What Is an Overdraft Fee and How Can You Avoid It?

Have you ever checked your bank account after a routine grocery run, only to find a sneaky $35 fee tacked on because you were a few dollars short? You're not alone—overdraft fees catch millions of Ame...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Have you ever checked your bank account after a routine grocery run, only to find a sneaky $35 fee tacked on because you were a few dollars short? You're not alone—overdraft fees catch millions of Americans off guard each year, turning small slip-ups into big headaches. In this guide, we'll break down exactly what an overdraft fee is, how it works, and share practical steps to dodge them entirely.

What Is an Overdraft Fee?

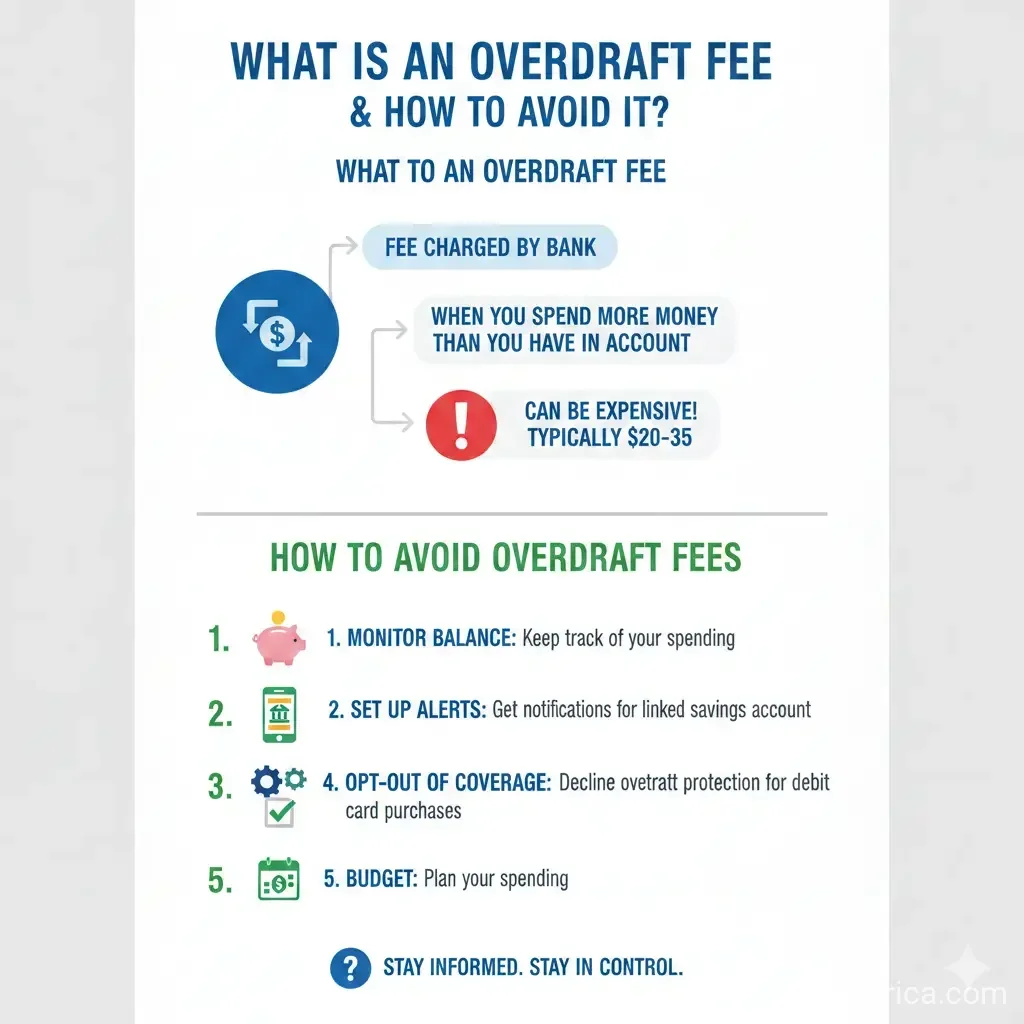

An overdraft fee is a charge your bank or credit union assesses when you spend more money than you have in your checking account, and they cover the shortfall anyway. Unlike a declined transaction, where the bank says "no" and might charge a non-sufficient funds (NSF) fee instead, an overdraft fee kicks in when the bank pays the transaction using its own funds—then bills you for both the overdraft amount and the fee.

How Overdraft Fees Work

Picture this: Your balance is $100, but you swipe your debit card for $125 at the store. If your bank honors the purchase (often called "courtesy pay" or "overdraft privilege"), they'll cover the $25 gap and hit you with a fee—typically around $35. Your new balance? A painful -$60. Banks process transactions in batches, often at the end of the day, so pending charges can pile up unexpectedly.

These fees aren't random; they're designed to offset the bank's processing costs and discourage risky spending. But in 2026, with rising living costs, they hit hardest on everyday Americans juggling bills.

Overdraft Fees vs. NSF Fees

Don't mix up overdraft fees with NSF fees. An overdraft fee applies when the bank pays the transaction; an NSF fee hits when they decline it, like bouncing a check. Both sting—NSF fees average $30-$35 too—but opting out of overdraft coverage often leads to more NSF charges on declined debit swipes.

