How Much Do You Need to Retire Comfortably in the USA?

Imagine waking up every morning in retirement without checking your bank balance first. That's the dream for millions of Americans, but turning it into reality starts with knowing how much you need to...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine waking up every morning in retirement without checking your bank balance first. That's the dream for millions of Americans, but turning it into reality starts with knowing how much you need to retire comfortably in the USA. With living costs rising and Social Security facing uncertainties, planning ahead is crucial—especially with 2026 bringing fresh contribution limits to boost your savings.

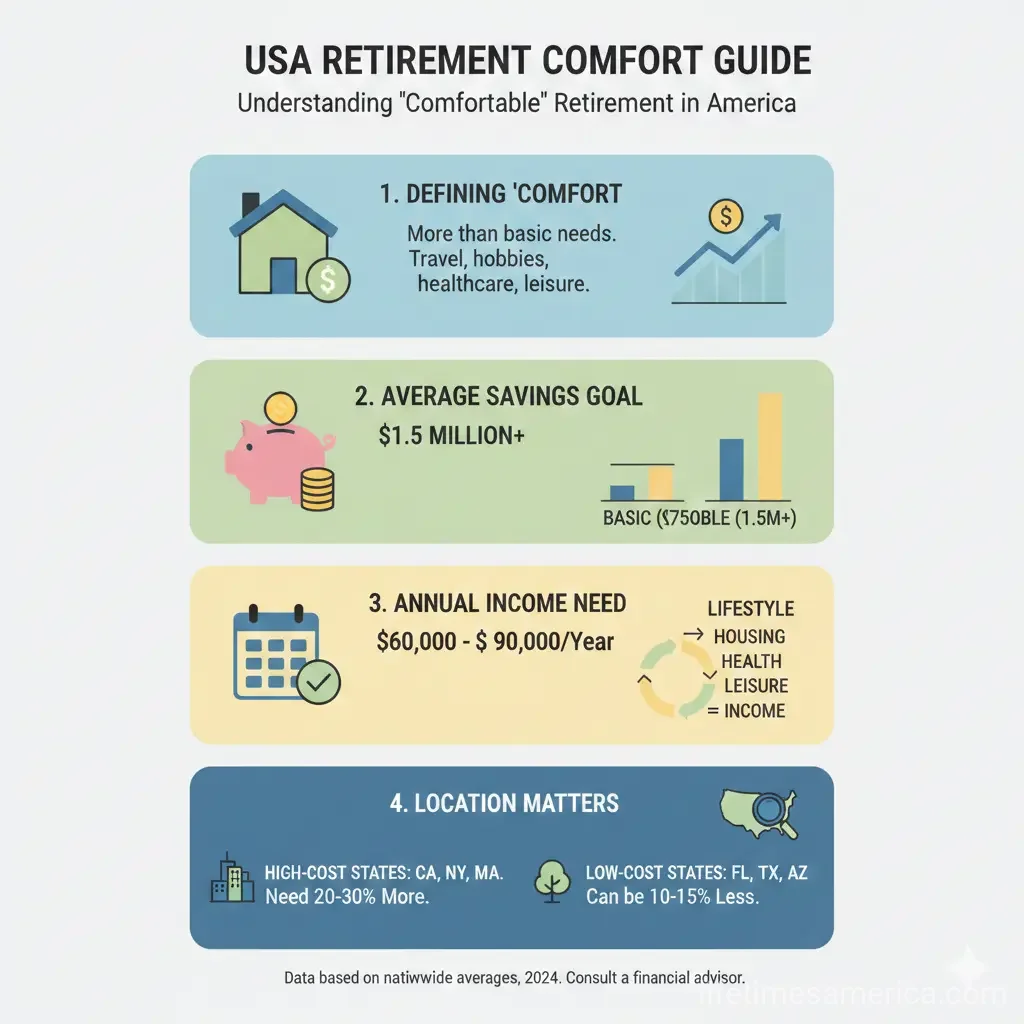

Understanding "Comfortable" Retirement in America

Comfortable retirement means covering essentials like housing and healthcare while enjoying travel, hobbies, or family time. It varies by lifestyle, location, and health, but experts often peg it at 70-80% of your pre-retirement income. For a household earning $80,000 annually, that could mean $56,000-$64,000 yearly in retirement spending.

In high-cost states like California or New York, you might need double that in urban areas, while Midwest or Southern spots offer relief. Factor in inflation—projected at 2-3% annually—and longevity, as many Americans now live into their 90s.

Key Factors Influencing Your Number

- Location: Housing eats 30-40% of budgets; coastal cities demand more savings.

