How to Start an Emergency Fund from Scratch: $1 to $1;000

Picture this: Your car breaks down on the way to work, or an unexpected medical bill lands in your mailbox. Without a safety net, you're scrambling for credit cards or loans with sky-high interest rat...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Picture this: Your car breaks down on the way to work, or an unexpected medical bill lands in your mailbox. Without a safety net, you're scrambling for credit cards or loans with sky-high interest rates. But what if you could handle that $1,000 crisis with cash on hand? Starting an emergency fund from scratch—even with just $1—puts you in control, no matter your income level.

In 2026, with rising costs and economic uncertainty, only 47% of Americans can cover a $1,000 emergency from savings, according to recent surveys. The average unexpected expense? Closer to $1,700. This guide walks you through building that crucial $1 to $1,000 fund step by step, tailored for everyday Americans. You'll get practical tips, U.S.-specific tools like FDIC-insured accounts, and a roadmap to automate your way to financial peace.

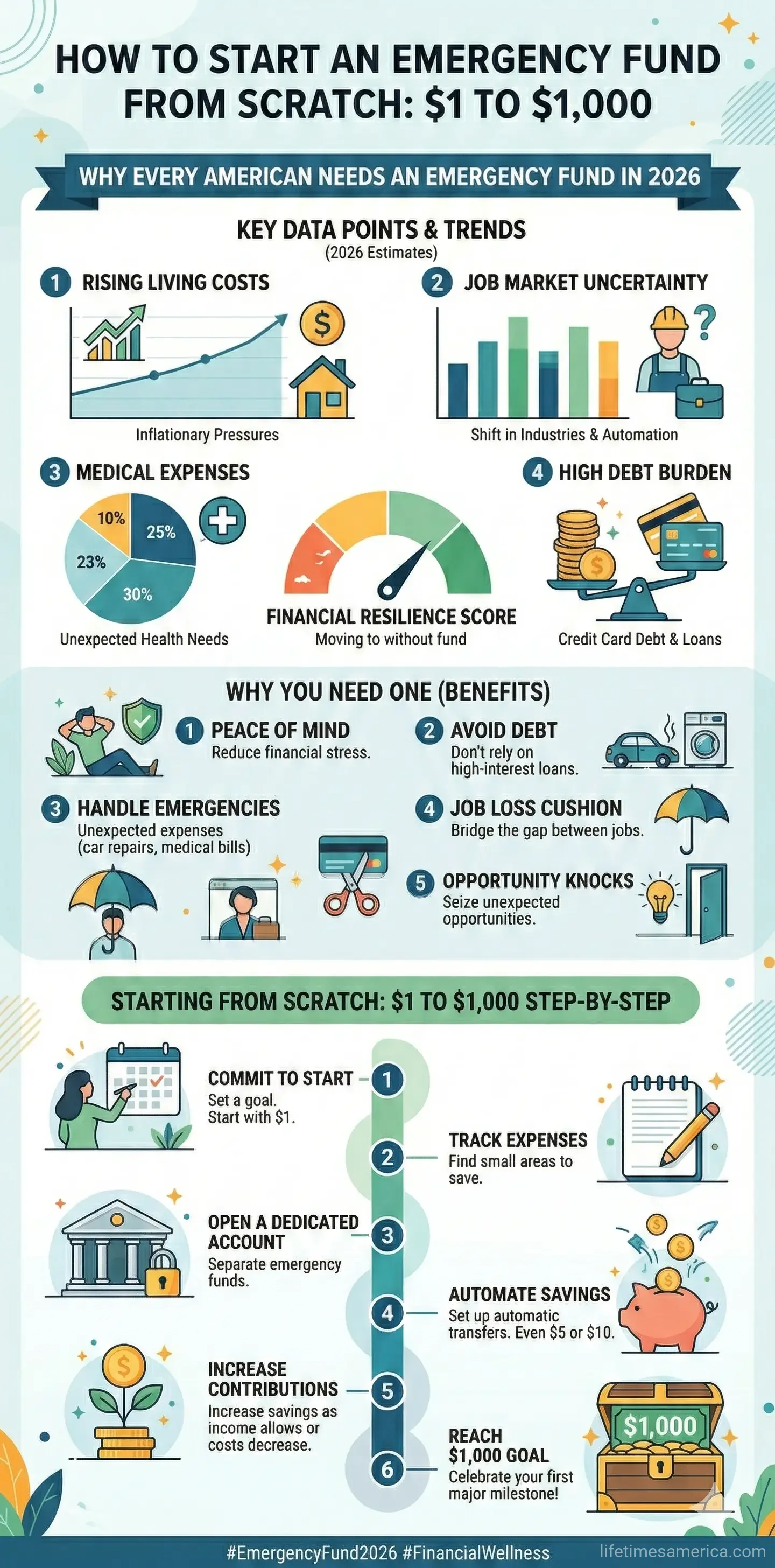

Why Every American Needs an Emergency Fund in 2026

Life throws curveballs: job layoffs, home repairs, or medical emergencies. Without a buffer, 53% of Americans turn to high-interest debt, prolonging financial stress. An emergency fund acts as your slack—cash separated from daily spending for true crises only.

In today's economy, with variable incomes common and job searches averaging longer than ever, this fund prevents reactive decisions like selling assets at a loss. For U.S. households, it's not just nice-to-have; it's essential amid Medicare gaps, 401(k) volatility, and state-specific costs like high auto insurance in Florida or Michigan.

Benefits Beyond the Obvious

- Peace of mind: Sleep better knowing you're covered for 3-6 months of essentials.

- Debt avoidance: Skip 20-30% APR credit cards; use cash instead.

- Better decisions: Time to job hunt without desperation.

