How to Buy a Foreclosed Property: A Beginner’s Guide to REOs

Imagine snagging a spacious family home in your dream neighborhood at 20-30% below market value— that's the allure of buying a foreclosed property, specifically an REO (Real Estate Owned) home. These...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine snagging a spacious family home in your dream neighborhood at 20-30% below market value— that's the allure of buying a foreclosed property, specifically an REO (Real Estate Owned) home. These bank-owned gems offer savvy American buyers a shot at real estate investing or homeownership without breaking the bank, but they come with unique hurdles like "as-is" sales and repair needs. This beginner's guide walks you through every step to buy an REO property confidently in 2026.

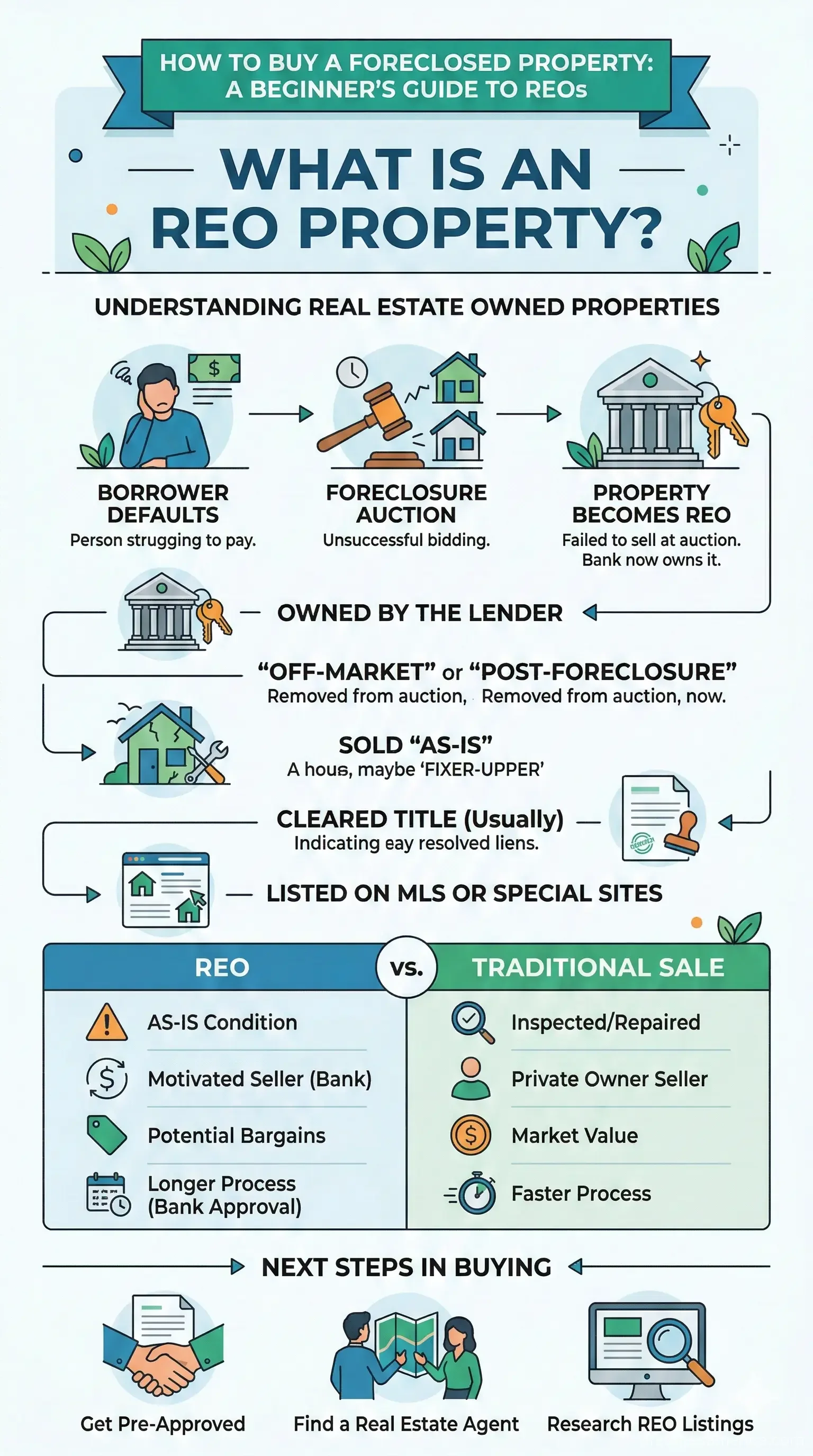

What Is an REO Property?

REO properties are homes owned by banks or lenders after a foreclosure process. When a homeowner defaults on their mortgage, the lender repossesses the property. If it doesn't sell at a public auction, it becomes bank-owned—hence REO—and is listed for sale to recover losses. Unlike pre-foreclosure deals (where you negotiate with the owner) or auctions (which demand cash and carry risks), REOs offer a cleaner title with most liens cleared, making them ideal for first-time foreclosure buyers.

In the U.S., government-backed REOs from agencies like HUD, VA, USDA, and Fannie Mae add even more options, often with buyer incentives like low down payments. As of 2026, rising interest rates have kept inventory tight, but REOs remain a hot opportunity for deals in states like Florida, Texas, and California.

