What Is a CD (Certificate of Deposit) and Is It Worth It?

Imagine parking your money in a safe spot where it earns a steady return, protected from market ups and downs—that's the promise of a Certificate of Deposit, or CD. In today's shifting rate environmen...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine parking your money in a safe spot where it earns a steady return, protected from market ups and downs—that's the promise of a Certificate of Deposit, or CD. In today's shifting rate environment, many Americans are wondering if CDs still make sense for their savings goals.

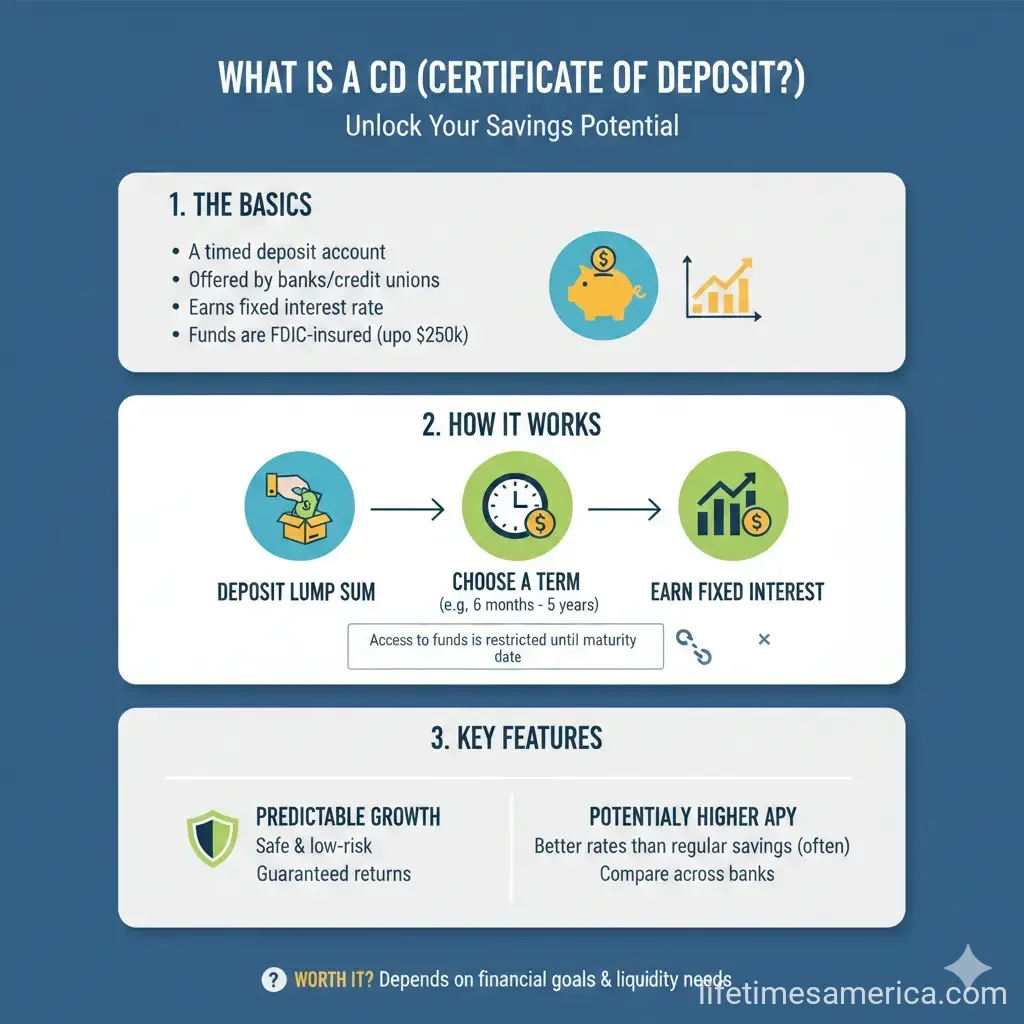

What Is a Certificate of Deposit (CD)?

A Certificate of Deposit (CD) is a type of savings account where you deposit a fixed amount of money for a set period, such as six months to five years, and the bank pays you interest in return. Unlike a regular savings account, your funds are locked in until the maturity date, when you get back your principal plus earned interest.

CDs are issued by banks, credit unions, and brokerage firms, and they're considered one of the safest savings options available to Americans. The Federal Deposit Insurance Corporation (FDIC) insures CDs up to $250,000 per depositor, per insured bank, for each account ownership category, covering all accounts in your name at that bank. This protection means your money is secure even if the bank fails, as long as it's within the limits.

How Do CDs Work?

