounts in the same category at one bank combine toward the $250,000 limit. Spread across banks or categories, you can insure millions.

Ownership Categories Explained

- Single Accounts: Owned by one person. Checking and savings add up to $250,000 max per bank.

- Joint Accounts: Shared by two+ people; each gets $250,000 coverage. A $500,000 joint savings/CD is fully insured.

- Trust Accounts: Revocable trusts cover $250,000 per beneficiary (up to 5 = $1.25 million per owner as of 2024, extended into 2026).

- IRAs and Retirement: Separate category for IRAs, covering another $250,000.

- Business Accounts: Treated separately if not solely for insurance extension; doesn't affect personal coverage.

| Different Types of Account Ownership | Insured Amount | Uninsured Amount |

|---|---|---|

| Account holder A (single): Savings $50,000 + CD $250,000 | $250,000 | $50,000 |

| Account holders A & B (joint): Savings $150,000 + CD $325,000 | $500,000 | $0 |

| Account holder C (Trust, 5 beneficiaries: $250,000 each) | $1.25 million | $0 |

Source: Adapted from Bankrate examples.

What Accounts Are Covered by FDIC Insurance?

FDIC protects deposit products like:

- Checking accounts

- Savings accounts

- Money market deposit accounts (MMDAs)

- Certificates of deposit (CDs)

IRAs holding these qualify separately. Business operating accounts are covered too.

What FDIC Insurance Does NOT Cover

Not everything in a bank is protected:

- Stocks, bonds, mutual funds, annuities

- Life insurance policies

- Safe deposit box contents

- 401(k)s or investments (only cash equivalents like MMDAs)

For investments, SIPC offers separate protection up to $500,000 (cash $250,000) at brokerages.

Why FDIC Insurance Matters for Americans

In today's economy, with high-yield savings rates above 4% in 2026 and inflation concerns, more Americans park cash in banks. FDIC insurance builds trust, stabilizes the banking system, and protects against rare but devastating failures. Without it, we'd see panic withdrawals harming everyone.

For families saving for college, retirees on fixed incomes via Social Security, or small business owners, it means security. Recent events remind us: Don't assume government bailouts—structure accounts properly.

Practical Tips: How to Maximize Your FDIC Coverage

Follow these steps to insure more than $250,000:

- Spread Across Banks: $250,000 at Bank A, $250,000 at Bank B—fully covered.

- Use Ownership Categories: Single, joint, trust, IRA at one bank = multiples of $250,000.

- Add Names: Joint with spouse doubles coverage instantly.

- Check Bank Status: Use FDIC's BankFind tool at fdic.gov.

- For Businesses: Separate entity accounts; avoid insurance-only setups.

- Large Deposits? Consider CDARS or ICS networks for multi-bank coverage via one relationship.

Example: A couple with $1 million could insure it all at one bank via single ($250k each), joint ($500k), and trusts ($250k each).

Frequently Asked Questions

Related Articles

How to Handle "Identity Theft" in 2026: The First 24 Hours

Imagine checking your bank account on a quiet Saturday evening, only to discover unauthorized charges totaling thousands of dollars—or worse, spotting a new credit card opened in your name. In 2026, i...

The Best "Digital Banking" Apps for US Teens: A Parent's Guide

Imagine handing your teen a debit card that teaches them financial responsibility without the risk of overdrafts or debt. In 2026, digital banking apps make this possible, giving US parents powerful t...

The Best Online Banks with No Monthly Fees in 2026

Imagine ditching those pesky monthly bank fees that quietly eat into your budget every single month. In 2026, online banks make it easier than ever for Americans to enjoy truly free checking accounts...

How to Start an Emergency Fund from Scratch: $1 to $1;000

Picture this: Your car breaks down on the way to work, or an unexpected medical bill lands in your mailbox. Without a safety net, you're scrambling for credit cards or loans with sky-high interest rat...