Online Banks vs Traditional Banks: Which Is Better for You?

Imagine checking your bank balance at 2 a.m., transferring funds in seconds, or earning double the interest on your savings—all without leaving your couch. That's the promise of online banks, but trad...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine checking your bank balance at 2 a.m., transferring funds in seconds, or earning double the interest on your savings—all without leaving your couch. That's the promise of online banks, but traditional banks still draw crowds with their familiar branches and face-to-face service. In 2026, choosing between online banks vs traditional banks boils down to your lifestyle, needs, and comfort with digital tools.

As Americans navigate rising costs and busy schedules, understanding these options helps you pick the best fit. Both types are federally insured up to $250,000 per depositor through the FDIC, ensuring your money's safety regardless of choice. Let's break down the key differences, pros, cons, and real-world examples to see which is better for you.

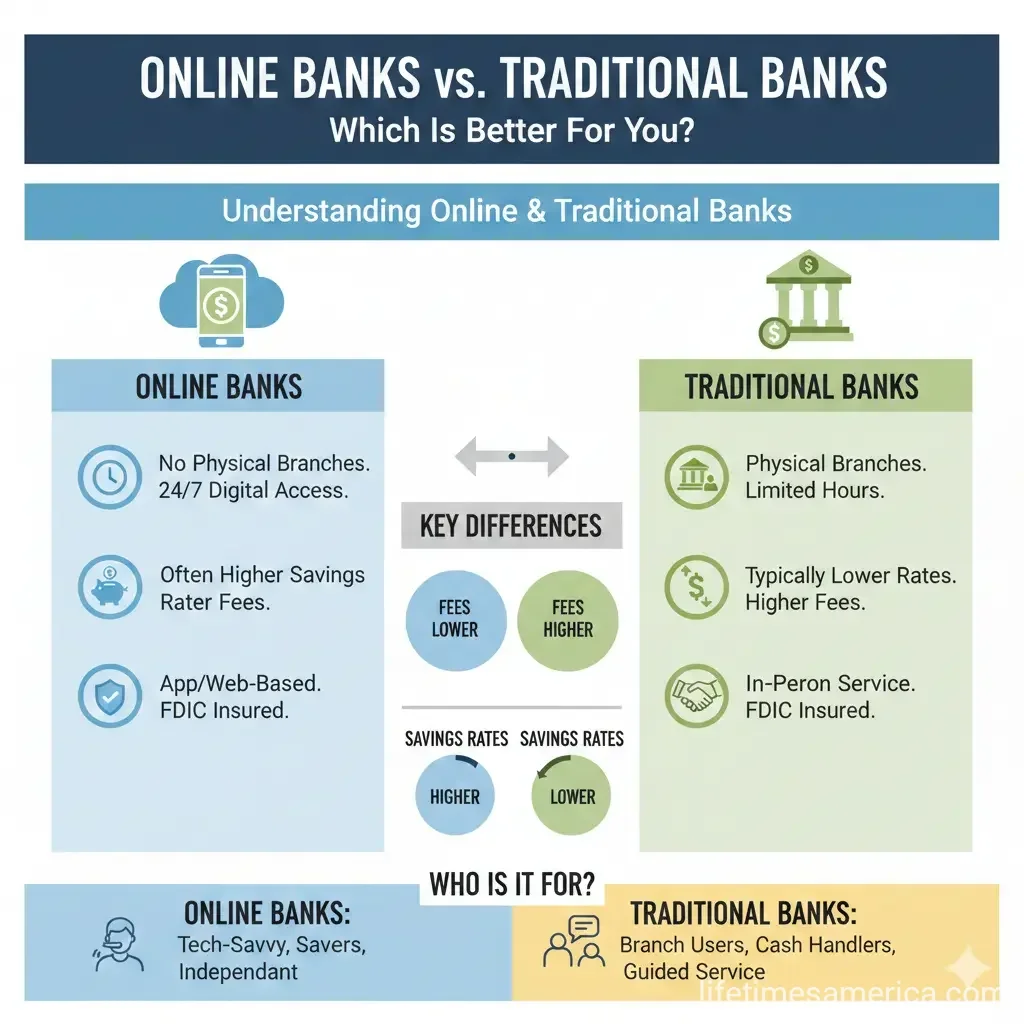

Understanding Online Banks and Traditional Banks

Traditional banks, like Chase or Bank of America, maintain physical branches across the U.S., blending in-person service with digital apps. Online banks, such as Ally, Chime, or Marcus by Goldman Sachs, operate entirely digitally, skipping branches to cut costs.

What Makes a Bank "Traditional"?

These institutions offer brick-and-mortar locations for deposits, withdrawals, and advice. You'll find ATMs nationwide and services like notary or safe deposit boxes. Even in 2026, they invest heavily in apps—Chase's mobile platform, for instance, rivals many online tools.

The Rise of Online-Only Banks

Online banks leverage technology for 24/7 access via apps with features like mobile check deposits and instant notifications. Without branch overhead, they pass savings to you through better rates and fewer fees.

Pros and Cons of Traditional Banks

Traditional banks shine for those who value personal touch and cash handling, but they come with trade-offs.

Key Pros

- Large ATM networks and easy cash deposits/withdrawals: Deposit cash at branches or thousands of ATMs without fees.

- In-person support: Speak to a teller for complex issues, notary services, or large transactions.

- Wide product range: From 401(k)s to business loans and mortgages, all under one roof.