When you open a CD, you choose a term length—anywhere from 30 days to 10 years—and deposit the minimum required amount, often starting at $500 or $1,000. The bank offers a fixed interest rate, which is typically higher than what you'd get from a standard savings account because you're committing your money for longer.

Interest can be paid out monthly, quarterly, or at maturity, and it's compounded in some cases to grow your earnings. At maturity, you have options: withdraw the funds, roll them over into a new CD, or let it auto-renew. For example, a popular strategy is a CD ladder—opening multiple CDs with staggered terms like one-year, two-year, up to five-year—so one matures each year for ongoing access.

Types of CDs Available in 2026

- Traditional CDs: Fixed rate and term, with early withdrawal penalties.

- Bump-up CDs: Allow you to request a higher rate if market rates rise during the term.

- No-penalty CDs: Let you withdraw early without fees after an initial period, offering more flexibility.

- Brokered CDs: Bought through brokerage firms, sometimes with higher rates negotiated in bulk.

Some banks, like those offering variable rates on longer terms, even allow partial withdrawals up to 50% of principal after six months without penalty on select products.

Current CD Rates and Trends in 2026

As of February 2026, top CD rates are up to 4.50% APY for various terms, though they've softened from peaks in 2023 due to Federal Reserve rate cuts. For instance, you might lock in just under 4% on a three-year CD, providing stability amid expected further cuts.

Rates are influenced by the federal funds rate set by the U.S. Federal Reserve, which guides lending across the economy. Online banks and credit unions often beat traditional banks with competitive APYs and low minimums, like $500 deposits. Always check disclosures for fixed vs. variable rates, payment schedules, and maturity details.

Pros and Cons of CDs

CDs offer predictable growth but come with trade-offs. Here's a clear breakdown:

| Pros | Cons |

|---|---|

| Higher rates than savings accounts—often the best among bank products. | Early withdrawal penalties, typically several months' interest. |

| Fixed rates lock in earnings, protecting against rate drops. | Limited liquidity—can't add funds or access easily until maturity. |

| FDIC-insured up to $250,000 for principal safety. | May lag inflation, reducing real returns over time. |

| Easy to calculate returns in advance. | Opportunity cost if stocks or other investments outperform. |

Is a CD Worth It in 2026?

Yes, CDs are worth it if you have money you won't need soon and want guaranteed returns amid uncertainty. They're ideal for medium-term goals like a home down payment or retirement supplement, especially with rates around 4% still beating many savings accounts. Experts recommend locking in now for terms over 12 months to hedge against further Fed cuts.

However, they're not for emergency funds—high-yield savings accounts offer similar rates (around 4% APY) with full liquidity and no penalties. CDs shine for those trading flexibility for higher, fixed yields, but compare to inflation (hovering around 2-3% recently) to ensure real growth.

When CDs Make the Most Sense

- You're saving for a known expense in 6-60 months.

- Rates are attractive compared to alternatives.

- You prioritize safety over high-risk investments like stocks.

- Building a ladder for steady income, such as in retirement.

When to Skip CDs

- Need quick access to cash.

- Expect inflation to outpace rates.

- Prefer variable rates that could rise.

How to Open a CD: Step-by-Step Guide

- Assess your goals: Match term to when you'll need funds.

- Shop rates: Use bank comparison sites for top APYs from FDIC-insured institutions.

- Choose type: Traditional for max rate, bump-up or no-penalty for flexibility.

- Verify insurance: Confirm FDIC coverage up to $250,000 via fdic.gov.

- Open online or in-branch: Provide ID, SSN, and deposit funds (often via transfer).

- Plan maturity: Set alerts for renewal options.

Minimums vary—many online banks start at $500, making CDs accessible.

CDs vs. Other Savings Options

| Feature | CD | High-Yield Savings | Money Market Account |

|---|---|---|---|

| Rate Type | Fixed | Variable | Variable |

| Liquidity | Low (penalties) | High | High (limited transactions) |

| Insurance | FDIC up to $250k | FDIC up to $250k | FDIC up to $250k |

| Best For | Locked savings | Emergency funds | Checking-like savings |

Next Steps to Maximize Your Savings

Review your financial goals and compare current rates from multiple FDIC-insured banks. If you're sitting on a maturing CD, consider rolling it into a longer-term option or a high-yield savings for liquidity. Tools like the FDIC's Electronic Deposit Insurance Estimator help ensure full coverage. Start small with a ladder to test the waters—your future self will thank you for that protected growth.

Frequently Asked Questions

Sources & References

-

1

Certificates of Deposit (CDs) - Investor.gov — www.investor.gov

-

2

What is a Certificate of Deposit? - TD Bank — www.td.com

- 3

-

4

Best CD Rates for February 2026: Up to 4.50% - NerdWallet — www.nerdwallet.com

- 5

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...