How to Get a Small Business Loan in the USA

Getting a small business loan in the USA doesn't have to be overwhelming, even if you're worried about your credit score or just starting out. Whether you're looking to launch a new venture, expand yo...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Getting a small business loan in the USA doesn't have to be overwhelming, even if you're worried about your credit score or just starting out. Whether you're looking to launch a new venture, expand your existing business, or purchase equipment, there are several loan options available—including government-backed programs that are specifically designed to help small business owners succeed. We'll walk you through everything you need to know to get approved.

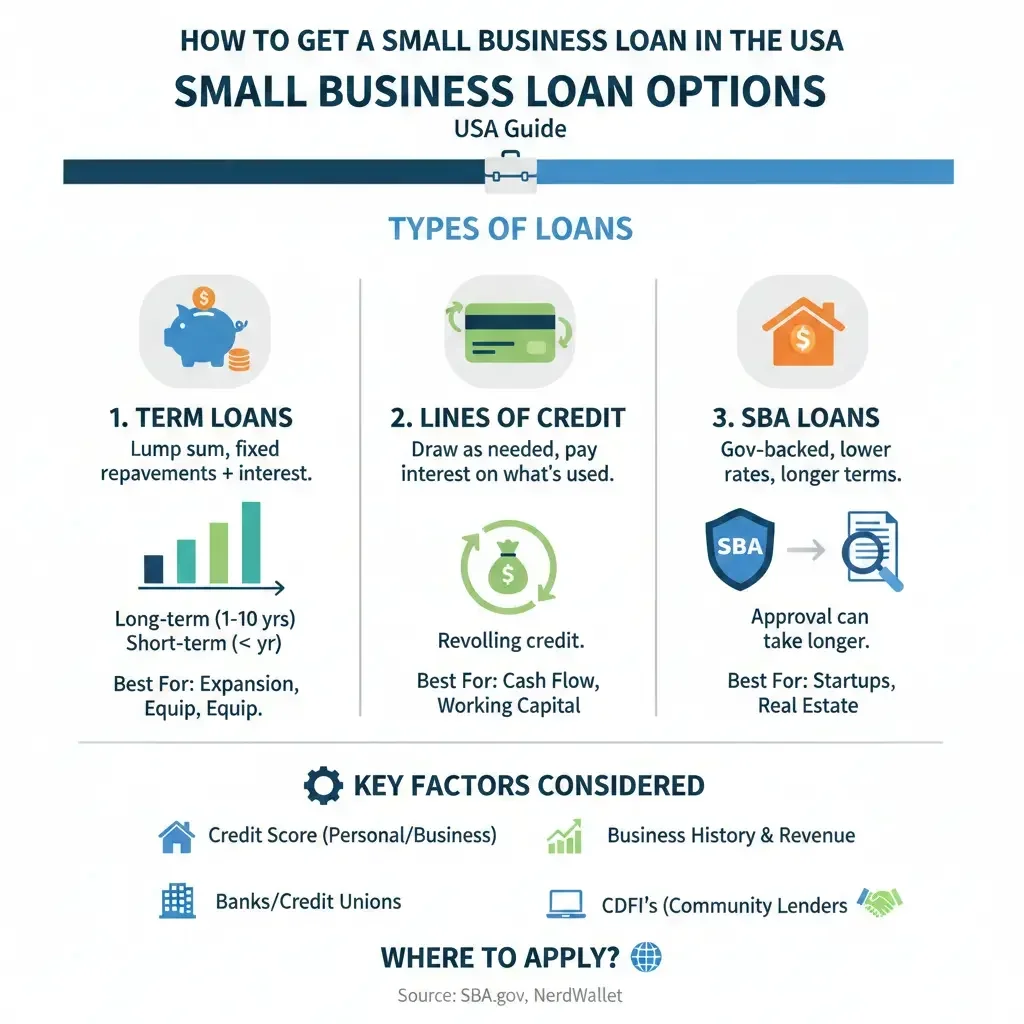

Understanding Your Small Business Loan Options

The most popular small business loans come from the U.S. Small Business Administration (SBA), which backs loans through participating lenders rather than lending money directly. The two most common SBA programs are 7(a) loans and 504 loans.

