What Is Compound Interest and How Does It Grow Your Savings?

Imagine turning $1,000 into over $7,000 in just 30 years without adding another dime. That's the magic of compound interest at work, quietly multiplying your savings while you sleep. For Americans bui...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine turning $1,000 into over $7,000 in just 30 years without adding another dime. That's the magic of compound interest at work, quietly multiplying your savings while you sleep. For Americans building wealth through 401(k)s, IRAs, or high-yield savings accounts, understanding this powerhouse is key to financial freedom.

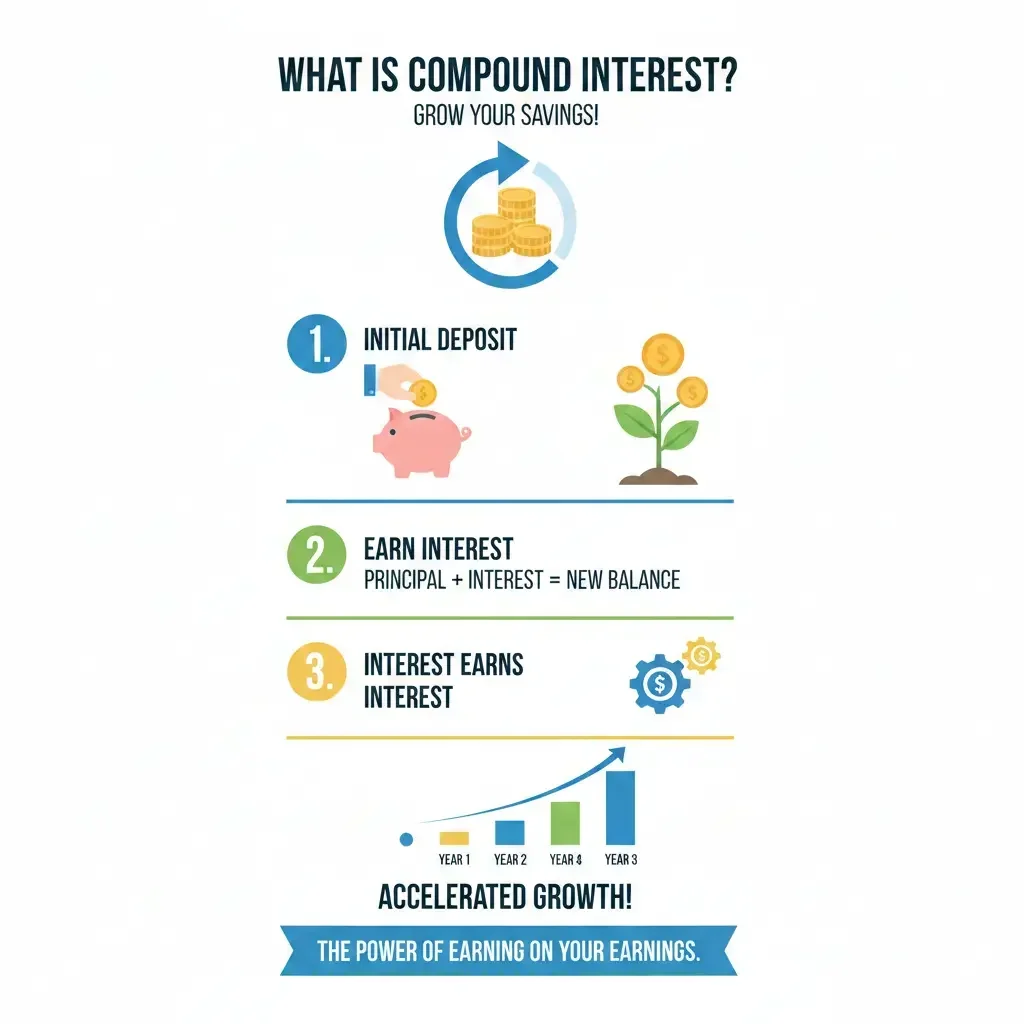

What Is Compound Interest?

Compound interest is the interest you earn on both your initial deposit—called the principal—and the interest that has already accumulated. Unlike simple interest, which only pays on the principal, compounding creates a snowball effect, where your money generates more money over time.

This process is essential for long-term savings in the U.S., powering growth in retirement accounts and college savings plans like 529s. The IRS recognizes compound growth in tax-advantaged accounts, allowing your earnings to compound tax-free or tax-deferred until withdrawal.

Compound Interest vs. Simple Interest

Simple interest calculates only on the principal. For example, $1,000 at 5% simple interest for 10 years yields $500 in interest ($1,000 × 0.05 × 10).

With compound interest at the same rate, compounded annually, you'd end up with $1,628.89—over $128 more—because interest earns on growing balances.

The Compound Interest Formula Explained

The standard formula for compound interest is A = P(1 + r/n)nt, where:

- A is the amount of money accumulated after time t, including interest.