- Healthcare: Medicare starts at 65, but gaps like long-term care can cost $100,000+ yearly.

- Lifestyle: Frequent travel? Add $10,000-$20,000 annually.

- Inflation and Longevity: Plan for 25-30 years post-retirement.

The Famous 25x Rule: A Starting Point

The "4% rule" suggests withdrawing 4% of your nest egg yearly, adjusted for inflation, with low depletion risk over 30 years. Flip it: Multiply annual expenses by 25 for your target savings. Need $60,000 yearly? Aim for $1.5 million.

This rule, from the Trinity Study, assumes a balanced stock-bond portfolio. Conservative savers might use 25-33x for safety, especially with market volatility.

Regional Retirement Costs in 2026

Average U.S. retiree needs $1.46 million for 20 years of comfortable living, per recent analyses. Breakdown:

| Category | Annual Cost | 20-Year Total |

|---|---|---|

| Housing | $18,000 | $360,000 |

| Food | $7,200 | $144,000 |

| Healthcare | $12,000 | $240,000 |

| Transportation | $6,000 | $120,000 |

| Entertainment | $4,800 | $96,000 |

| Total | $48,000 | $960,000 |

Adjust upward for coastal living or luxury; downward for frugal habits. Tools like the IRS withholding estimator or SSA's Quick Calculator help personalize.

Social Security: Your Baseline, Not Your Whole Plan

Average monthly benefit in 2026 hits about $1,900, or $22,800 yearly, but max benefits near $4,000/month require 35 years of high earnings. Don't rely solely on it—it's designed as a supplement, covering just 40% of average earners' needs.

Claim at 62 for reduced payments, full retirement age (67 for most) for standard, or delay to 70 for 8% annual boosts. With trust fund concerns, work credits matter—aim for 40.

Medicare and Healthcare Realities

Medicare Parts A/B cover basics at 65, but premiums, deductibles, and Medigap policies add $5,000-$10,000 yearly. Long-term care insurance? Essential if not self-funding.

2026 Retirement Savings Limits: Maximize Now

Good news for 2026: IRS hiked limits to supercharge savings. 401(k), 403(b), and 457 plans allow $24,500 for under-50s. Age 50+? Add $8,000 catch-up for $32,500 total. Ages 60-63 get "super catch-up" of $11,250, totaling $35,750.

IRAs cap at $7,500 ($8,600 with catch-up for 50+). High earners ($150,000+ in 2025) must do catch-ups as Roth. Total defined contribution limit: $72,000 ($80,000 for 50+).

Actionable Savings Strategies

- Max Employer Matches: Free money—most plans match 50% up to 6%.

- HSAs for Healthcare: $4,400 single/$8,750 family in 2026; triple tax-free.

- Roth Conversions: Shift traditional to Roth pre-RMDs (age 73, or 75 if born 1960+).

- Automate Increases: Bump contributions 1% yearly.

A 50-year-old maxing 401(k) ($32,500) plus IRA ($8,600) could save $41,100 tax-advantaged—huge for compound growth.

Building Your Personalized Retirement Number

Step 1: Track expenses for 3 months. Step 2: Project to retirement, inflating 2.5%. Step 3: Subtract guaranteed income (Social Security, pensions). Step 4: Multiply gap by 25.

Example: $70,000 expenses - $25,000 Social Security = $45,000 gap x 25 = $1.125 million needed.

Investment Growth Assumptions

Assume 5-7% annual returns post-fees/inflation. Diversify: 60% stocks, 40% bonds. Rebalance yearly.

- Use Vanguard or Fidelity calculators for simulations.

- Stress-test for downturns (e.g., 2008 crash).

Common Pitfalls and How to Avoid Them

Overspending early, underestimating healthcare, or ignoring taxes derail plans. RMDs at 73 force withdrawals, taxing Roth conversions strategically helps. Review annually; adjust for life changes like divorce or inheritance.

Take Control of Your Retirement Today

Run your numbers using SSA.gov or IRS tools, max 2026 contributions, and consult a fiduciary advisor. Small steps now—like upping savings 1%—compound massively. You're not just saving; you're buying freedom. Start with one action this week.

Frequently Asked Questions

Sources & References

-

1

What are 2026 401(k) and IRA max contribution limits? | Principal — www.principal.com

- 2

-

3

How to Make 2026 Your Best Year Yet for Retirement Savings — www.kiplinger.com

- 4

-

5

2026 Retirement Plan Contribution Limits (401k, 457(b) & More) — www.missionsq.org

-

6

6 Retirement Must-Knows for 2026 - YouTube — www.youtube.com

- 7

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...