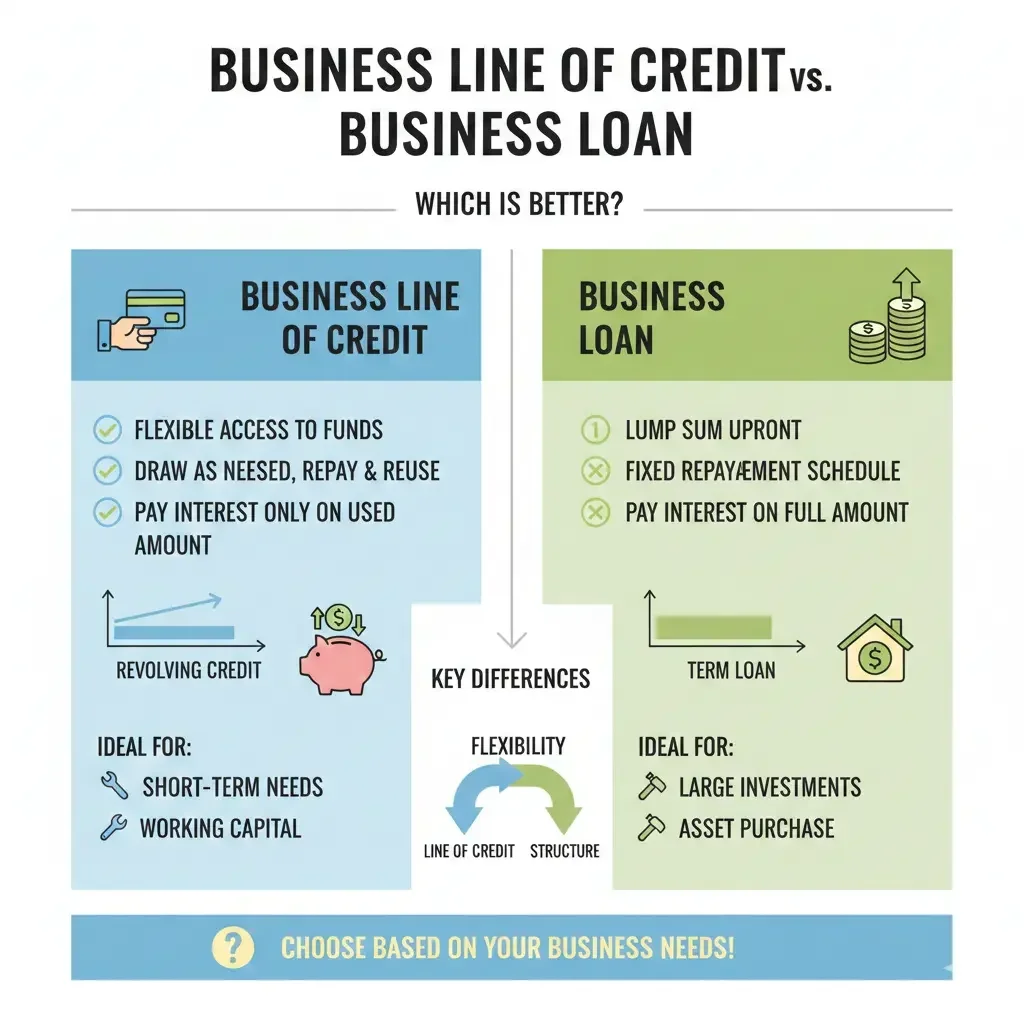

Business Line of Credit vs Business Loan: Which Is Better?

Imagine your small business in Denver is buzzing with holiday orders, but cash flow lags behind invoices. Do you grab a one-time chunk of cash with a business loan or tap into a flexible line of credi...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine your small business in Denver is buzzing with holiday orders, but cash flow lags behind invoices. Do you grab a one-time chunk of cash with a business loan or tap into a flexible line of credit as needs arise? Choosing between a business line of credit and a business loan can make or break your financial strategy in today's fast-paced U.S. market.

Both options fuel growth, but they serve different needs. A business line of credit acts like a credit card for your company—draw what you need, when you need it, up to a limit. A business loan delivers a lump sum upfront for bigger, planned expenses. We'll break down the differences, pros, cons, and real-world scenarios to help you decide which fits your American business best in 2026.

What Is a Business Line of Credit?

A business line of credit gives you revolving access to funds up to an approved limit, similar to a personal credit card but tailored for business use. Once approved, draw only what you need—say, $15,000 out of a $50,000 limit for inventory—and pay interest just on that amount. Repay it, and the credit replenishes for reuse.

In the U.S., lenders like banks, online platforms, and credit unions offer these, often with unsecured options for established businesses (no collateral required). Approval can happen in as little as 24 hours with less paperwork than loans. Interest rates typically range higher than loans but apply only to borrowed funds, and minimum payments offer flexibility.

Types of Business Lines of Credit

- Unsecured: No collateral needed; ideal for businesses with strong credit and revenue.

- Secured: Backed by assets like equipment; allows higher limits for riskier borrowers.

- Short-term vs. evergreen: Short-term for seasonal needs; evergreen renews annually.

Perfect for managing cash flow gaps, like bridging payroll during slow months or covering unexpected repairs.

What Is a Business Loan?

A business loan provides a one-time lump sum disbursed after approval, repaid in fixed monthly installments over a set term—often 2 to 6 years. Funds go toward specific goals, such as expanding your Atlanta storefront or buying machinery.

