Hard Money Loans Explained: When Real Estate Investors Use Them

If you're a real estate investor looking to close a deal quickly without jumping through traditional bank hoops, hard money loans might be your answer. These specialized financing tools have become es...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're a real estate investor looking to close a deal quickly without jumping through traditional bank hoops, hard money loans might be your answer. These specialized financing tools have become essential for property flippers, developers, and investors who need capital fast and don't fit the conventional lending mold. Let's explore how hard money loans work, who uses them, and whether they're the right fit for your investment strategy.

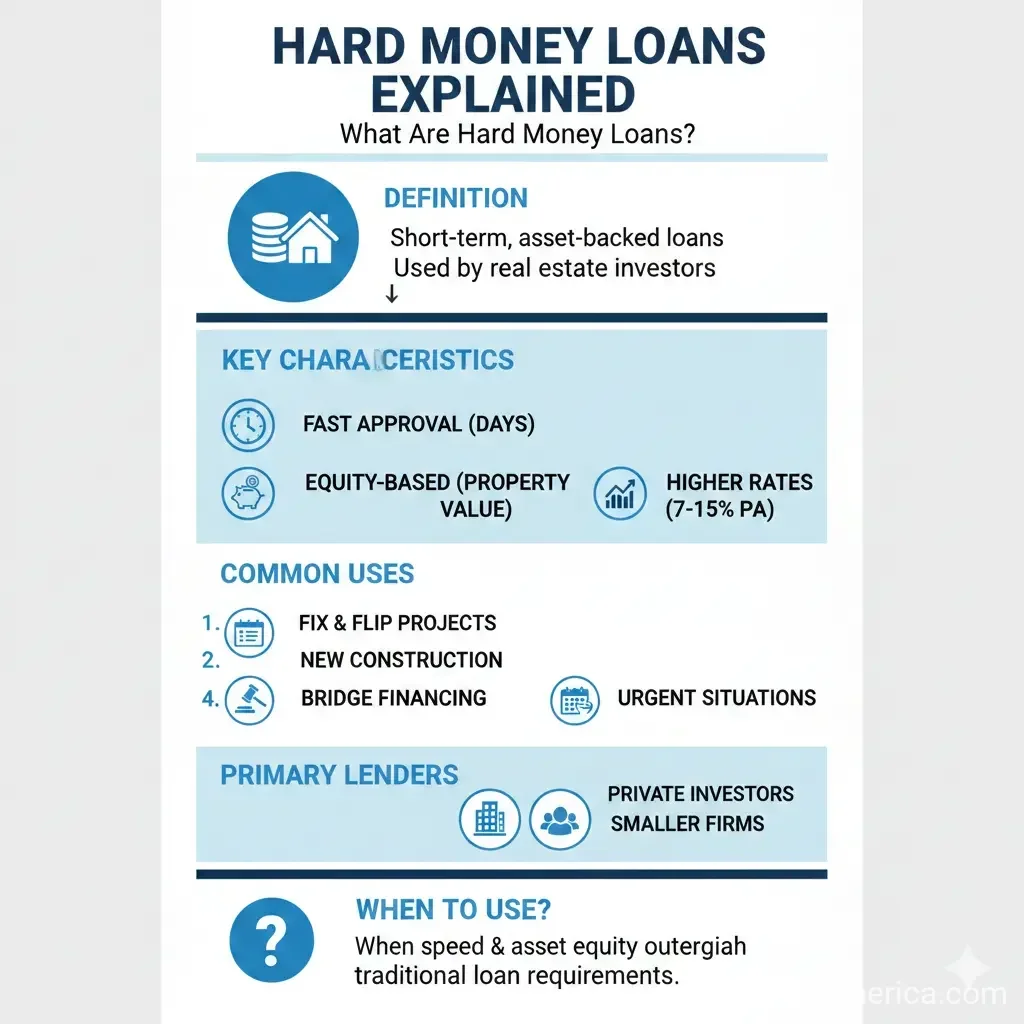

What Are Hard Money Loans?

Hard money loans are short-term, asset-based financing secured by real estate property rather than your credit score or income. Unlike traditional bank mortgages that scrutinize your credit history, debt-to-income ratio, and employment verification, hard money lenders focus primarily on the value of the property itself. This fundamental difference makes hard money loans accessible to borrowers who might not qualify for conventional financing, including those with lower credit scores or unconventional income sources.

