How Much Should You Spend on Rent Each Month?

Imagine finally finding that perfect apartment in your dream neighborhood, only to realize the rent payment leaves you scraping by until payday. You're not alone—millions of Americans grapple with thi...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine finally finding that perfect apartment in your dream neighborhood, only to realize the rent payment leaves you scraping by until payday. You're not alone—millions of Americans grapple with this dilemma every month. Deciding how much you should spend on rent each month is crucial for financial stability, especially in 2026's competitive housing market where median rents hover around $1,367 nationwide. This guide breaks down proven rules, calculations, and real-world tips tailored for U.S. renters to help you budget smartly without sacrificing your lifestyle.

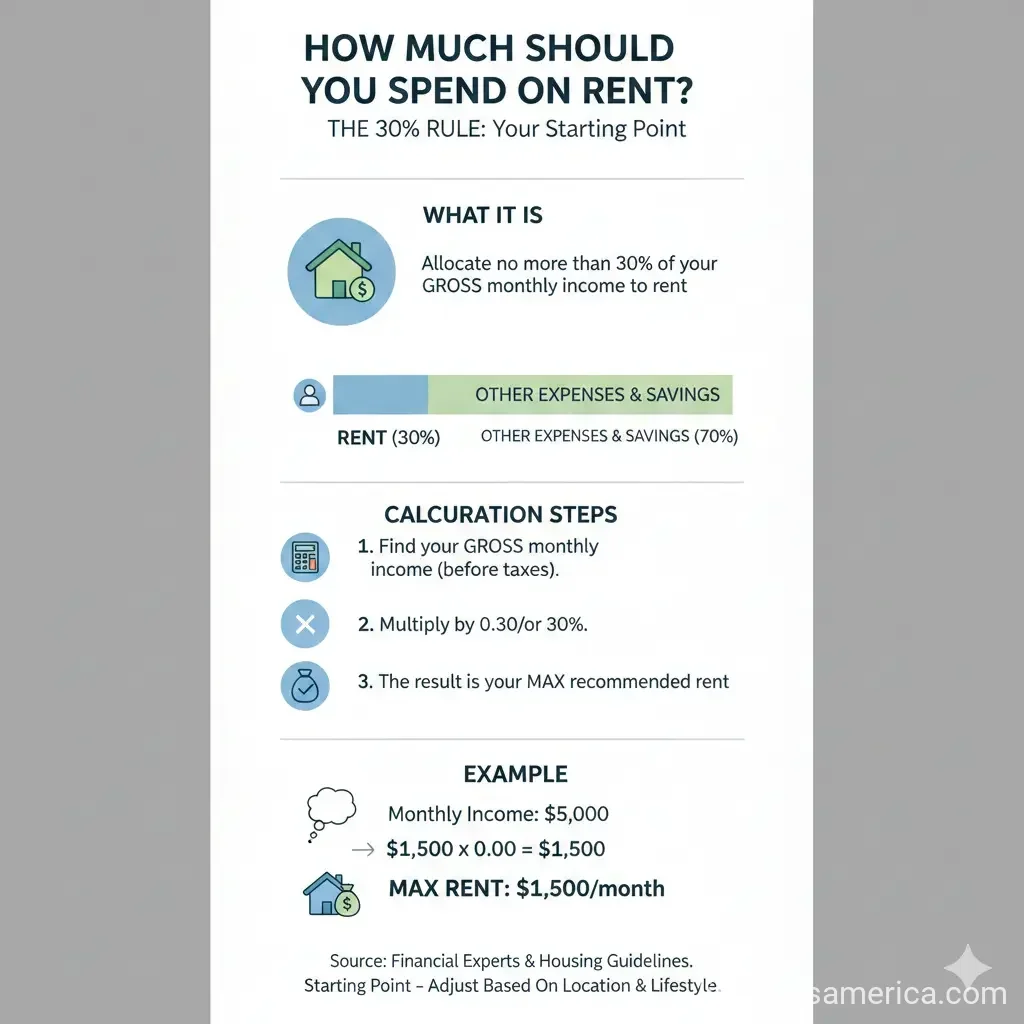

The 30% Rule: Your Starting Point for Rent Affordability

The most widely recommended guideline is the 30% rule, which suggests spending no more than 30% of your gross monthly income on rent, excluding utilities. This benchmark originated decades ago but remains a cornerstone for landlords and financial advisors alike, as it leaves room for other essentials like groceries, transportation, and savings.

For example, if your gross annual salary is $60,000, your monthly gross income is $5,000. At 30%, you'd aim for rent no higher than $1,500. Landlords often use this ratio too—income must be at least three times the rent, meaning a $2,000 apartment requires $6,000 monthly gross income.

Why 30% Works (and When It Doesn't)

- Low ratio (under 30%): Ideal for building savings or tackling debt—think 24% for that $1,200 rent on $5,000 income.

- Moderate (30-50%): Manageable short-term but risky if unexpected costs arise, like car repairs.

- Over 50%: High strain; prioritize cutting costs or finding roommates.

In high-cost cities like New York or San Francisco, sticking to 30% can feel impossible. Research local averages—use tools from Apartments.com or Redfin calculators to adjust realistically.

