What Is Medicare and When Does It Start?

Turning 65 soon? You're probably wondering about that big question on every retiree's mind: What is Medicare and when does it start? Medicare isn't just health insurance—it's your safety net for medic...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Turning 65 soon? You're probably wondering about that big question on every retiree's mind: What is Medicare and when does it start? Medicare isn't just health insurance—it's your safety net for medical costs in retirement, covering millions of Americans each year. Whether you're planning ahead or hitting eligibility age, understanding Medicare helps you avoid surprises and make smart choices for your health and wallet.

In this guide, we'll break down everything you need to know about Medicare, from its basics to 2026 costs, eligibility timelines, and practical steps to enroll. Let's dive in so you can focus on enjoying retirement.

What Is Medicare?

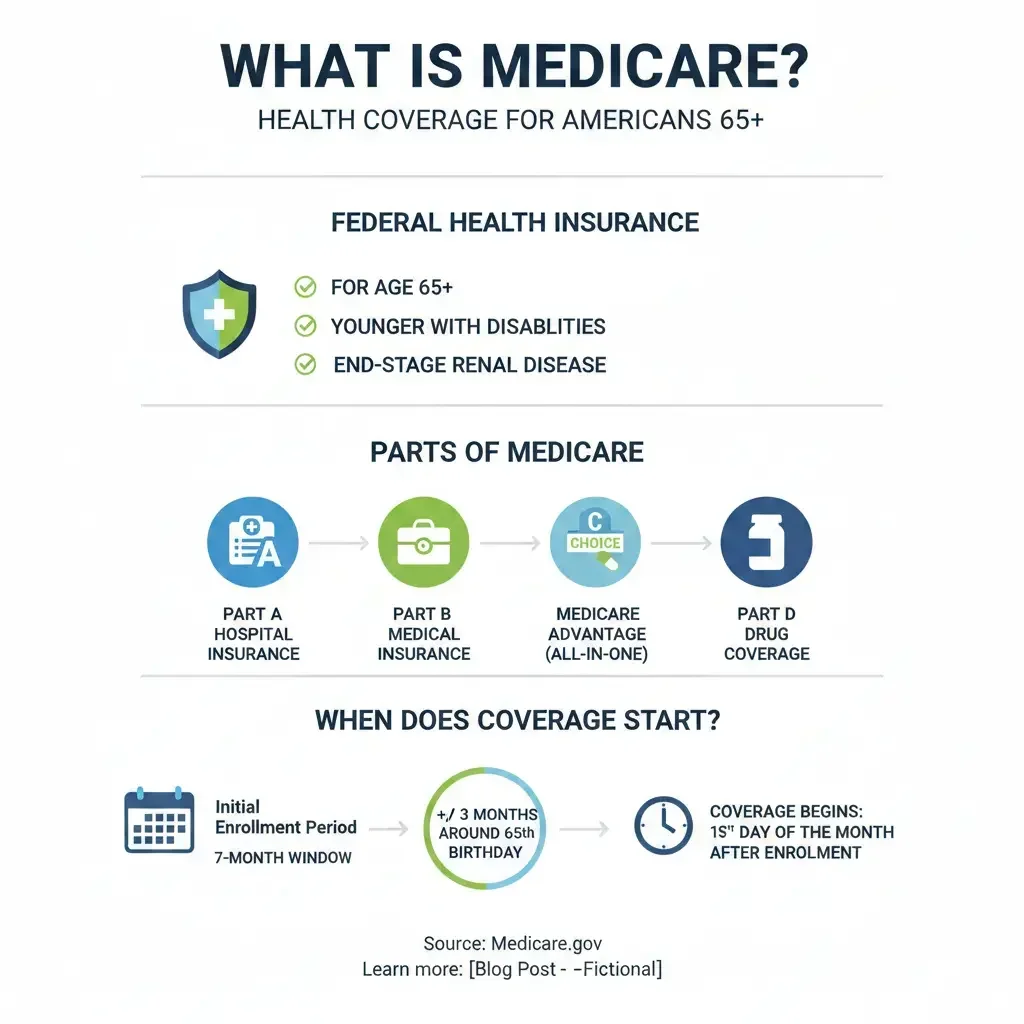

Medicare is a federal health insurance program in the United States that primarily serves people age 65 or older, as well as younger individuals with certain disabilities, end-stage renal disease, or amyotrophic lateral sclerosis (ALS, also known as Lou Gehrig's disease). Launched in 1965 under the Social Security Administration and now run by the Centers for Medicare & Medicaid Services (CMS), it acts as social insurance—funded partly through payroll taxes you pay while working—to help cover healthcare costs when you need it most.