Hard money loans are typically provided by private individuals or private lending companies, not traditional banks. Because these lenders operate outside the strict regulatory framework that governs conventional mortgages, they can approve loans and fund them much faster—often within days rather than weeks.

How Hard Money Loans Work

The Basic Structure

Hard money loans function differently from traditional mortgages in several key ways. Here's what you need to know about the typical loan structure:

- Loan-to-Value (LTV) Ratio: Most hard money lenders will finance 60% to 75% of the property's value, though some may go up to 80% or 90% depending on the project type. For example, a $200,000 property might qualify you for $120,000 to $150,000 in financing.

- Down Payment Requirements: You'll typically need to put down 20% to 30% of the purchase price. This larger down payment compared to traditional mortgages reflects the lender's focus on protecting their collateral.

- Interest Rates: Hard money loans carry higher interest rates than conventional mortgages, typically ranging from 8% to 15%. The exact rate depends on factors like the property condition, your experience level, and the lender's assessment of risk.

- Loan Terms: These loans are short-term by design, usually lasting 6 to 24 months. This short timeline aligns with typical real estate investment projects like flips or renovations.

- Upfront Fees: Expect to pay 2% to 4% of the loan amount upfront. These fees cover the lender's origination costs and underwriting.

Payment Structure

Hard money loans typically feature interest-only payments during the loan term, with the remaining principal balance due in full at the end—often called a balloon payment. This structure allows you to minimize monthly cash outflow while the property is being renovated or held, with the expectation that you'll repay the entire balance when you sell the property or refinance into a traditional loan.

The Approval Process

The hard money loan approval process moves quickly and follows a different path than traditional lending:

- Property Identification: You select an investment property and present it to the lender.

- Initial Screening: The loan officer confirms the deal fits their lending criteria based on property type, location, and your investment strategy.

- Underwriting and Valuation: The lender completes formal underwriting and assesses the property's after-repair value (ARV)—what the property will be worth after improvements.

- Term Structuring: Loan terms, pricing, and timelines are finalized.

- Closing and Funding: The loan closes and funds quickly, often within 7 to 14 days.

When Real Estate Investors Use Hard Money Loans

Common Use Cases

Hard money loans serve several specific investment scenarios where speed and flexibility matter more than traditional lending terms:

- House Flipping: Investors use hard money to quickly purchase distressed properties, fund renovations, and flip them for profit. The short loan term aligns perfectly with the typical 6-12 month flip timeline.

- Fix-and-Flip Projects: Similar to house flipping, these loans finance the purchase and renovation of properties that need significant work.

- Rental Property Refinishing: Investors renovate rental units to increase their value and rental income potential.

- Bridge Financing: If you need to purchase a new property before selling your current one, hard money provides quick capital to bridge the gap. You repay the loan once you sell your existing property.

- New Construction: Developers use hard money to fund new construction projects where traditional lenders might be hesitant.

- Land Acquisition and Development: Hard money loans help builders and developers quickly secure land before competitors, enabling them to capitalize on time-sensitive market opportunities.

- Off-Market and Distressed Properties: When you find a great deal off-market or from a distressed seller, hard money allows you to move quickly before the property hits the open market.

- Unconventional Properties: Properties that don't meet traditional lending standards due to condition, zoning issues, or incomplete income history may still qualify for hard money loans.

Who Benefits Most from Hard Money Loans?

Hard money loans work best for specific borrower profiles:

- Real estate investors with time-sensitive projects

- Borrowers with credit challenges or lower credit scores

- Experienced investors who understand short-term debt strategy

- Investors in competitive markets where speed provides a competitive advantage

- New investors without extensive traditional lending history

- Borrowers seeking properties that don't qualify for traditional loans

Advantages of Hard Money Loans

Hard money loans offer distinct advantages in specific situations:

- Speed: Approval and funding happen in days, not weeks, allowing you to close deals quickly and beat competitors.

- Flexible Underwriting: Lenders focus on the property's potential rather than your credit score or income, making them accessible to borrowers traditional banks reject.

- Accessibility for Poor Credit: If you have credit challenges, hard money provides a viable financing path.

- Capital Efficiency: For experienced investors, short-term hard money debt preserves liquidity for multiple projects, unexpected rehab costs, or parallel deals.

- Competitive Advantage: In hot markets, hard money enables quicker closings, helping you compete against cash buyers without tying up all your capital.