SBA 7(a) loans are the most flexible option, allowing you to borrow up to $5 million for working capital, refinancing debt, purchasing equipment, and buying or upgrading real estate and buildings. 504 loans are specifically designed for purchasing real estate and equipment, with loan amounts generally up to $5.5 million depending on your industry.

If your business operates in a rural area, you might also qualify for a USDA B&I loan, which can provide up to $25 million for startup costs, expansion, equipment purchases, and working capital.

Core SBA Loan Eligibility Requirements for 2026

Before you apply for any SBA loan, your business must meet baseline eligibility criteria. These requirements are set by the SBA and apply across all their loan programs.

Business Requirements

Your business must meet all of these operational criteria:

- Be an operating, for-profit business that's legally registered and operating in compliance with applicable laws

- Be located in and primarily operating in the United States (if you operate internationally, loan proceeds can only be used for U.S. operations)

- Be authorized to do business in the state or territory where you're applying for a loan

- Meet the SBA's definition of a "small" business based on your industry's size standards

- Operate in an SBA-eligible industry (speculative, illegal, and nonprofit businesses are ineligible)

Financial and Tax Compliance

Your business must also demonstrate financial responsibility:

- Be current on all government debt obligations, including prior SBA loans

- Not have defaulted on federal debt that resulted in a loss to the government

- Be current on all federal, state, and local taxes with required tax filings completed

- Have no federal loan defaults (being 90+ days late on federal student loans or government-backed mortgages disqualifies you)

Personal Requirements for Owners

As of December 19, 2025, the SBA requires 100% of business owners to be U.S. citizens or verified legal permanent residents and to have their chief residence in the United States or its territories. Additionally:

- No owner may be incarcerated, on parole or probation, or under indictment for a felony or crime involving moral turpitude

- All owners must actively work in the business and invest their own time or money

- All owners must be entered into the SBA's ETRAN system for full transparency

Financial Qualifications for SBA 7(a) Loans

If you're pursuing an SBA 7(a) loan specifically, you'll need to meet additional financial thresholds:

- Fewer than 500 employees (for manufacturing and mining industries)

- Less than $7.5 million in average annual revenue for the past three years

- Net income under $5 million (after taxes, not counting carry-over losses)

- Tangible net worth less than $15 million

In practice, banks generally prefer businesses with minimum annual gross revenues exceeding $250,000, though this represents a practical lending threshold rather than an official SBA requirement. Some lenders may consider businesses with $150,000–$250,000 in revenue for smaller loan amounts or microloans, but approval becomes significantly more challenging below this range.

Credit Score and Personal Financial Requirements

While the SBA doesn't set a minimum credit score requirement, lenders typically evaluate your personal financial standing as part of the approval process. Banks generally require:

- Credit score of 690 or higher (good to excellent credit)

- Preferably above 680 for SBA 7(a) loans

- Freedom from recent bankruptcies, foreclosures, or tax liens

- Strong personal finances demonstrating your ability to repay

Even those with less-than-perfect credit may still qualify for SBA loans, but you'll likely face higher interest rates or stricter collateral requirements.

The SBA Loan Application Process

Step 1: Prepare Your Documentation

Gather the paperwork lenders will request:

- Copies of your business license and lease

- Financial statements, including profit-and-loss statements

- Personal and business tax returns (typically 2–3 years)

- Bank statements

- Proof of business ownership and personal identification

- A detailed business plan explaining how you'll use the loan funds

Step 2: Explore Financing Alternatives

The SBA requires that you demonstrate you've tried and failed to obtain funds from other financial lenders, fully exhausting non-SBA loan options. This means approaching traditional banks and credit unions first. Document these rejections, as they strengthen your SBA application.

Step 3: Choose Your Lender

Apply through an SBA-approved lender, which includes banks, credit unions, and online lenders. Different lenders may have varying underwriting standards beyond the baseline SBA requirements, so it's worth comparing options.

