High-Yield Savings vs Investing: Where Should You Put Your Money?

When you've got money to grow, the choice between a high-yield savings account and investing can feel overwhelming. Both options promise growth, but they work in fundamentally different ways. Understa...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

When you've got money to grow, the choice between a high-yield savings account and investing can feel overwhelming. Both options promise growth, but they work in fundamentally different ways. Understanding the differences—and knowing which aligns with your financial goals—is crucial to making the right decision for your situation.

Understanding High-Yield Savings Accounts

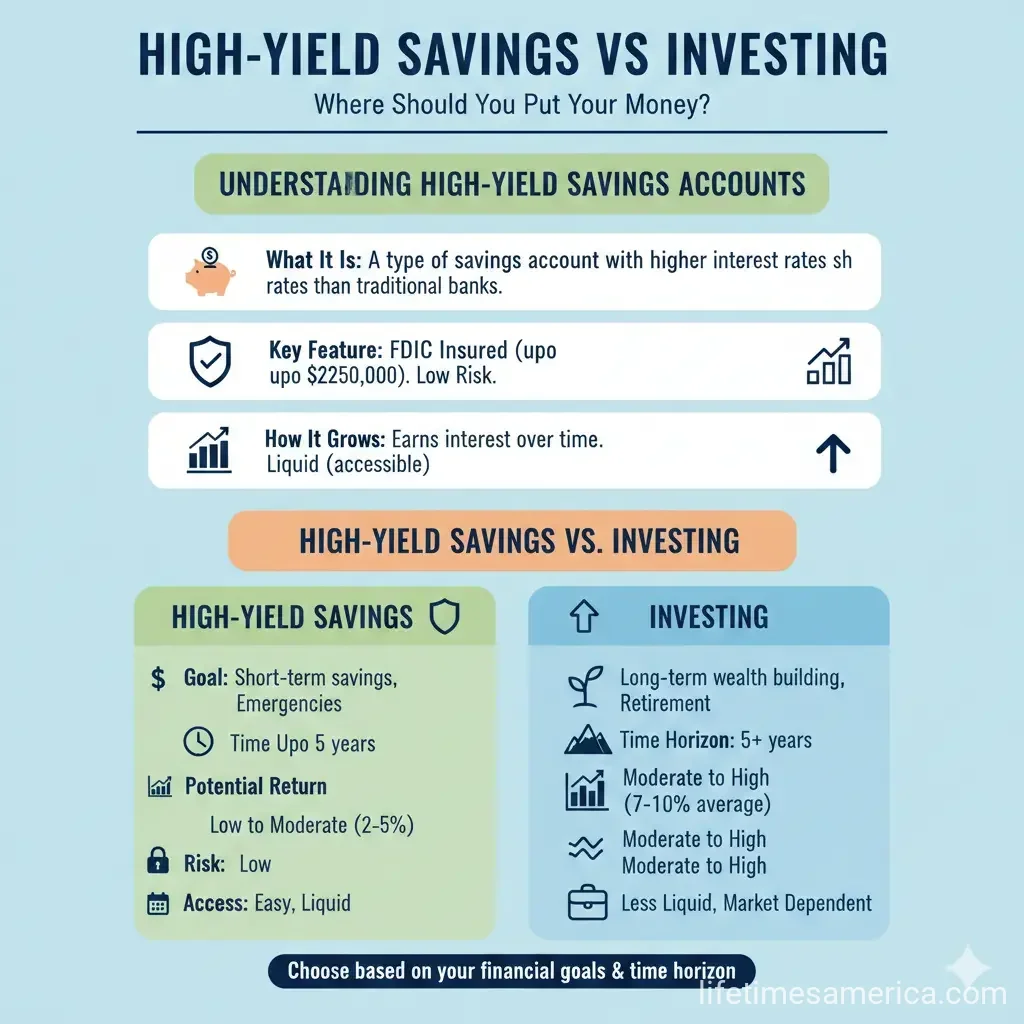

A high-yield savings account (HYSA) is a bank account that pays you interest on your cash balance, typically through an online bank or financial institution. Unlike traditional savings accounts at brick-and-mortar banks, HYSAs offer significantly higher interest rates, currently ranging from 3% to 4% or higher in 2026.

Here's how they work: You deposit your money, and the bank pays you interest on that balance. The interest rate remains relatively consistent, and your account is FDIC-insured up to $250,000, which means your deposits are protected by federal insurance if the bank fails. You can access your money whenever you need it, making HYSAs highly liquid.

Who Should Use a High-Yield Savings Account?

HYSAs work best for several situations:

- Emergency funds: A high-yield savings account is an ideal place to stash your emergency savings since you can access the money quickly without penalty.

- Short-term goals: If you're saving for something within the next few months or years—like a home down payment, wedding, or vacation—an HYSA helps your money grow while staying accessible.

- Risk-averse investors: If the thought of market volatility keeps you up at night, HYSAs offer peace of mind because you won't lose your principal investment.

- Current savings: If you have cash sitting in a traditional savings account earning minimal interest, moving it to an HYSA is a practical first step toward better returns.

The Case for Investing

Investing involves purchasing assets—stocks, bonds, mutual funds, or index funds—with the goal of increasing their value over time. Unlike savings accounts, investing offers the potential for significantly higher returns, but it comes with trade-offs: your money isn't guaranteed to grow, and you could lose your principal investment.