Step-by-Step: How to Calculate Your Ideal Rent Budget

Calculating your rent-to-income ratio is straightforward and empowers you to negotiate or hunt smarter. Follow these steps using your gross income (pre-tax, pre-deductions):

- Find your gross annual income from your paystub or W-2.

- Divide by 12 for monthly gross income.

- Multiply by 0.30 for your max rent.

- Subtract utilities (average $150-300/month) for total housing costs.

Real U.S. Salary Examples Based on 30% Rule

| Annual Gross Income | Monthly Gross Income | Max Monthly Rent (30%) |

|---|---|---|

| $30,000 | $2,500 | $750 |

| $40,000 | $3,333 | $1,000 |

| $50,000 | $4,167 | $1,250 |

| $75,000 | $6,250 | $1,875 |

| $100,000 | $8,333 | $2,500 |

These figures are pre-utilities and don't account for taxes—withholdings via IRS Form W-4 can reduce take-home pay by 20-30%. Always verify with a rent affordability calculator.

Beyond the 30% Rule: Smarter Budgeting Frameworks

While 30% is a solid start, integrate it into broader strategies like the 50/30/20 rule, popularized by experts and suitable for after-tax (net) income. Allocate:

- 50% to needs: Rent, utilities, groceries, minimum debt payments, renter's insurance, and retirement like 401(k) contributions.

- 30% to wants: Dining out, entertainment, travel.

- 20% to savings/debt: Emergency fund (3-6 months expenses), extra student loans, or down payment savings.

Example: On $4,000 net monthly income, that's $2,000 needs (rent capped inside), $1,200 wants, $800 savings. For tighter budgets, try 60/30/10: 60% needs, 30% wants, 10% savings/debt—better for high-debt or low-income households.

"The 30% rule is actually pretty outdated—it originated in 1969... Research the average rent costs in your neighborhood."

Factors Unique to American Renters in 2026

U.S. housing varies wildly—national median rent is $1,367 (Dec 2025 data), but expect $2,500+ in coastal metros vs. $900 in Midwest towns. Consider:

Location and Market Trends

Federal resources like the Bureau of Labor Statistics (BLS) track Consumer Price Index (CPI) for rent—up 3-5% annually. Check HUD's Fair Market Rents for your zip code to gauge affordability. In 2026, remote work trends let many afford pricier homes if commuting drops.

Other Expenses and Lifestyle

- Utilities and add-ons: Add $200-400 for electricity, internet; some states offer LIHEAP aid for low-income households.

- Debt and savings: Factor student loans (average $37,000), car payments, or Medicare/Medicaid gaps if applicable.

- Lifestyle: Frequent travelers might stretch to 35%; homebodies save on utilities.

Landlord Requirements and Legal Protections

Landlords screen via rent-to-income (3x rent rule). Know your rights—Fair Housing Act prohibits discrimination; use usa.gov for tenant resources. In rent-controlled areas like parts of California, caps limit hikes.

Practical Tips to Stretch Your Rent Budget

- Get roommates: Splits costs; apps like Roomi make it easy.

- Negotiate rent: Offer longer leases or prepay for discounts—common in softening 2026 markets.

- Build credit: Higher FICO scores unlock better apartments; free via AnnualCreditReport.com.

- Track everything: Use apps like Mint or YNAB to monitor spending.

- Save for emergencies: Aim for $1,000 starter fund before big moves.

- Explore assistance: Section 8 vouchers via HUD for eligible low-income Americans.

Take Control of Your Rent Budget Today

Armed with the 30% rule, 50/30/20 framework, and these tools, you're set to find rent that fits your life—not the other way around. Start by plugging your numbers into a free calculator, review your full budget, and scout listings on sites like Zillow or Apartments.com. If over 30%, cut wants or seek aid. Consistent tracking builds wealth—whether renting long-term or eyeing homeownership via FHA loans. Your financial future starts with this decision.

Frequently Asked Questions

Sources & References

- 1

-

2

How Much Rent Can I Afford? - Rent Calculator - Apartments.com — www.apartments.com

-

3

How Much Rent Can I Afford? - Rent Affordability Calculator - Redfin — www.redfin.com

-

4

How Much Rent Can I Afford? Complete Guide - Bungalow — bungalow.com

-

5

How Much Should I Spend On Rent? - NerdWallet — www.nerdwallet.com

-

6

Rent-to-Income Ratio Calculator - TurboTenant — www.turbotenant.com

Related Articles

How to Build a 6-Month Emergency Fund on a Minimum Wage

Building a six-month emergency fund on minimum wage might feel impossible, but it's more achievable than you think. With the right strategy and consistent effort, you can create a financial safety net...

The Best "Financial Literacy" Books Every American Should Read in 2026

Imagine standing at the edge of financial freedom, armed with knowledge that turns everyday dollars into lifelong security. In 2026, with inflation hovering around 2.5% and retirement accounts like 40...

How to Avoid "Lifestyle Creep" After a 2026 Promotion

Picture this: You've just landed that well-deserved promotion in 2026, your salary jumps by 20% or more, and suddenly you're eyeing a sleeker car, fancier dinners out, or that home upgrade you've alwa...

The Best Cashback Apps for Grocery Shopping in 2026

Imagine slashing your grocery bill by hundreds of dollars each year without clipping coupons or hunting for sales. In 2026, cashback apps make it simple for Americans to earn real money back on everyd...