How to Build an Investment Portfolio for Retirement at Any Age

Building a retirement investment portfolio doesn't require a finance degree or perfect timing—it requires a solid strategy tailored to your age, goals, and risk tolerance. Whether you're in your 30s,...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Building a retirement investment portfolio doesn't require a finance degree or perfect timing—it requires a solid strategy tailored to your age, goals, and risk tolerance. Whether you're in your 30s, 50s, or already retired, the right approach can help you grow wealth, manage risk, and create a sustainable income stream for your retirement years.

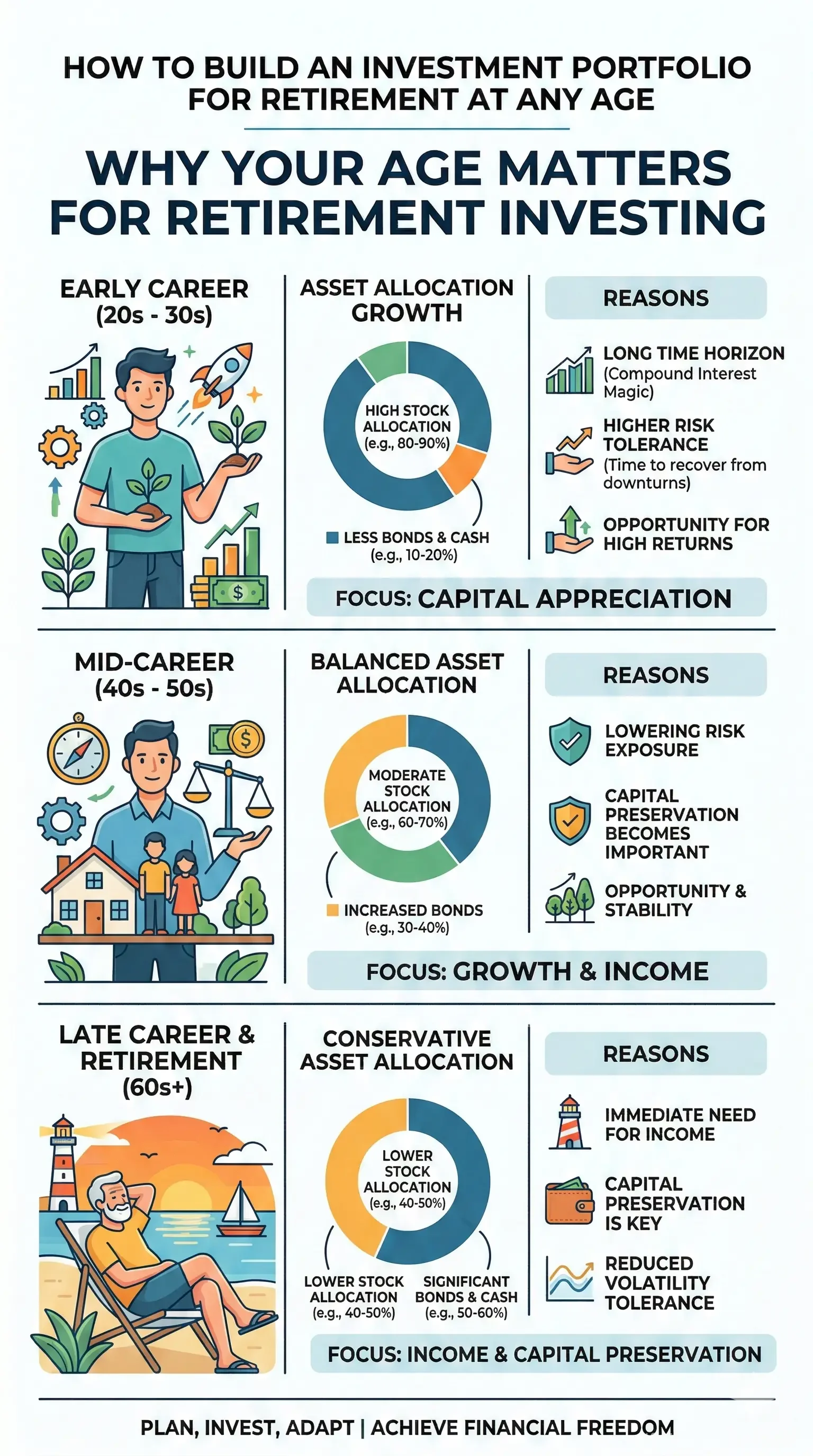

Why Your Age Matters for Retirement Investing

Your age is one of the most important factors in determining your investment strategy. The further you are from retirement, the more time you have to recover from market downturns and benefit from long-term growth. Conversely, retirees face sequence-of-returns risk—the danger that poor market performance early in retirement can significantly impact your ability to withdraw funds sustainably.

This fundamental difference means your portfolio should evolve as you age. A 35-year-old and a 65-year-old need completely different approaches, even though both are saving for retirement.

The Three-Bucket Retirement Portfolio Framework

One of the most effective ways to organize your retirement investments is using a three-bucket approach:

- Income Bucket: Bonds, cash, and income-producing assets that provide stable, predictable returns

- Growth Bucket: Stocks (both U.S. and international) that offer long-term appreciation potential

- Hedge/Alternative Bucket: Real assets, commodities, or alternatives that protect against inflation and market volatility

This structure balances stability, growth, and inflation protection—three critical needs for retirement savers at any life stage.

Asset Allocation by Age: A Practical Roadmap

Ages 30-40: Focus on Growth

With several decades until retirement, you should focus on stocks as your primary investment. You have enough time to benefit from long-term growth potential while riding out short-term market volatility. During this phase, many people are in peak earning years and can redirect resources toward retirement savings.

