How to Pay Off $50k in Student Loans on a Modest Salary

Carrying $50,000 in student loans on a modest salary feels overwhelming, but thousands of Americans tackle this every year and come out debt-free. With the right strategies, discipline, and knowledge...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Carrying $50,000 in student loans on a modest salary feels overwhelming, but thousands of Americans tackle this every year and come out debt-free. With the right strategies, discipline, and knowledge of 2026 federal changes, you can accelerate payoff without sacrificing your lifestyle.

Whether you're earning $40,000–$60,000 annually in teaching, retail, or entry-level office roles, these proven steps—tailored for U.S. borrowers—will help you pay off your loans faster. We'll cover budgeting basics, repayment tweaks, and updates from the One Big Beautiful Bill Act (OBBBA) that reshape options starting July 1, 2026.

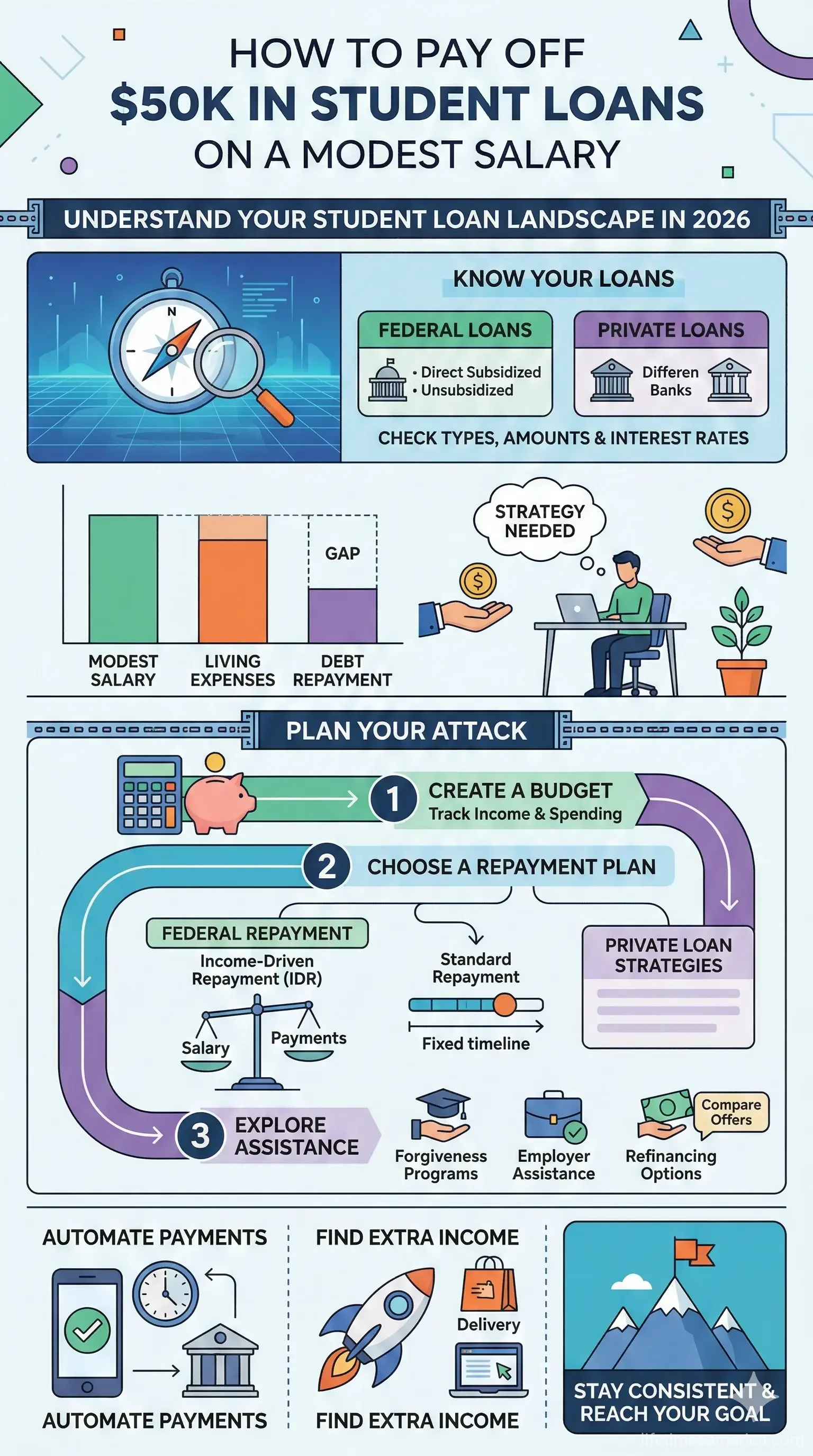

Understand Your Student Loan Landscape in 2026

Before diving into payoff tactics, know your loans. Federal loans dominate for most Americans, offering perks like income-driven plans. But OBBBA introduces big shifts: New borrowers after July 1, 2026, pick between a tiered standard plan (10–25 years based on balance) or the Repayment Assistance Plan (RAP), which bases payments on total adjusted gross income over 30 years. Pre-2026 loans keep access to older plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR).

