Checking vs Savings Account: What Is the Difference?

Ever wondered why your paycheck hits one account but your emergency fund sits in another? You're not alone—millions of Americans juggle checking vs savings accounts daily to balance spending and savin...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever wondered why your paycheck hits one account but your emergency fund sits in another? You're not alone—millions of Americans juggle checking vs savings accounts daily to balance spending and saving. Understanding their differences can help you avoid fees, earn more interest, and build real financial security in 2026.

Both accounts are FDIC-insured up to $250,000 per depositor, per bank, giving you peace of mind no matter where you park your cash. But that's where the similarities end. Let's break down the key distinctions, so you can choose wisely and optimize your banking setup.

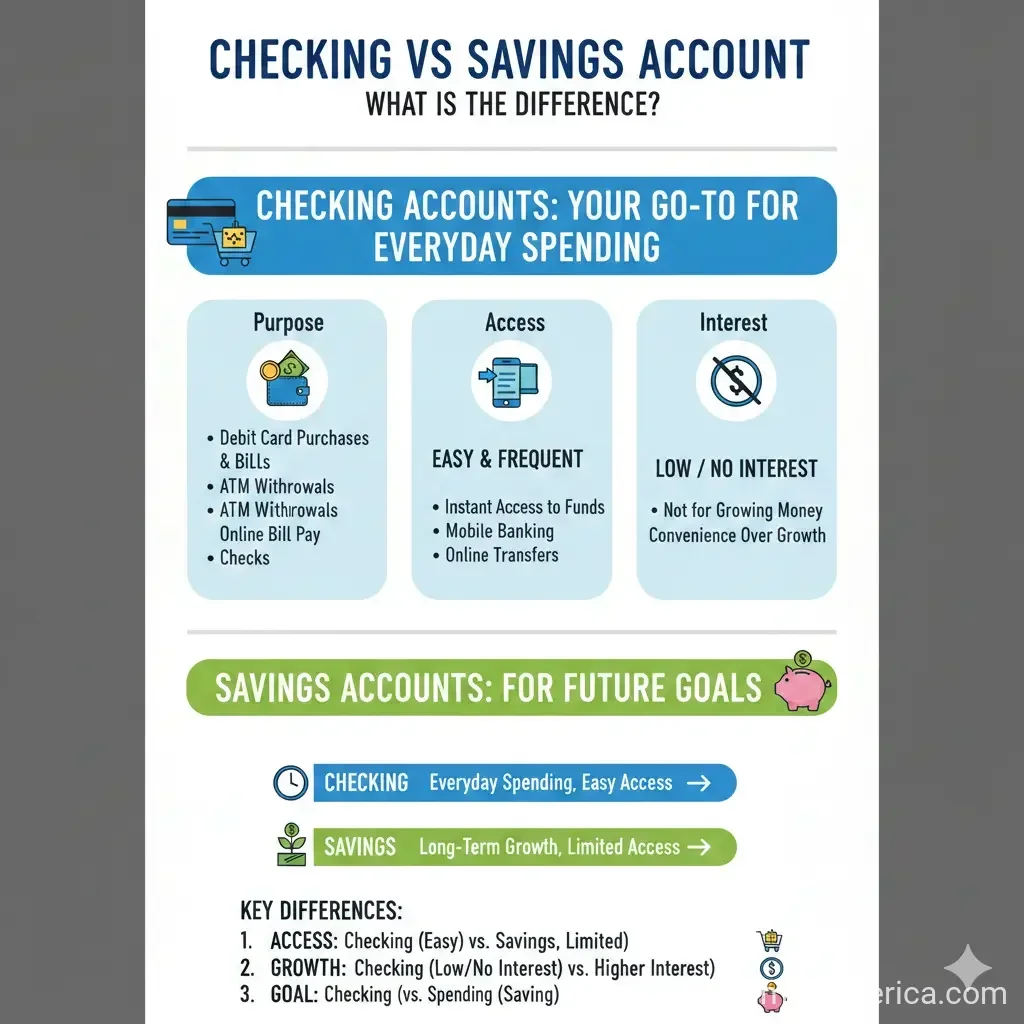

Checking Accounts: Your Go-To for Everyday Spending

A checking account is like your financial command center—designed for frequent transactions without limits. Use it for direct deposits from your employer, paying rent via apps like Zelle, swiping your debit card at the grocery store, or writing checks (though fewer folks do that now).

In 2026, with inflation still a factor, checking accounts shine for liquidity. Banks like Bank of America and Huntington offer features such as:

- Unlimited withdrawals, transfers, and payments—no caps to cramp your style.

- Online bill pay, mobile check deposits, and ATM access nationwide.

- Overdraft protection options to cover unexpected shortfalls (watch for fees, though).

- Cash-back rewards or early direct deposit perks at select banks.

Do Checking Accounts Earn Interest?

Most don't, but interest-bearing versions exist. These pay a low APY—often under 0.5% in 2026—tiered by balance. They're great if you keep higher averages, but high minimums and fees can eat gains. Compare this to savings for better growth.

Common Checking Account Fees to Watch

Fees can sneak up, but many banks waive them with direct deposit or minimum balances:

- Monthly maintenance: $5–$25, often avoidable.

- Overdraft: Up to $35 per transaction.