Why Buy an REO Property? Pros and Cons

The Advantages

- Discounted Prices: Banks price REOs at or near market value to sell fast, often 10-30% below comparable homes, especially if repairs are needed.

- Clean Title: Lenders typically evict occupants and clear liens before listing, reducing legal headaches.

- Financing Flexibility: Use standard mortgages, FHA 203(k) loans for fixes, or even VA/USDA options if eligible.

- Investor-Friendly: Great for flipping or rentals, with fewer emotional sellers involved.

The Risks to Watch

- "As-Is" Condition: No seller repairs or disclosures—expect hidden issues like roof leaks or plumbing woes since banks rarely maintain them.

- Competition: Cash investors snap up deals quickly.

- Longer Approvals: Offers need bank and sometimes investor sign-off, delaying closings.

- Appraisal Gaps: Low appraisals are common; you may cover the difference or lose financing.

Bottom line: REOs suit prepared buyers who budget 10-20% extra for surprises. Always weigh these against traditional buys, where inspections rule and prices reflect upkeep.

Step-by-Step Guide: How to Buy a Foreclosed REO Property

Step 1: Get Financially Ready

Start with a mortgage pre-approval—it's non-negotiable. Lenders scrutinize your credit, income, and reserves more than for regular homes. Aim for proof of funds if paying cash, and discuss REO-specific loans like FHA 203(k), which bundles purchase and rehab costs up to FHA standards (e.g., working utilities, no major hazards). In 2026, expect rates around 6-7% for qualified buyers; check Bank of America or NewRez for REO-friendly products.

Actionable Tip: Use free tools on CFPB's Owning a Home site to calculate affordability, including repair buffers.

Step 2: Find REO Listings

Search beyond Zillow or Redfin—REOs hide on specialized sites:

- Bank websites: Bank of America Foreclosures, Chase REO listings.

- Government portals: HUD Homes, VA Homes, Fannie Mae HomePath.

- MLS flagged as "REO" or "bank-owned" via local agents.

- Auction sites like Auction.com for transitioning REOs.

Hire a foreclosure-savvy real estate agent—they access exclusive listings and comps (comparable sales from the last 180 days). Pro tip: Set alerts for your zip code to beat investors.

Step 3: Research and Inspect Thoroughly

Run a comparative market analysis (CMA) to bid smart—factor in repairs via a professional inspection if allowed (not always in "as-is" REOs). Always order a title search through a company like First American Title; even REOs can have surprises. Buy title insurance—it's cheap peace of mind against liens or judgments.

"Never assume that the title is clear without having a professional check it."

Step 4: Make a Competitive Offer

Offer at market value minus repair costs—banks want fair deals to move inventory fast. Include an appraisal contingency to renegotiate if values dip. Submit via your agent with pre-approval; cash beats financed offers. Expect 1-2 weeks for multi-level approvals.

Step 5: Close the Deal

Once accepted, appraisals and underwriting proceed like standard sales, but faster since banks push closings. Budget for higher closing costs (3-5%) and walk-throughs to confirm vacancy. Congrats—you're a REO owner!

Financing Your REO Purchase in 2026

Conventional mortgages work, but FHA 203(k) shines for fixers—finance up to $35,000 in repairs (limits vary by county; check HUD.gov). VA and USDA REOs offer zero-down for eligible vets or rural buyers. Pre-approve with the owning lender for priority. Avoid pitfalls: Some require 10-20% down for investment properties.

Common Mistakes to Avoid

- Skipping Inspections: "As-is" doesn't mean blind buying—inspect utilities and structure.

- Lowball Offers: Banks reject unrealistic bids; use comps.

- Ignoring Reserves: Stash 6 months' expenses for post-purchase fixes.

- No Agent: Go solo and miss insider access.

- Overleveraging: Don't buy beyond your budget—foreclosures aren't always steals.

Ready to Dive In? Your Next Steps

Buying an REO property can build wealth or secure your family's future—start today by getting pre-approved and connecting with a local agent via the National Association of Realtors (realtor.com). Research listings on HUD.gov, budget for inspections/title insurance, and remember: patience pays off. With smart prep, you'll navigate 2026's market like a pro and claim your foreclosure win.

Frequently Asked Questions

Sources & References

-

1

How to buy a foreclosed home - Bank of America Foreclosures — foreclosures.bankofamerica.com

-

2

Buying a Bank-Owned Property — www.zillow.com

-

3

REO Homes: A Step-by-Step Guide to Buying Bank-Owned Properties — www.newrez.com

-

4

Buying a Foreclosed Home in 2026: 7 Things You Need to Know — www.amerisave.com

-

5

How to Buy a Foreclosed Home: The Ultimate Guide — www.redfin.com

-

6

How To Buy A Foreclosed Home, Step-By-Step — www.bankrate.com

-

7

How to Buy Foreclosure Properties: A Guide for Real Estate Investors — semiretiredmd.com

-

8

The REO Guide: 10 Steps to Buying a Bank-Owned Home - Pennymac — www.pennymac.com

-

9

A guide to REO properties: How to buy & finance them — www.chase.com