U.S. options include SBA loans (backed by the Small Business Administration for favorable terms), term loans from banks, or online lenders. These often require collateral for larger amounts and have stricter approval processes, taking weeks or months. But they shine with lower, fixed interest rates and predictable payments.

Common Types of Business Loans

- Term loans: Fixed amount for general use; SBA 7(a) loans up to $5 million.

- Equipment loans: Finance purchases where the asset serves as collateral.

- SBA loans: Government-guaranteed for small businesses; lower rates via sba.gov.

Great for one-off investments where you know the exact cost upfront.

Business Line of Credit vs. Business Loan: Key Differences

Here's a side-by-side comparison to highlight how they stack up in 2026:

| Feature | Business Line of Credit | Business Loan |

|---|---|---|

| Funding Style | Revolving; draw as needed up to limit | Lump sum, one-time |

| Repayment | Flexible minimums on drawn amount; interest-only option | Fixed monthly principal + interest |

| Interest Rates | Variable, higher (often 7-25%); only on used funds | Fixed, lower (5-15%); on full amount |

| Best For | Short-term, ongoing needs like cash flow | Long-term, large purchases |

| Approval Time | 24 hours to days; less docs | Weeks to months; more scrutiny |

| Collateral | Often unsecured | Usually required |

| Amounts | $10K-$250K typically | $50K-$5M+ (SBA) |

This table shows lines of credit prioritize flexibility, while loans favor predictability and scale.

Pros and Cons of Each Option

Business Line of Credit: Pros and Cons

Pros:

- Pay interest only on what you use—saving money during low-need periods.

- Quick access for emergencies or seasonal dips.

- Builds business credit with responsible use.

- Fewer restrictions on fund use (business purposes only).

Cons:

- Higher rates and potential fees (draw, annual).

- Lower limits; not for major expansions.

- Variable rates can rise with Fed hikes.

Business Loan: Pros and Cons

Pros:

- Lower rates and fixed payments for budgeting ease.

- Higher amounts for big projects like real estate.

- Clear payoff date reduces long-term uncertainty.

Cons:

- Collateral often required, risking assets.

- Lengthy approval; must reapply for more funds.

- Less flexibility if plans change.

When to Choose a Business Line of Credit Over a Loan

Opt for a line if your Phoenix retail shop faces unpredictable cash flow from tourism slumps. Use it for:

- Inventory buys during peak seasons.

- Payroll or vendor payments during invoice delays.

- Unexpected costs like equipment breakdowns.

It's revolving nature suits short-term needs without overborrowing.

When to Choose a Business Loan Over a Line of Credit

Go for a loan when funding a $200,000 warehouse expansion in Chicago—fixed terms match the long-term asset. Ideal for:

- Major equipment or vehicle purchases.

- Business acquisitions or renovations.

- Projects with known timelines and costs.

SBA loans via sba.gov offer competitive rates for qualified U.S. small businesses.

Factors to Consider Before Applying

Assess your business's health: Lenders check credit score (680+ FICO ideal), 6-24 months in business, and $100K+ annual revenue. Compare rates via nerdwallet.com or bankrate.com.

Shop multiple lenders—traditional banks for loans, online for lines. Factor in fees: origination (1-6% for loans), draw fees for lines. Check if you qualify for both; many businesses do if debt-to-income allows.

Real-World U.S. Examples

A Texas construction firm used a $100K line for material fluctuations amid supply chain issues. Meanwhile, a California tech startup secured an SBA term loan for office expansion, locking in 6.5% fixed rate.

"Business loans generally have better terms... lower interest rates, higher loan amounts."

Next Steps for Your Business

Review your cash flow needs: short-term flexibility? Line of credit. Big investment? Loan. Pull your business credit report via dun & bradstreet.com, then prequalify with 2-3 lenders. Consult sba.gov for free counseling or irs.gov for tax implications on interest deductions. Track the Federal Reserve's 2026 rate outlook to time your application—lower rates favor loans. Whichever you choose, use funds wisely to fuel sustainable growth.

Frequently Asked Questions

Sources & References

-

1

Business Line of Credit Vs. Loan: Comparing Funding Options — www.americanexpress.com

- 2

-

3

When to Use a Business Line of Credit vs. a Traditional Business Loan — www.academybank.com

- 4

-

5

Business Line of Credit or Business Loan – What's Right for You? — www.navyfederal.org

-

6

Best Business Lines of Credit of February 2026 - NerdWallet — www.nerdwallet.com

-

7

Business Line of Credit (LOC) vs. Loan: What's Best for You in 2026? — www.finder.com

Useful Tools

Related Articles

How to Use a "Qualified Small Business Stock" (QSBS) to Pay Zero Tax

If you're an investor, entrepreneur, or employee at a startup, you've probably heard the phrase "tax-free gains" and thought it sounded too good to be true. But there's actually a legitimate way to po...

How to Claim the "Employee Retention Credit" (ERC) in 2026: Is it Still Possible?

Imagine discovering tens of thousands of dollars in your business's pocket—funds you earned by keeping employees on payroll during the toughest days of the COVID-19 crisis. That's the promise of the E...

The Best "Virtual" Business Addresses for US LLCs in 2026

Starting a limited liability company (LLC) in 2026 means navigating smart choices for privacy, professionalism, and compliance. One key decision is picking the right business address—especially if you...

How to Transition from W-2 to Self-Employed: A Financial Checklist

Making the leap from a steady W-2 paycheck to self-employment is exciting—and terrifying. You're trading the security of regular income and employer benefits for freedom and control over your work. Bu...