A growth-focused allocation might look like:

- 80-90% stocks

- 10-20% bonds and fixed income

- Small allocation to alternatives (optional)

Ages 40-50: Maintain Growth, Add Stability

With more than a decade or two of working years left, it's important to maintain growth potential through appropriate stock allocation. However, you might begin adding a meaningful allocation to bonds to reduce volatility as retirement approaches.

A balanced approach might include:

- 65-75% stocks

- 25-35% bonds and fixed income

Ages 50+: Transition to Conservative

As you near retirement, your portfolio should gradually shift from aggressive to conservative. This doesn't mean abandoning stocks entirely—retirement can last three decades or more, meaning your portfolio still needs growth. However, you'll want more exposure to bonds and cash to reduce the impact of short-term market swings.

A conservative-growth allocation might include:

- 50-60% stocks

- 40-50% bonds and fixed income

In Retirement: Protect Principal While Growing

Exposure to stocks should remain an important part of your allocation target, even in retirement. However, since you may need to access these assets for income in the near term, you're more susceptible to short-term risks. Position your portfolio with more exposure to bonds and cash while maintaining some growth potential.

A typical retiree allocation might be:

- 40-50% stocks

- 50-60% bonds, cash, and fixed income

Diversification: Your Risk Management Tool

Many retirees build portfolios heavily concentrated in U.S. large-cap stocks, especially technology companies. While this strategy worked well over the past 15 years, it's not guaranteed to continue. Diversification is not about maximizing returns—it's about managing uncertainty.

A properly diversified portfolio should include:

- Multiple sectors (technology, healthcare, financials, consumer goods, etc.)

- Domestic and international stocks

- Bonds and fixed income

- Alternative assets where appropriate

Within your stock allocation, consider this model:

- 60% U.S. large-cap stocks

- 25% developed international stocks

- 10% U.S. small-cap stocks

- 5% emerging market stocks

This approach reduces the impact of any single market event and improves portfolio resilience.