- Compound growth: High-yield savings earn 4-5% APY in 2026, beating inflation.

How Much Should Your Starter Emergency Fund Be?

Don't aim for perfection—start with $1,000. This "starter fund" covers most immediate surprises like car repairs or ER visits, giving you breathing room to build more.

The gold standard? 3-6 months of essential expenses (rent, utilities, groceries, minimum debt payments—not vacations). Calculate yours:

- List monthly essentials: e.g., $2,000 for a single renter.

- Multiply by 3 ($6,000) or 6 ($12,000) based on stability.

Adjust for your life: Dual-income households lean toward 3 months; single earners with kids or gig workers need 6+. Use the IRS withholding estimator at irs.gov to maximize take-home pay from refunds.

Step-by-Step: Building from $1 to $1,000

Starting from zero? No problem. Follow this 30-60 day plan, inspired by proven roadmaps.

Step 1: Audit Your Cash Flow (Week 1)

Spend 30-60 minutes reviewing last 60 days' bank statements. Track every dollar using free tools like Mint or your bank's app. Identify leaks: subscriptions ($20/month Netflix?), dining out, impulse buys.

Actionable tip: Cancel 2-3 unused subscriptions—save $50/month instantly.

Step 2: Open Your Emergency Account (Day 1)

Choose FDIC-insured (up to $250,000) options for safety. Top 2026 picks:

- High-yield savings: 4.5-5% APY, instant access (Ally, Capital One, or credit unions via NCUA).

- Money market accounts: Check-writing access, stable yields.

- No fees, separate from checking: Label it "Emergency Fund" mentally.

Avoid stocks or crypto—liquidity is king (24-48 hour access).

Step 3: Set a Realistic Savings Goal with 50/30/20

Follow the 50/30/20 rule: 50% needs, 30% wants, 20% savings/debt. If paycheck-to-paycheck, start with windfalls like tax refunds (average $2,800 in 2026 per IRS data).

| Monthly Income Example | Needs (50%) | Wants (30%) | Savings (20%) |

|---|---|---|---|

| $4,000 take-home | $2,000 | $1,200 | $800 |

| Target for fund | - | Cut $200 | $300/month to fund |

Hit $1,000 in 3-4 months at $300/month.