Step 4: Submit Your Application

You'll typically need to provide detailed paperwork, and some lenders may require you to apply in person. Be prepared to explain your business purpose and how you'll use the loan funds—the SBA requires a sound business purpose with intended fund usage approved by the SBA.

Step 5: Prepare for Personal Guarantees and Collateral

Lenders will likely require a personal guarantee from you and possibly collateral to secure the loan. This means you're personally liable for repaying the loan if your business can't.

Important 2026 Updates to Know

Recent changes to SBA lending rules affect your eligibility and application process:

- As of February 28, 2026, the SBA removed the Small Business Sustainability Screening (SBSS) requirement for 7(a) loans under $350,000, streamlining the approval process for smaller loans

- All owners must now be entered into ETRAN (the SBA's electronic system) with full transparency

- New residency requirements mean all owners must reside within the United States, eliminating silent ownership structures

Practical Tips for Getting Approved

- Start early: Gather your financial documents and tax returns before applying. Lenders need 2–3 years of history to evaluate your business.

- Improve your credit: If your score is below 690, spend time paying down debt and making on-time payments before applying.

- Have a solid business plan: Clearly explain what you'll do with the loan funds and how it'll help your business grow or operate more efficiently.

- Show personal investment: Demonstrate that you've invested your own time and money into the business. Lenders want to see you have "skin in the game."

- Stay current on obligations: Pay all taxes, government loans, and business debts on time. Even one late payment can disqualify you.

- Consider a co-signer: If you're concerned about approval, having a co-signer with stronger finances can improve your chances.

Your Next Steps

Getting a small business loan starts with understanding whether you meet the baseline SBA requirements. Review the eligibility criteria above and gather your financial documentation. If you're not quite ready yet—perhaps your credit needs improvement or your business needs more time to establish revenue—create a timeline for addressing those gaps.

Visit the official SBA website to learn more about specific loan programs and find an SBA-approved lender near you. The SBA also offers free business counseling through SCORE mentors and Small Business Development Centers, which can help you strengthen your application and business plan before you apply.

Remember, meeting eligibility requirements doesn't guarantee approval—lenders will evaluate your specific situation, business plan, and financial health. But with solid preparation and a clear understanding of what lenders are looking for, you'll be well-positioned to secure the funding your business needs to grow.

Frequently Asked Questions

Sources & References

-

1

SBA Loan Eligibility Requirements (2026) - Lendio — www.lendio.com

-

2

SBA Loan Guide: Requirements, Types and Application Process - First Citizens — www.firstcitizens.com

-

3

SBA 7(a) Loans: Borrower Qualifications in 2026 — www.sba7a.loans

-

4

SBA Loan Requirements 2026: How to Get Approved for an SBA Loan — www.fastwaysba.com

-

5

Business Loan Requirements: What You Need to Qualify - NerdWallet — www.nerdwallet.com

-

6

SBA Loans Explained: Complete Small Business Guide (2026) — www.peoplesbankmtg.com

- 7

-

8

Loans - U.S. Small Business Administration — www.sba.gov

- 9

Related Articles

How to Use a "Qualified Small Business Stock" (QSBS) to Pay Zero Tax

If you're an investor, entrepreneur, or employee at a startup, you've probably heard the phrase "tax-free gains" and thought it sounded too good to be true. But there's actually a legitimate way to po...

How to Claim the "Employee Retention Credit" (ERC) in 2026: Is it Still Possible?

Imagine discovering tens of thousands of dollars in your business's pocket—funds you earned by keeping employees on payroll during the toughest days of the COVID-19 crisis. That's the promise of the E...

The Best "Virtual" Business Addresses for US LLCs in 2026

Starting a limited liability company (LLC) in 2026 means navigating smart choices for privacy, professionalism, and compliance. One key decision is picking the right business address—especially if you...

How to Transition from W-2 to Self-Employed: A Financial Checklist

Making the leap from a steady W-2 paycheck to self-employment is exciting—and terrifying. You're trading the security of regular income and employer benefits for freedom and control over your work. Bu...