The historical long-term average annualized return for the S&P 500 index is approximately 10%, which substantially outpaces high-yield savings accounts. However, these returns aren't guaranteed, and they fluctuate year to year based on market conditions.

Types of Investments to Consider

Stock Index Funds: An S&P 500 index fund provides broad, diversified exposure to the U.S. stock market and is an excellent choice for beginning investors who can stay invested for at least three to five years. These funds track the performance of 500 large-cap American companies.

Bonds and Bond Funds: Bond mutual funds or index funds typically offer returns of 3% to 4% for U.S. government bonds, with higher yields available for riskier corporate bonds. Bonds are generally less volatile than stocks but offer lower growth potential.

Dividend Stocks: Some investors build portfolios around dividend-paying stocks, though it's important to focus on companies with a solid history of dividend increases rather than just the highest current yield.

Who Should Invest?

Investing makes sense when:

- You have a long time horizon: Investing is more suitable for goals that are years or even decades away, such as retirement. The longer you stay invested, the more time your money has to weather market ups and downs.

- You can tolerate volatility: Your investments will fluctuate in value. If you can handle seeing your account balance go up and down without panic-selling, you're better positioned for investing.

- You're building long-term wealth: Whether it's retirement savings through a 401(k), an IRA, or a taxable brokerage account, investing helps you accumulate wealth over decades.

- You want to outpace inflation: High-yield savings accounts at 4% may lose purchasing power if inflation runs higher, whereas historically, stocks have beaten inflation over the long term.

High-Yield Savings vs. Investing: Direct Comparison

Let's look at how these options stack up across key factors:

| Factor | High-Yield Savings Account | Investing |

|---|---|---|

| Typical Returns | 3% to 4%+ annually | S&P 500 average: ~10% annually (historical) |

| Risk Level | Very low (FDIC-insured up to $250,000) | Moderate to high (depends on asset type) |

| Liquidity | Highly accessible; withdraw anytime | Varies; some assets take time to sell |

| Best Time Horizon | Months to a few years | 3+ years, ideally decades |

| Inflation Protection | Modest; may lose purchasing power if rates fall | Better long-term inflation protection |

| Guaranteed Returns | Yes, fixed interest rate | No; returns fluctuate and aren't guaranteed |

Real-World Example: $40,000 Comparison

Let's say you have $40,000 to put away. Here's how a high-yield savings account compares to a CD (which offers a fixed rate):

- 3-month CD at 3.90%: Earns $384.42 vs. a 4.20% HYSA earning $413.54—the HYSA wins by $29.12.

- 6-month CD at 4.10%: Earns $811.76 vs. a 4.20% HYSA earning $831.36—the HYSA wins by $19.60.

- 1-year CD at 4.10%: Earns $1,640 vs. a 4.20% HYSA earning $1,680—the HYSA wins by $40.

In 2026, HYSAs are currently competitive with or outperforming CDs. However, if you invested that same $40,000 in an S&P 500 index fund and saw historical average returns of 10%, you'd earn approximately $4,000 in year one—though with no guarantee and potential for losses.

The Inflation Factor

One critical consideration: inflation. While high-yield savings accounts are considered safe investments, you run the risk of losing purchasing power over time if the interest rate is lower than inflation. In September 2025, inflation was running at about 3%. If your HYSA earns 4% but inflation is 3%, your real return is only about 1%.

This is where investing has a historical advantage. Stocks, particularly diversified index funds, have historically outpaced inflation over the long term, helping preserve and grow your purchasing power.

Interest Rate Sensitivity

An important distinction: high-yield savings accounts are sensitive to Federal Reserve rate changes. When the Fed cuts rates, HYSA yields typically decrease. CDs, by contrast, lock in a fixed rate until maturity, making them appealing if you expect rates to fall.

This matters in 2026 because if the Fed continues cutting rates, your HYSA earnings could decline, while a CD would maintain its guaranteed rate for the full term.

A Balanced Approach: Combining Both Strategies

You don't have to choose one or the other. Many Americans use both strategies simultaneously:

- Emergency fund: Keep 3-6 months of expenses in a high-yield savings account for quick access.

- Short-term goals: Use HYSAs for money you'll need within 1-3 years.

- Retirement savings: Invest through a 401(k) (especially if your employer matches contributions) or an IRA.

- Long-term wealth building: Use a taxable brokerage account for goals beyond retirement.

This diversified approach gives you safety, liquidity, and growth potential all at once.

Making Your Decision

The choice between high-yield savings and investing isn't either-or—it's about matching your strategy to your timeline and risk tolerance. High-yield savings accounts offer safety, liquidity, and respectable returns for short-term goals and emergency funds. Investing offers higher growth potential for long-term wealth building, but requires patience and the ability to weather market volatility.

Start by assessing your financial situation: How much do you have to invest? When will you need the money? How comfortable are you with risk? Your answers will guide you toward the right choice—or the right combination of both.

Whatever you decide, the most important step is taking action. Money sitting idle in a low-interest account is definitely working against you. Whether you open a high-yield savings account today or start investing for retirement, you're moving in the right direction.

Frequently Asked Questions

Sources & References

- 1

-

2

High-Yield Savings Account (HYSA) vs. Investing — www.chase.com

-

3

10 Best Investments For 2026 — www.bankrate.com

-

4

11 Best Investments for 2026 — www.nerdwallet.com

-

5

Saving vs. Investing: What's the Difference? — www.usbank.com

Useful Tools

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...