The 10 Best Index Funds for Your 401(k) in 2026

Building a solid 401(k) portfolio doesn't have to be complicated. If you're looking for a straightforward way to grow your retirement savings with low fees and consistent performance, index funds are...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Building a solid 401(k) portfolio doesn't have to be complicated. If you're looking for a straightforward way to grow your retirement savings with low fees and consistent performance, index funds are an excellent choice. These funds track market indexes, giving you diversified exposure to hundreds or thousands of companies while keeping your costs minimal. Let's explore the best index fund options available for your 401(k) in 2026.

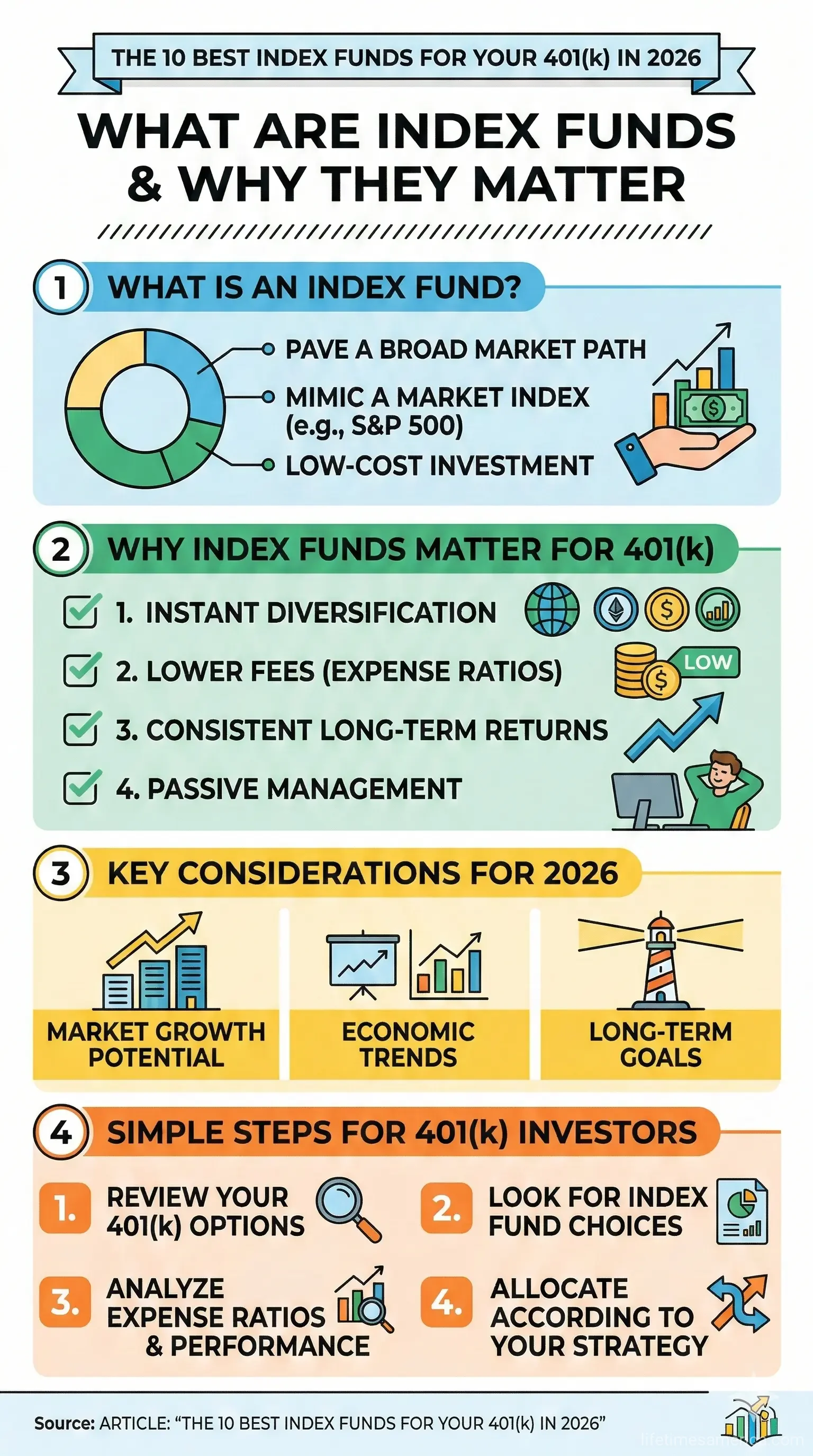

What Are Index Funds and Why They Matter for Your 401(k)

Index funds are investment funds designed to replicate the performance of a specific market index. Instead of having a fund manager actively picking individual stocks, index funds simply mirror the holdings of their target index. This passive approach means lower management fees, which translates to more of your money staying invested and growing over time.