- P is the principal amount.

- r is the annual nominal interest rate (as a decimal).

- n is the number of times interest is compounded per year.

- t is the time the money is invested for in years.

For continuous compounding, the formula becomes A = Pert, representing the theoretical maximum growth.

A Real-World U.S. Example

Say you deposit $5,000 in a high-yield savings account at 4.5% APY in 2026, compounded monthly (n=12). After one year: A = 5000(1 + 0.045/12)(12×1) ≈ $5,231.06. That's $231.06 earned, accelerating yearly.

How Does Compound Interest Grow Your Savings?

Compounding frequency matters: daily beats monthly, which outperforms annually. More frequent compounding means faster growth, but always compare APY—it factors in compounding.

| Compounding Frequency | Final Amount After 10 Years ($10,000 @ 5% APY) |

|---|---|

| Annually | $16,288.95 |

| Monthly | $16,453.96 |

| Daily | $16,470.99 |

Calculations based on the formula; daily compounding adds about $182 extra over annual.

The Power of Time and Consistency

Time is your biggest ally. Starting early leverages decades of compounding. A 25-year-old investing $200 monthly at 7% (historical stock market average) could amass $614,000 by 65. Delay to 35, and it's only $226,000.

Regular contributions supercharge growth. Use tools like the Investor.gov compound interest calculator to model your scenario.

Compound Interest in U.S. Savings and Investments

In 2026, FDIC-insured high-yield savings accounts offer up to 4.5-5% APY, compounding daily or monthly, ideal for emergency funds.

Retirement Accounts: 401(k)s and IRAs

Employer 401(k) matches are free compounding fuel—many vest over time. Roth IRAs grow tax-free; contribute post-tax dollars for qualified withdrawals without IRS taxes.

Target-date funds in 401(k)s automatically adjust for compounding across decades, balancing stocks and bonds.

Other Vehicles

- HSAs: Triple tax-advantaged; compound pre-tax for medical expenses.

- 529 Plans: State-sponsored for education, with tax-free growth.

- CDs: Fixed rates, FDIC-backed, compounding quarterly or monthly.

Practical Tips to Maximize Compound Interest

Harness compounding with these actionable steps tailored for Americans:

- Start Now: Even $50/month in a Roth IRA compounds massively over 40 years.

- Automate Contributions: Set payroll deductions to 401(k)s or bank auto-transfers.

- Seek High APYs: Shop FDIC-insured online banks via DepositAccounts.com.

- Reinvest Dividends: In brokerage accounts, let stock dividends compound.

- Avoid Withdrawals: Penalties erode compounding; build ladders for liquidity.

- Use Calculators: Investor.gov or Bankrate tools for projections.

Watch fees: Index funds with low expense ratios (under 0.1%) preserve more for compounding.

Common Pitfalls to Avoid

Debt compounds against you—credit card APRs average 20%+ in 2026, outpacing savings. Pay off high-interest debt first.

Inflation erodes purchasing power; aim for returns above 2-3% annually. Taxes hit non-retirement accounts—use tax-advantaged options.

Start Growing Your Savings Today

Compound interest isn't just math—it's your path to financial independence. Open a high-yield savings account, max your 401(k) match, or explore a Roth IRA via Fidelity or Vanguard. Use a calculator to project your future, then act. Small steps today yield massive rewards tomorrow.

Frequently Asked Questions

Sources & References

-

1

Compound Interest Calculator — financialmentor.com — www.financialmentor.com

-

2

Compound Interest Calculator — nerdwallet.com — www.nerdwallet.com

-

3

Compound Interest Calculator — calculatorsoup.com — www.calculatorsoup.com

-

4

Compound Savings Calculator — bankrate.com — www.bankrate.com

-

5

What Is Compound Interest? — ccu.com — www.ccu.com

-

6

Compound Interest Calculator — calculator.net — www.calculator.net

-

7

Compound Interest Calculator — investor.gov — www.investor.gov

Useful Tools

Related Articles

The Best "No-Fee" Brokerages for Fractional Shares in 2026

Imagine owning a slice of Amazon or Tesla without needing thousands of dollars upfront. That's the power of fractional shares, letting everyday Americans build diversified portfolios on any budget in...

The Best "Micro-Investing" Apps for Spare Change in 2026

Imagine turning your daily coffee run's spare change into a growing investment portfolio without lifting a finger. In 2026, micro-investing apps make it easier than ever for Americans to build wealth...

How to Hedge Against 2.8% Inflation: The Best Assets for 2026

Inflation at 2.8% might not grab headlines like the 9% peaks of a few years back, but it's still quietly eroding your purchasing power—think higher grocery bills, pricier gas, and rent that just keeps...

How to Use "Series I Bonds" as a 2026 Inflation Hedge

If you're worried about inflation eating away at your savings, Series I bonds offer a straightforward way to protect your purchasing power while earning a competitive return backed by the U.S. governm...