- Advanced digital tools: Big players like Citi offer seamless apps alongside branches.

Key Cons

- Higher fees: Monthly maintenance, overdraft, and out-of-network ATM charges add up.

- Lower APYs: Savings rates often lag behind online competitors.

- Limited hours: Branches close evenings and weekends, though ATMs help.

For example, if you're a small business owner depositing daily cash from sales, a traditional bank like Wells Fargo makes life easier.

Pros and Cons of Online Banks

Online banks appeal to tech-savvy users seeking efficiency and earnings, but they aren't for everyone.

Key Pros

- Higher interest rates: In 2026, online savings APYs are often 4-5x higher than traditional banks, thanks to no branch costs.

- Low or no fees: Skip monthly charges; many reimburse ATM fees nationwide.

- Superior apps and 24/7 access: User-friendly interfaces with real-time alerts and quick transfers.

- Competitive loans: Personal loans under 6% APR, vs. over 10% at traditional banks.

Key Cons

- No cash deposits: Many charge fees or don't accept cash; use partner ATMs for withdrawals.

- Limited support: Phone, chat, or email only—no branch visits.

- Fewer services: Less emphasis on in-person needs like cashier's checks.

Take Ally Bank: It offers high-yield savings and no-fee checking, ideal for remote workers building emergency funds.

Key Differences: Online Banks vs Traditional Banks Comparison

Here's a side-by-side look at how they stack up in 2026:

| Feature | Traditional Banks | Online Banks |

|---|---|---|

| Branches | Yes, nationwide networks | No physical locations |

| Savings APY | Lower (e.g., 0.01-1%) | Higher (e.g., 4-5%+) |

| Fees | Higher (maintenance, overdraft) | Low/none, ATM reimbursements |

| Cash Handling | Easy deposits/withdrawals | Limited or fee-based |

| Customer Service | In-person + digital | Phone/chat 24/7 |

| Security | FDIC-insured + branches | FDIC-insured + encryption |

Security is equal: Both use multifactor authentication and FDIC protection. Traditional banks edge out for new account openers—48% prefer them for in-person options.

Which Is Better for You? Factors to Consider

No one-size-fits-all—match to your habits:

- Choose traditional if: You handle cash often, need face-to-face advice, or want diverse services like IRS-linked loans.

- Choose online if: You're digital-first, prioritize earnings, or live far from branches. Great for millennials (35% prefer digital).

- Hybrid approach: Use a traditional bank for checking/cash and online for high-yield savings.

Practical tip: Check FDIC's BankFind tool at fdic.gov to verify insurance and read reviews on sites like Bankrate.

U.S.-Specific Considerations and Regulations

All U.S. banks follow federal rules: FDIC insures deposits to $250,000, and the CFPB oversees fair practices. Online banks must partner with FDIC-insured entities if not banks themselves (e.g., Chime via The Bancorp Bank). In 2026, expect Reg E protections for electronic transfers, limiting fraud liability to $50 if reported promptly.

For taxes, both issue 1099-INT forms—link to IRS Free File for easy filing.

Top Examples in 2026

- Traditional: Chase (vast branches, robust app), Bank of America (Medicare-linked services).

- Online: Ally (top checking/savings), SoFi (high satisfaction), Marcus (low-loan fees).

Next Steps: Make the Right Choice for Your Finances

Assess your needs: Tally cash deposits, preferred service style, and savings goals. Compare rates on Bankrate.com, verify FDIC status, and test apps with small transfers. Many switchers keep both for flexibility—start with a high-yield online savings alongside your traditional checking. Your money works harder when you choose wisely.

Frequently Asked Questions

Sources & References

-

1

Brick-And-Mortar Banks Vs. Online Banks: Pros And Cons | Bankrate — www.bankrate.com

-

2

Online Banks vs. Traditional Banks: Pros & Cons in 2026 | Breeze — www.meetbreeze.com

-

3

Online Banks vs. Traditional Banks - SmartAsset.com — smartasset.com

-

4

Neo Banks vs Traditional Banks vs Fintechs: The Complete 2026 Guide | Bleap — www.bleap.finance

-

5

Traditional Banks vs. Online Banking | Citi.com — www.citi.com

-

6

9 Best Online Checking Accounts for 2026 - NerdWallet — www.nerdwallet.com

-

7

How Traditional Institutions Can Beat Neobanks at Customer Acquisition | The Financial Brand — thefinancialbrand.com

Useful Tools

Related Articles

How to Handle "Identity Theft" in 2026: The First 24 Hours

Imagine checking your bank account on a quiet Saturday evening, only to discover unauthorized charges totaling thousands of dollars—or worse, spotting a new credit card opened in your name. In 2026, i...

The Best "Digital Banking" Apps for US Teens: A Parent's Guide

Imagine handing your teen a debit card that teaches them financial responsibility without the risk of overdrafts or debt. In 2026, digital banking apps make this possible, giving US parents powerful t...

The Best Online Banks with No Monthly Fees in 2026

Imagine ditching those pesky monthly bank fees that quietly eat into your budget every single month. In 2026, online banks make it easier than ever for Americans to enjoy truly free checking accounts...

How to Start an Emergency Fund from Scratch: $1 to $1;000

Picture this: Your car breaks down on the way to work, or an unexpected medical bill lands in your mailbox. Without a safety net, you're scrambling for credit cards or loans with sky-high interest rat...