Private loans lack these flexibilities, so check your servicer via StudentAid.gov. For $50k at 5% interest on a 10-year standard plan, expect ~$530 monthly payments. On a $50,000 salary, that's doable with cuts elsewhere.

Assess Your Current Plan

- Log into StudentAid.gov for your loan details, interest rates, and servicer.

- Compare plans: Standard (10 years, fixed) vs. income-driven (lower payments, longer term).

- Use the official Loan Simulator tool to model scenarios.

Build a Realistic Budget on a Modest Salary

Average U.S. household income hovers around $75,000, but many in service or admin jobs earn less. Start with the 50/30/20 rule: 50% needs, 30% wants, 20% savings/debt. On $45,000 after taxes (~$3,200/month), allocate $640 to debt while covering rent ($1,200), food ($400), and utilities ($300).

Track and Cut Expenses

- Automate tracking: Apps like Mint or YNAB categorize spending free.

- Slash big wins: Cook at home (save $200/month), cancel unused subscriptions ($50/month), carpool (save $100 gas).

- Housing hack: Roommates or suburbs drop rent 20–30%.

Example: One teacher paid off $55k in 7 years by meal-prepping and biking to work, freeing $300 extra monthly.

Top Strategies to Pay Off $50k Faster

Focus on principal reduction and interest savings. Here's how, with real math for a $50k loan at 4.5% interest.

1. Make Extra Principal Payments

Target principal early—interest accrues daily. Add $100/month to your $530 payment: Pay off in ~7.5 years, save $4,000 interest. Lump sums anytime work too; apply via servicer specifying "principal."

"By paying an extra $100 every month on a standard 10-year plan, you’d be debt-free about five and a half years ahead of schedule." — NerdWallet (adapted for $10k example)

2. Switch to Biweekly Payments

Pay half monthly (~$265) every two weeks: 26 half-payments = 13 full ones yearly. For $50k, shave 3–4 years, save $3,500 interest. Confirm your servicer allows; most do.

3. Enroll in Autopay for Discounts

Federal loans give 0.25% interest rate cut via autopay. On $50k at 5%, that's $125/year saved. Private lenders often match. Instant win—no extra effort.

4. Stick to or Optimize Repayment Plans

Standard 10-year plan is fastest if affordable: $50k gone in 120 payments. IDR lowers to 10% discretionary income (~$300 on $50k salary) but extends to 20–25 years, risking more interest. RAP (post-2026) mandates payments even on low income, up to 30 years.

Refinance private if rates drop below 4% and you skip forgiveness—but lose federal perks like Public Service Loan Forgiveness (PSLF).

5. Boost Income Without Burnout

- Side gigs: Drive Uber ($500/month), tutor online ($20/hour).

- Negotiate raise: 3–5% bump adds $150/month to loans.

- Tax refund: Average $2,800—dump into principal.

6. Explore Forgiveness and Relief

PSLF forgives after 10 years/120 payments in public/nonprofit jobs (teachers, nurses qualify). Teacher Loan Forgiveness: Up to $17,500 for 5 years. Check eligibility annually via StudentAid.gov.

Leverage 2026 OBBBA Changes Wisely

OBBBA streamlines but limits options. Pre-July 1, 2026 loans retain IBR/PAYE; consolidate before if needed to preserve. New graduate limits ($20,500/year, $100k lifetime) curb future debt, but for existing $50k, focus on RAP if income-based suits. RAP ties to AGI, forgives after 30 years—taxable.

| Plan | Term | Best For |

|---|---|---|

| Standard/Tiered | 10–25 years | Higher earners, quick payoff |

| RAP/IDR | 20–30 years | Modest salaries, forgiveness |

Common Pitfalls to Avoid

- Deferment/forbearance: Pauses payments but interest piles up.

- Co-signer refinance risks: Lose federal aid.

- Ignoring servicer: Always confirm extra payments apply to principal.

Your Next Steps to Debt Freedom

Today: Log into StudentAid.gov, run the Loan Simulator, and enroll in autopay. This month: Cut one expense, add $50 extra to principal. Track progress quarterly. Many Americans clear $50k in under 10 years—your modest salary won't stop you. Stay consistent, and celebrate milestones like every $5k paid.

Frequently Asked Questions

Sources & References

-

1

How to Pay Off Student Loans Fast: 7 Strategies for 2026 - NerdWallet — www.nerdwallet.com

-

2

How OBBBA reshapes student lending - Brookings Institution — www.brookings.edu

-

3

Federal Student Loans in 2026: What the One Big Beautiful Bill Act... - Citizens Bank — www.citizensbank.com

- 4

- 5

-

6

One Big Beautiful Bill Act Updates - Federal Student Aid — studentaid.gov

-

7

Student Loan Changes 2026: New Repayment Options... - NASFAA — www.nasfaa.org