- Flexible Terms: Lenders adjust terms based on your project needs, including interest-only payments and balloon payment structures.

Disadvantages and Risks

Before pursuing hard money financing, understand the significant drawbacks:

- Higher Interest Rates: Rates of 8% to 15% are substantially higher than traditional mortgages, increasing your borrowing costs.

- Short Repayment Terms: The 6-24 month timeline creates pressure to execute your exit strategy quickly.

- Large Down Payments: The 20% to 30% down payment requirement ties up significant capital upfront.

- Balloon Payments: You must repay the entire principal balance at maturity, requiring careful cash flow planning.

- Limited Regulatory Oversight: Hard money loans lack the consumer protections and regulations that govern traditional mortgages.

- Prepayment Penalties: Many hard money lenders charge penalties if you pay off the loan early, though some don't.

- Higher Risk: If your project doesn't go as planned, you may struggle to make the balloon payment or refinance into a traditional loan.

Hard Money Loans vs. Traditional Mortgages

Understanding the differences helps you choose the right financing tool for your situation:

| Feature | Hard Money Loans | Traditional Mortgages |

|---|---|---|

| Lender Type | Private investors or companies | Banks and traditional lenders |

| Approval Focus | Property value | Credit score, income, debt-to-income ratio |

| Approval Timeline | 7-14 days | 30-45 days |

| Interest Rates | 8-15% | Currently around 6-7% (varies) |

| Loan Term | 6-24 months | 15-30 years |

| Down Payment | 20-30% | 3-20% |

| Payment Structure | Interest-only with balloon payment | Fixed monthly payments |

| Regulatory Oversight | Limited | Heavily regulated at federal and state level |

Qualifying for a Hard Money Loan

While hard money lenders are more flexible than traditional banks, they still evaluate your application. Here's what they typically consider:

- Credit Score: While not the primary factor, most lenders prefer a minimum credit score of 600-640. A lower score may require a larger down payment or additional collateral.

- Property Value: The property's current condition and after-repair value are critical. Lenders want to ensure they can recover their investment if they must foreclose.

- Exit Strategy: You'll need to explain how you plan to repay the loan—through a sale, refinance, or rental income.

- Investment Experience: Some lenders require real estate investing experience, though others don't. A strong business plan can improve your approval odds.

- Down Payment: Having 20-30% ready demonstrates your commitment and reduces the lender's risk.

- Rental Income: If the property is an investment rental, some lenders consider its rental income when evaluating the loan.

Finding Hard Money Lenders

Hard money lenders operate differently than banks. Here's how to find them:

- Real Estate Investment Networks: Connect with local real estate investment clubs and networking groups where hard money lenders often operate.

- Online Lending Platforms: Several companies specialize in hard money lending and accept applications online. Examples include Constitution Lending and other specialized lenders.

- Mortgage Brokers: Brokers who specialize in investment properties often have relationships with hard money lenders.

- Referrals: Ask other real estate investors for recommendations from lenders they've worked with successfully.

- Local Banks: Some community banks maintain relationships with private lenders and can provide referrals.

Frequently Asked Questions

Sources & References

-

1

www.offermarket.us — www.offermarket.us

-

2

www.herringbank.com — www.herringbank.com

-

3

www.housingwire.com — www.housingwire.com

-

4

www.housecanary.com — www.housecanary.com

-

5

www.tidalloans.com — www.tidalloans.com

-

6

www.chase.com — www.chase.com

Useful Tools

Related Articles

How to Use a "Qualified Small Business Stock" (QSBS) to Pay Zero Tax

If you're an investor, entrepreneur, or employee at a startup, you've probably heard the phrase "tax-free gains" and thought it sounded too good to be true. But there's actually a legitimate way to po...

How to Claim the "Employee Retention Credit" (ERC) in 2026: Is it Still Possible?

Imagine discovering tens of thousands of dollars in your business's pocket—funds you earned by keeping employees on payroll during the toughest days of the COVID-19 crisis. That's the promise of the E...

The Best "Virtual" Business Addresses for US LLCs in 2026

Starting a limited liability company (LLC) in 2026 means navigating smart choices for privacy, professionalism, and compliance. One key decision is picking the right business address—especially if you...

How to Transition from W-2 to Self-Employed: A Financial Checklist

Making the leap from a steady W-2 paycheck to self-employment is exciting—and terrifying. You're trading the security of regular income and employer benefits for freedom and control over your work. Bu...