- Out-of-network ATM: $2–$5 plus bank surcharges.

Pro tip: Shop no-fee options from credit unions or online banks via the FDIC's BankFind tool at fdic.gov.

Savings Accounts: Build Wealth While You Sleep

Savings accounts are your growth engine, earning interest on every dollar you stash away. Perfect for emergency funds (aim for 3–6 months' expenses), vacation savings, or down payments. Limited access discourages impulse buys, helping you stick to goals.

High-yield savings accounts (HYSAs) from online banks lead in 2026, offering APYs around 4–5%—far outpacing traditional ones at 0.01–0.5%. Your money compounds automatically, turning $10,000 into over $10,400 in a year at 4% (assuming daily compounding).

Savings Account Rules and Limits

Federal Regulation D was relaxed post-2020, but many banks still enforce:

- Up to 6 "convenient" withdrawals per statement cycle (transfers count; in-person/ATM often unlimited).

- Excess fees: $5–$25 per extra withdrawal.

- Minimum balance requirements to waive monthly fees.

This structure promotes saving—set it and forget it.

Types of Savings Accounts

- Standard Savings: Basic interest, easy access.

- High-Yield Savings: Top rates from Ally or Capital One.

- Money Market Accounts: Check-writing perks with higher rates (still savings-like limits).

Checking vs Savings Account: Side-by-Side Comparison

Here's a quick table to see the checking vs savings account differences at a glance:

| Feature | Checking Account | Savings Account |

|---|---|---|

| Purpose | Daily spending, bills, debit | Saving for goals, emergencies |

| Access | Unlimited transactions | Limited withdrawals (often 6/month) |

| Interest | Rare/low (under 0.5% APY) | Yes, up to 5% APY in HYSAs |

| Fees | Overdraft, monthly, ATM | Minimum balance, excess withdrawal |

| Tools | Debit card, checks, bill pay | Auto-transfers, goal trackers |

| FDIC Insurance | Up to $250,000 | Up to $250,000 |

Data synthesized from major banks.

Pros and Cons: Which Wins for You?

Checking Account Pros

- Flexibility for life's curveballs.

- Digital tools like Zelle integration.

- No transaction guilt.

Cons: Minimal growth; fee traps if unmanaged.

Savings Account Pros

- Money grows passively—beat inflation.

- Psychological separation from spending.

- HYSAs crush traditional checking rates.

Cons: Withdrawal hassles; lower liquidity.

Real-Life Strategies: Use Both Like a Pro

The best setup? Both accounts. Direct deposit your paycheck to checking, pay bills, then auto-transfer 20% to savings (the 50/30/20 rule: 50% needs, 30% wants, 20% savings). Apps like Ally or Bank of America make this seamless.

Actionable Tips for 2026:

- Automate Transfers: Post-payday, move funds before you spend.

- Ladder Accounts: One checking, multiple savings buckets (emergency, car fund, etc.).

- Hunt Rates: Use Bankrate.com or NerdWallet for top APYs—switch if under 4%.

- Bundle for Perks: Many banks waive fees with linked accounts.

- Track with Apps: Mint or YNAB to monitor balances.

- IRS Tip: Savings interest over $10 is taxable—report on Form 1099-INT.[irs.gov]

For gig workers or freelancers, pair with a high-yield checking for unlimited access plus some interest.

Next Steps to Master Your Money

Review your accounts today: Log into online banking, compare APYs, and set up auto-savings. Visit fdic.gov for insured banks or consumerfinance.gov for fee smarts. Open a HYSA if you don't have one—your future self will thank you. With smart checking vs savings account use, you'll spend wisely, save effortlessly, and thrive financially.

Frequently Asked Questions

Sources & References

-

1

Bank of America: The Difference Between Checking and Savings Accounts — bettermoneyhabits.bankofamerica.com

-

2

SouthStar Bank: Checking vs Savings Accounts: What's the Difference? — southstarbank.com

-

3

Bankrate: Checking Vs. Savings Accounts: Differences And How To... — www.bankrate.com

- 4

-

5

Huntington Bank: Difference Between Checking and Savings Accounts — www.huntington.com

-

6

Experian: Checking Account vs. Savings Account — www.experian.com

-

7

NerdWallet: Checking vs. Savings Accounts: The Difference — www.nerdwallet.com

-

8

IRS: Interest Income — www.irs.gov

Useful Tools

Related Articles

How to Handle "Identity Theft" in 2026: The First 24 Hours

Imagine checking your bank account on a quiet Saturday evening, only to discover unauthorized charges totaling thousands of dollars—or worse, spotting a new credit card opened in your name. In 2026, i...

The Best "Digital Banking" Apps for US Teens: A Parent's Guide

Imagine handing your teen a debit card that teaches them financial responsibility without the risk of overdrafts or debt. In 2026, digital banking apps make this possible, giving US parents powerful t...

The Best Online Banks with No Monthly Fees in 2026

Imagine ditching those pesky monthly bank fees that quietly eat into your budget every single month. In 2026, online banks make it easier than ever for Americans to enjoy truly free checking accounts...

How to Start an Emergency Fund from Scratch: $1 to $1;000

Picture this: Your car breaks down on the way to work, or an unexpected medical bill lands in your mailbox. Without a safety net, you're scrambling for credit cards or loans with sky-high interest rat...