Step 4: Cut Expenses Without Misery

- Downgrade cable ($20 save).

- Meal prep vs. takeout ($100/month).

- Shop sales via apps like Ibotta.

- Refinance auto loans if rates dropped (check bls.gov for CPI trends).

Step 5: Boost Income—High-Leverage Moves

Commit 5 hours/week to gigs: Uber, DoorDash, freelance on Upwork, or overtime. Direct 100% extra to your fund. Americans earn $500-1,000/month this way.

Step 6: Automate and Nudge Behavior

Set payroll direct deposit split or auto-transfers post-payday. Use apps like Acorns for round-ups—$1 becomes $1,000 faster. Track with a 12-month checklist:

| Month | Focus | Key Action |

|---|---|---|

| 1 | Audit & Setup | Open HYSA, auto-transfer $50. |

| 2 | Income Boost | Gig 5hrs/wk, all to fund. |

| 3 | Deep Cuts | Eliminate 1 big want. |

Best Places to Park Your Growing Emergency Fund

Keep 100% liquid and insured. Once at $1,000, ladder 25-40% into 3-month CDs (4%+ yields). Avoid mixing with daily cash—separate accounts only.

- HYSA: Top priority, no penalties.

- Money market: For larger sums.

- CD ladder: Post-$1,000 milestone.

Check usa.gov for FDIC locator; credit unions via ncua.gov.

Common Pitfalls and How to Avoid Them

Don't dip in for "wants"—only true emergencies. If you fall behind, restart with $1; consistency beats speed. Rebuild post-use immediately.

Frequently Asked Questions

You've got the blueprint: Start today with $1 in a high-yield savings account, automate transfers, and watch it grow to $1,000 and beyond. Track progress monthly, celebrate milestones, and adjust as life changes. Your future self—debt-free and stress-reduced—will thank you. Open that account now at your bank or credit union, and take the first step toward unbreakable financial security.

Sources & References

-

1

Build Emergency Fund 2026: How Americans Can Save $10,000 — abhyashsuchi.in

-

2

How to Build an Emergency Fund in 2026: A Step-by-Step Guide — useorigin.com

-

3

How to build an emergency fund for 2026 | Rocket Loans — www.rocketloans.com

-

4

Yes, You Need An Emergency Fund. Here's How To Start In 2026 — hermoney.com

-

5

Best Places to Keep Your Emergency Fund in 2026 | Thrivent — www.thrivent.com

-

6

Your 2026 Financial Roadmap | iTHINK Financial — www.ithinkfi.org

-

7

IRS Withholding Estimator — www.irs.gov

-

8

Find FDIC-Insured Banks — www.usa.gov

-

9

NCUA Credit Union Locator — www.ncua.gov

-

10

BLS Consumer Expenditure Survey — www.bls.gov

Related Articles

How to Handle "Identity Theft" in 2026: The First 24 Hours

Imagine checking your bank account on a quiet Saturday evening, only to discover unauthorized charges totaling thousands of dollars—or worse, spotting a new credit card opened in your name. In 2026, i...

The Best "Digital Banking" Apps for US Teens: A Parent's Guide

Imagine handing your teen a debit card that teaches them financial responsibility without the risk of overdrafts or debt. In 2026, digital banking apps make this possible, giving US parents powerful t...

The Best Online Banks with No Monthly Fees in 2026

Imagine ditching those pesky monthly bank fees that quietly eat into your budget every single month. In 2026, online banks make it easier than ever for Americans to enjoy truly free checking accounts...

The Best High-Yield Savings Accounts (HYSA) in the US Right Now

Imagine watching your emergency fund or vacation savings grow faster than ever, all while keeping your money safe and accessible. In 2026, high-yield savings accounts (HYSAs) offer APYs up to 5.00%—ov...