Simplifying Your Portfolio: Three Smart Strategies

Managing a complex portfolio with dozens of individual funds can be overwhelming. Here are three ways to simplify:

Strategy 1: Use Index Funds Instead of Actively Managed Funds

Index funds are passive investments that track market indices like the S&P 500. They have lower fees, require less monitoring, and historically match or beat actively managed funds for most investors. Index funds are a great low-cost way to achieve diversification easily.

Strategy 2: Choose Broad All-Market Stock Funds

Instead of managing multiple style-specific equity products (growth stocks, value stocks, small-cap, large-cap), favor broad all-market stock funds that give you exposure to all of these at once. This simplifies your portfolio while maintaining proper diversification.

Strategy 3: Use Target-Date or Allocation Funds

Target-date funds are an excellent option if you don't want to manage a portfolio yourself. These funds automatically shift your investments from more aggressive stocks to more conservative bonds as your target retirement date nears, so your portfolio becomes safer when you need it most.

Allocation funds combine stocks and bonds in one portfolio, providing asset-class diversity in a single fund. Conservative allocation funds hold 15-30% in equities and the rest in bonds, while aggressive funds hold more stocks than bonds.

Robo-Advisors: Automated Investing for Hands-Off Investors

If you prefer a completely hands-off approach, robo-advisors can manage your entire portfolio automatically. You simply deposit money into the account, answer questionnaires about your goals and risk tolerance, and the robo-advisor handles the rest. Most robo-advisors select low-cost ETFs and build a diversified portfolio tailored to your needs.

Rebalancing: Keep Your Portfolio on Track

Market performance can throw your asset allocation out of balance over time. If you decided years ago to keep 55% in equities and 45% in fixed income, but a booming stock market has pushed your allocation to 65/35, it's time to rebalance.

Rebalancing means selling some of your winning investments and buying more of your underperforming ones. This disciplined approach helps you avoid buying high and selling low—a common investor mistake.

Plan for Inflation and Long-Term Care

Two often-overlooked retirement risks are inflation and long-term care costs. Make sure your portfolio includes inflation-fighting investments like stocks and real assets. Additionally, consider long-term care insurance or hybrid annuities that provide both growth and long-term care protection. As 2026 progresses, protecting your portfolio from high long-term care costs is just as important as managing market risk.

Practical Steps to Start Building Your Portfolio Today

- Determine your target retirement date and calculate how many years you have to save

- Choose your asset allocation based on your age and risk tolerance

- Select your investment vehicles (index funds, target-date funds, or a robo-advisor)

- Open a retirement account if you haven't already (401(k), IRA, or Roth IRA)

- Set up automatic contributions so you invest consistently regardless of market conditions

- Review and rebalance annually to keep your portfolio aligned with your goals

Your Retirement Investment Journey Starts Now

Building a retirement investment portfolio at any age comes down to three core principles: understanding your time horizon, maintaining proper diversification, and sticking to a disciplined plan. Whether you're just starting out in your 30s or fine-tuning your strategy in your 50s, the key is to begin now and adjust as you progress through life.

Start by assessing your current situation, determining your target retirement date, and choosing an asset allocation that matches your age and risk tolerance. Use low-cost index funds or target-date funds to keep things simple, set up automatic contributions, and commit to annual rebalancing. With this approach, you'll build a retirement portfolio that works for you—not against you.

Ready to take action? Open a retirement account today, make your first contribution, and set a calendar reminder to review your portfolio annually. Your future self will thank you.

Frequently Asked Questions

Sources & References

-

1

Retirement Investing 2026: Strategic Portfolio Tips — earlyretirementadvice.com

-

2

10 Best Long-Term Investments In 2026 — www.bankrate.com

-

3

3 Ways to Simplify Your Investment Portfolio in 2026 — www.morningstar.com

-

4

6 Key Ways to Plan for Financial Success in 2026 — www.kiplinger.com

-

5

Retirement savings by age: What to do with your portfolio in 2026 — www.troweprice.com

-

6

7 Smart Money Moves for 2026 Retirement Planning — www.fidelity.com

Useful Tools

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...