How Much Do Overdraft Fees Cost in 2026?

Expect to pay $30 to $35 per overdraft item at most major U.S. banks, though some cap daily fees. Here's a snapshot of 2026 fees from big players:

- Chase: $34 per item over $50, max three per day ($102 total).

- Wells Fargo: $35 per item, max three per day.

- PNC: Around $36, with possible daily fees if unresolved.

- Huntington: No fee if overdrawn by $50 or less, thanks to their 24-Hour Grace buffer.

The FDIC notes fees hover around $35, but banks set their own rates—always check your account agreement. Multiple fees can snowball: One bad day with ATM withdrawals, debit swipes, and checks could rack up $100+.

"Banks may also charge continuous or daily overdraft fees, which are applied for each day your account stays overdrawn."

U.S. Regulations on Overdraft Fees

Federal rules protect you. Since the 2009 Regulation E rule from the Federal Reserve (now under CFPB), banks must get your opt-in consent before charging overdraft fees on ATM or one-time debit card transactions. You can opt in or out anytime—for free—giving you control.

In 2026, ongoing CFPB scrutiny pushes for fairer practices, like fee caps tied to actual costs or benchmarks around $5 for "true courtesy" overdrafts. Though a broader CFPB overdraft rule was repealed by Congress, core protections remain. State laws vary—California defines overdraft fees strictly for debit transactions exceeding balances. Visit consumerfinance.gov for your rights.

How to Avoid Overdraft Fees: 8 Practical Strategies

Dodging overdraft fees is easier than you think. Here's actionable advice tailored for U.S. bank customers:

1. Opt Out of Overdraft Coverage

Call your bank or log in online to opt out—it's your right under federal law. They'll decline transactions that overdraw, avoiding fees (though NSF might apply). Pro tip: Do this for ATM/debit unless you have backup protection.

2. Set Up Low-Balance Alerts

Most banks like Chase, Wells Fargo, and apps like Chime send free text/email alerts when your balance dips low. Enable them via your app to catch issues before they hit.

3. Link a Backup Savings Account

Overdraft protection transfers from savings (often $10-$12 per transfer) beat $35 fees. Set it up with banks like PNC—cheaper than courtesy pay.

4. Use Fee-Free Banking Options

Switch to banks without overdraft fees: Chime covers up to $200 with SpotMe (no fee for eligible users), Huntington's 24-Hour Grace skips fees under $50 overdrafts. Credit unions like NY Municipal often charge less.

5. Track Spending with Apps and Budgets

Apps like Mint or your bank's tools show real-time balances, including pending transactions. Budget 10-20% buffer in your account for surprises.

6. Time Deposits Strategically

Direct deposit hits vary—federal benefits like Social Security post same-day, paychecks might lag. Deposit cash early via ATM/mobile before midnight.

7. Ask for Waivers

If hit with a fee, call politely—many banks waive the first one for good customers. Document everything.

8. Leverage Grace Periods

Banks like Huntington give until next business day's midnight Central Time to deposit and avoid fees on overdrafts over $50.

| Strategy | Cost Savings | Best For |

|---|---|---|

| Opt Out | Up to $105/day | Low spenders |

| Fee-Free Bank | $0 fees | Frequent balancers |

| Alerts + Buffer | Prevents all | Everyone |

Take Control of Your Finances Today

Overdraft fees don't have to drain your wallet. Start by reviewing your bank's policy, opting out if needed, and setting alerts. Explore fee-free accounts for long-term wins. Small habits like checking balances weekly can save you hundreds yearly. Head to your banking app now—what's your first step?

Frequently Asked Questions

Sources & References

-

1

Overdraft Fee - Municipal Credit Union — www.nymcu.org

-

2

What Is An Overdraft Fee? How to Avoid & Calculate Them - Chime — www.chime.com

-

3

Myths vs. Facts – CFPB's Overdraft Final Rule — www.aba.com

-

4

What Is an Overdraft Fee? The Basics - NerdWallet — www.nerdwallet.com

- 5

-

6

What Are Overdraft Fees? | PNC Insights — www.pnc.com

-

7

Overdraft Fees Explained - Huntington Bank — www.huntington.com

-

8

Congress Repeals CFPB's Overdraft Rule — www.congress.gov

Related Articles

How to Handle "Identity Theft" in 2026: The First 24 Hours

Imagine checking your bank account on a quiet Saturday evening, only to discover unauthorized charges totaling thousands of dollars—or worse, spotting a new credit card opened in your name. In 2026, i...

The Best "Digital Banking" Apps for US Teens: A Parent's Guide

Imagine handing your teen a debit card that teaches them financial responsibility without the risk of overdrafts or debt. In 2026, digital banking apps make this possible, giving US parents powerful t...

The Best Online Banks with No Monthly Fees in 2026

Imagine ditching those pesky monthly bank fees that quietly eat into your budget every single month. In 2026, online banks make it easier than ever for Americans to enjoy truly free checking accounts...

How to Start an Emergency Fund from Scratch: $1 to $1;000

Picture this: Your car breaks down on the way to work, or an unexpected medical bill lands in your mailbox. Without a safety net, you're scrambling for credit cards or loans with sky-high interest rat...