Unlike private insurance, Medicare provides guaranteed benefits based on your work history and contributions, not just premiums. About 99% of beneficiaries qualify for premium-free Part A because they've worked at least 40 quarters (10 years) paying Medicare taxes. It's not free for everyone, though—premiums, deductibles, and copays apply, but it prevents medical bills from derailing your retirement savings.

The Four Parts of Medicare

Medicare breaks down into four main parts, each covering different needs:

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facilities, hospice, and some home health care. Most people get it premium-free.

- Part B (Medical Insurance): Pays for doctor visits, outpatient care, preventive services, and durable medical equipment like wheelchairs.

- Part C (Medicare Advantage): Private plans that bundle Parts A and B (often with Part D), adding extras like vision, dental, and hearing. Nearly all 2026 plans include these perks.

- Part D (Prescription Drugs): Helps with outpatient prescription costs through private stand-alone plans or those bundled in Part C.

Original Medicare (Parts A and B) is the foundation, but many add Medigap (supplemental insurance) or switch to Part C for more comprehensive coverage.

When Does Medicare Start?

Your Medicare start date depends on how and when you enroll. The key is your Initial Enrollment Period (IEP), a seven-month window around your 65th birthday: three months before, the month of, and three months after. Coverage timing varies:

- Enroll in the three months before your birthday month: Coverage starts the first day of your birthday month.

- Enroll in your birthday month: Starts July 1 if your birthday is January-June, or the first of your birthday month if later.

- Enroll in the first month after your birthday: Starts the first day of the second month after signup.

- Enroll in the next two months after: Starts the first day of the third month after.

If you're already receiving Social Security benefits before 65, you'll get automatically enrolled in Parts A and B—no action needed. For those still working with employer coverage, delay Part B to avoid penalties, but Part A is usually free and worth taking.

Special Enrollment for Workers and Abroad Travelers

Still employed at 65 with group health from a job or spouse? Use the Special Enrollment Period (SEP) when coverage ends—up to eight months after to avoid late penalties. Americans living outside the U.S. get a one-time Notice of Election window before or after extended stays.

Younger than 65? Medicare starts after 24 months of Social Security Disability Insurance (SSDI) or if you qualify via end-stage renal disease or ALS.

Medicare Eligibility Requirements

To qualify:

- Be 65 or older, or under 65 with disabilities/permanent kidney failure/ALS.

- U.S. citizen or legal resident for at least five continuous years.

- For premium-free Part A: 40 quarters of Medicare-covered work (or spousal credits).

Fewer than 30 quarters? Buy into Part A at $311/month in 2026 (up $26 from 2025). Everyone pays Part B premiums unless subsidized by Medicaid.

2026 Medicare Costs and Changes

Costs adjust annually based on the Social Security Act. Here's what to expect in 2026:

| Component | 2026 Amount | Change from 2025 |

|---|---|---|

| Part B Standard Premium | $202.90/month | Up $17.90 from $185 |

| Part B Annual Deductible | $283 | Up $26 from $257 |

| Part A Buy-In Premium (30+ quarters) | $311/month | Up $26 |

| Part D Out-of-Pocket Cap | $2,100/year | New cap from Inflation Reduction Act |

High earners pay more via income-related monthly adjustment amounts (IRMAA). For example, individuals with modified adjusted gross income over $109,000 (joint filers $218,000) add at least $14.50 to Part B. Part D deductibles rise slightly, but negotiated drug prices for 10 drugs save $1.5 billion in out-of-pocket costs.

Medicare Advantage and Part D Updates

Part C plans see behavioral health cost-sharing tweaks, automatic renewal for payment plans, insulin cap adjustments, and a slight out-of-pocket max increase. Part D caps catastrophic costs at $2,100, with premium stabilization subsidies dropping to $10/month. Average premiums shift, but extras like vision remain standard.

How to Enroll in Medicare

Enrollment is straightforward:

- Online: Create a my Social Security account at ssa.gov and apply for Part A/B.

- Phone: Call Social Security at 1-800-772-1213 (TTY 1-800-325-0778).

- In-Person: Visit your local Social Security office.

For Part C/D, use Medicare's Plan Finder tool at medicare.gov during Annual Enrollment (Oct 15-Dec 7). Compare plans based on your doctors, drugs, and costs—actionable tip: List your top three medications and preferred providers before shopping.

Practical Tips for Medicare Success

- Don't Delay Part A: It's usually free and pairs with employer plans.

- Assess Gaps: Original Medicare lacks out-of-pocket caps—consider Medigap or Advantage.

- Watch Penalties: Late Part B signup adds 10% premium per year delayed.

- Review Annually: Costs and plans change; check during Open Enrollment.

- Get Help: Use SHIP counselors (free via state health insurance programs) or 1-800-MEDICARE.

Frequently Asked Questions

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...