For 401(k) investors, index funds offer several advantages. They provide instant diversification across dozens or hundreds of companies, reduce the risk of poor stock-picking decisions, and typically feature expense ratios well below 0.10%. This matters significantly over decades of retirement saving—even small fee differences compound into substantial wealth differences by retirement.

Top Index Funds for Your 401(k) Portfolio

1. Vanguard 500 Index Fund (VFIAX)

The Vanguard 500 Index Fund Admiral Shares is a foundational choice for many retirement portfolios. This fund tracks the S&P 500, giving you exposure to 500 of the largest U.S. companies that represent approximately 75% of the U.S. stock market's total value. With an expense ratio of just 0.04%, you're paying minimal fees while gaining broad market exposure.

This fund is ideal if you want a simple, core holding that captures the performance of America's largest corporations across all major sectors.

2. Vanguard Total Stock Market Index Fund (VTSAX)

If you want even broader U.S. market exposure, the Vanguard Total Stock Market Index Fund Admiral Shares covers the entire U.S. equity market, including small-cap, mid-cap, and large-cap growth and value stocks. With the same ultra-low 0.04% expense ratio, this fund provides comprehensive domestic market coverage in a single holding.

This is an excellent choice for investors who want maximum U.S. stock market diversification without needing multiple funds.

3. Vanguard Growth Index Fund (VIGAX)

For those seeking higher growth potential, the Vanguard Growth Index Fund Admiral Shares focuses on large U.S. companies in higher-growth sectors like technology, consumer services, and financial services. The expense ratio is 0.05%, still exceptionally low.

This fund suits younger investors or those with a longer time horizon who can tolerate more volatility in exchange for growth potential.

4. Vanguard Total International Stock Index Fund (VTIAX)

International diversification is crucial for a well-rounded portfolio. The Vanguard Total International Stock Index Fund Admiral Shares tracks stock indexes in both developed and emerging markets globally. With a 0.09% expense ratio, it remains very affordable while providing exposure to opportunities outside the United States.

Adding international stocks to your 401(k) reduces concentration risk and captures growth from developed economies like Canada, Germany, and Japan, as well as emerging markets.

5. Vanguard Total Bond Market Index Fund (VBTLX)

Bonds provide stability and income, especially important as you approach retirement. The Vanguard Total Bond Market Index Fund Admiral Shares offers broad exposure to the U.S. bond market with a 0.04% expense ratio.

This fund works well as a stabilizing force in your portfolio, particularly if you're in a target-date fund or building a balanced allocation.

6. Vanguard Balanced Index Fund (VBIAX)

If you prefer a hands-off approach, the Vanguard Balanced Index Fund Admiral Shares mixes stocks (approximately 60%) and bonds (about 40%) in a single fund. The 0.07% expense ratio provides professional asset allocation with minimal fees.

This option works well for investors who want a simple, pre-built allocation without managing multiple funds.

7. Vanguard Small-Cap Index Fund (VSMAX)

Small-cap stocks offer higher growth potential than large-cap stocks, though with more volatility. The Vanguard Small-Cap Index Fund Admiral Shares provides exposure to smaller U.S. companies at a 0.05% expense ratio.

Consider adding this fund if you want to capture additional growth opportunities from smaller, emerging companies.

8. iShares Core S&P 500 ETF (IVV)

Sponsored by BlackRock, one of the world's largest fund companies, the iShares Core S&P 500 ETF tracks the S&P 500 index and has maintained a strong record since its inception in 2000. This fund offers an alternative to Vanguard's S&P 500 option with comparable low costs.

Many 401(k) plans offer iShares ETFs as investment options, making this a practical choice for those with access to it through their employer plan.

9. Schwab S&P 500 Index Fund (SWPPX)

Charles Schwab's S&P 500 Index Fund is another excellent option with a strong track record dating back to 1997. With tens of billions in assets under management, this fund provides stability and reliability for 401(k) investors.

If your 401(k) plan offers Schwab funds, this is a dependable core holding with competitive fees.

10. Invesco QQQ Trust ETF (QQQ)

For investors seeking technology-heavy growth exposure, the Invesco QQQ Trust ETF tracks the Nasdaq-100 Index, focusing on the largest non-financial companies—primarily technology firms. This fund was the top-performing large-cap growth fund in terms of total return over the 15 years to December 2023, according to Lipper.

Consider this fund if you want concentrated exposure to technology and growth stocks, though it carries more volatility than broad market index funds.

Building Your Index Fund Strategy

The Three-Fund Portfolio Approach

A simple, effective strategy for 401(k) investing uses just three index funds: a U.S. stock market index fund, an international stock index fund, and a bond index fund. This approach provides diversified exposure across asset classes and geographies while keeping your portfolio manageable.

For example, a balanced allocation might look like:

- 50% Vanguard Total Stock Market Index Fund (VTSAX)

- 30% Vanguard Total International Stock Index Fund (VTIAX)

- 20% Vanguard Total Bond Market Index Fund (VBTLX)

Adjust these percentages based on your age, risk tolerance, and time horizon until retirement.

Age-Based Allocation Strategy

Your allocation should shift as you age. Younger workers can tolerate more stock exposure for growth, while those closer to retirement should increase bond allocations for stability.

- Age 25-35: 90% stocks / 10% bonds

- Age 35-50: 75% stocks / 25% bonds

- Age 50-60: 60% stocks / 40% bonds

- Age 60+: 50% stocks / 50% bonds

Expense Ratios Matter

The difference between a 0.04% expense ratio and a 0.94% expense ratio might seem small, but over 30 years of investing, those extra fees can cost you hundreds of thousands of dollars in lost growth. Always prioritize low-cost index funds in your 401(k) selections.

Common Questions About Index Funds for 401(k)s

Can I use index funds in my 401(k)?

Yes, most employer 401(k) plans offer index fund options. Check your plan's investment menu or contact your HR department to see which index funds are available. If your plan doesn't offer index funds, consider requesting them—many employers will add popular low-cost options if employees request them.

Should I use target-date funds instead of building my own index fund portfolio?

Target-date funds are convenient and automatically adjust your allocation as you approach retirement. However, if you want more control and lower fees, building your own portfolio with individual index funds is a viable alternative. Both approaches work; choose based on your preference for simplicity versus customization.

How often should I rebalance my index fund portfolio?

Most financial advisors recommend rebalancing annually or when your allocation drifts more than 5% from your target. For example, if stocks rise significantly and now represent 65% of your portfolio instead of your target 60%, you'd sell some stocks and buy bonds to rebalance.

Are index funds safe for retirement?

Index funds carry market risk—when the market declines, so does your fund value. However, they're considered safer than individual stock picking because they're diversified across many companies. The longer your time horizon, the more comfortable you can be with market volatility, as history shows markets recover over time.

What's the difference between index mutual funds and index ETFs?

Both track indexes and have low costs, but they trade differently. Mutual funds trade once daily at the market close, while ETFs trade throughout the day like stocks. For 401(k) purposes, this distinction rarely matters—choose whichever your plan offers with the lowest expense ratio.

Can I invest in both U.S. and international index funds?

Absolutely. In fact, diversifying across U.S. and international markets is recommended. A typical allocation might include 70% U.S. index funds and 30% international index funds, though you can adjust this based on your comfort level.

Getting Started With Index Funds in Your 401(k)

If you haven't already, log into your 401(k) plan's investment portal and review your current holdings. Look for the expense ratios—if you're paying more than 0.50% annually, you likely have room to optimize. Identify which index funds your plan offers and consider reallocating to a simpler, lower-cost portfolio.

Remember that investing for retirement is a marathon, not a sprint. Index funds excel at this long-term approach because they're simple, low-cost, and historically reliable. By choosing quality index funds and maintaining a disciplined approach to rebalancing, you're setting yourself up for retirement success.

Start reviewing your 401(k) options today, and don't hesitate to contact your plan administrator if you have questions about available index funds or need help understanding your investment choices.

Sources & References

-

1

9 of the Best-Performing 401(k) Funds for Your Retirement Portfolio — www.the-ifw.com

-

2

7 Popular Vanguard Index Funds for February 2026 — www.nerdwallet.com

-

3

Best 401(k) Investments: Where to Invest — www.kiplinger.com

-

4

The BEST 3 ETF Portfolio for 2026 (That I'm Using to Grow My 401k) — www.youtube.com

-

5

Best Index Funds In 2026 — www.bankrate.com

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...