Medicare Part A vs. Part B: A Simplified Guide for Seniors

Turning 65 brings excitement about retirement, but it also means navigating Medicare—a lifeline for healthcare that can feel overwhelming. If you're a senior or caring for one, understanding Medicare...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Turning 65 brings excitement about retirement, but it also means navigating Medicare—a lifeline for healthcare that can feel overwhelming. If you're a senior or caring for one, understanding Medicare Part A vs. Part B is your first step to smart coverage choices without breaking the bank.

These two core parts form Original Medicare, covering hospital stays and doctor visits, respectively. With 2026 premiums and deductibles on the rise, knowing the differences helps you avoid penalties, minimize out-of-pocket costs, and pair them with options like Medigap or Medicare Advantage. Let's break it down simply, with 2026 numbers and tips tailored for Americans.

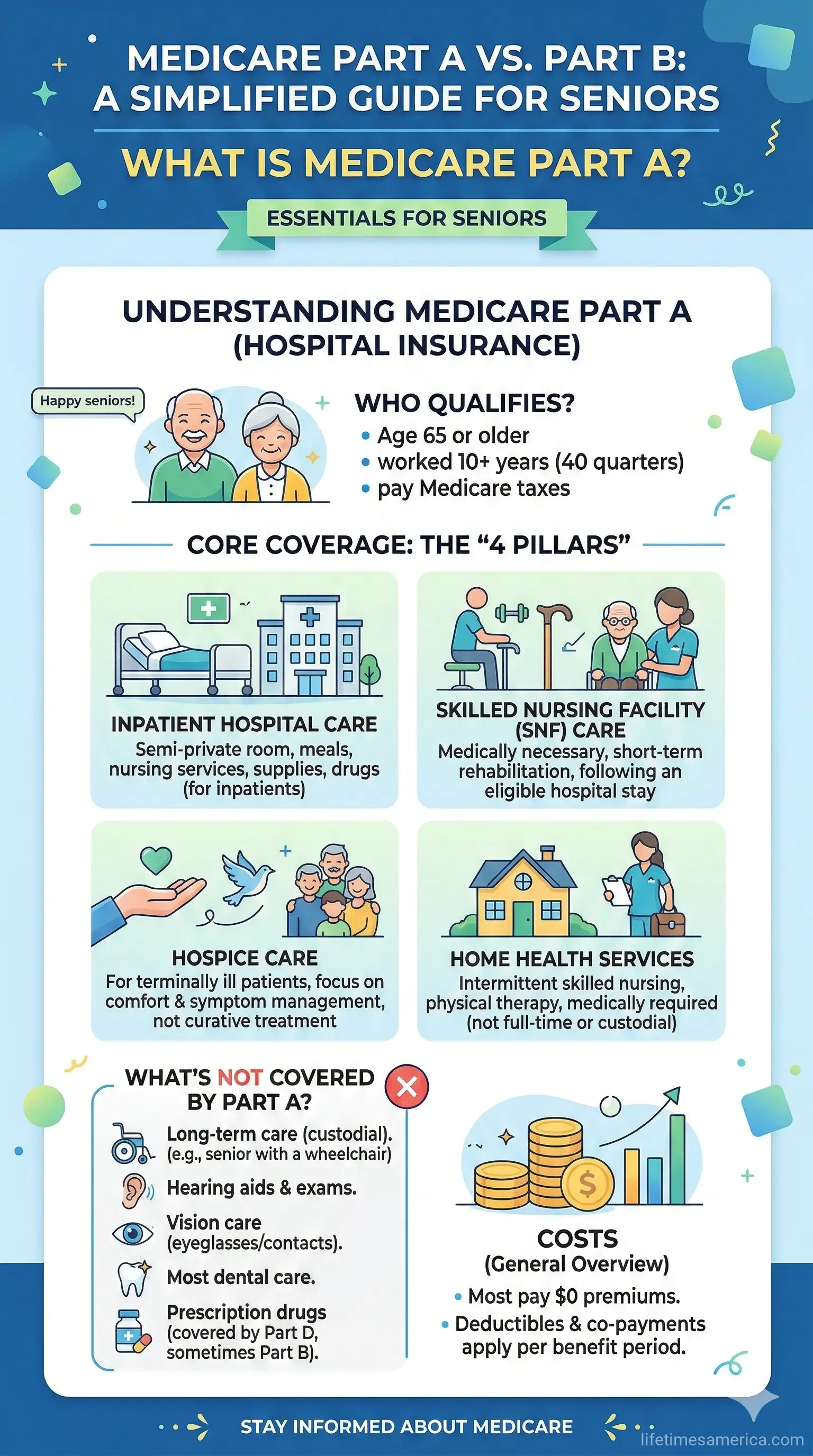

What is Medicare Part A?

Medicare Part A, often called Hospital Insurance, covers inpatient care essentials so you don't face massive bills during a health crisis. It's the foundation for most seniors, with about 99% qualifying premium-free if they've worked at least 40 quarters (10 years) paying Medicare taxes.

What Does Part A Cover?

- Inpatient hospital stays, including semiprivate rooms, meals, general nursing, and drugs as part of care.

- Skilled nursing facility (SNF) care after a qualifying hospital stay (up to 100 days per benefit period).

- Hospice care for terminal illness.

- Some home health care, like part-time skilled nursing or physical therapy.

- Inpatient rehabilitation facility services.

These benefits kick in after you meet the deductible, making Part A crucial for unpredictable hospital needs.

Part A Costs in 2026

Most don't pay a monthly premium, but costs include deductibles and coinsurance:

A "benefit period" starts when admitted and ends after 60 days without hospital or SNF care. Plan for these by saving or buying Medigap to cover coinsurance.

What is Medicare Part B?

Medicare Part B, or Medical Insurance, handles outpatient and preventive services—think doctor appointments and preventive screenings to keep you healthy. Everyone pays a premium, deducted from Social Security unless you're billed directly.

What Does Part B Cover?

- Doctor and specialist visits (in-office or outpatient).

- Outpatient hospital services, like ER visits or surgery.

- Preventive services at no cost (e.g., annual wellness visits, flu shots, mammograms).

- Durable medical equipment (walkers, oxygen).

- Mental health services, ambulance rides, and some home health.

After the deductible, you pay 20% coinsurance. It's voluntary but skipping it when first eligible (age 65 or after 24 months of disability) triggers lifelong penalties.

Part B Costs in 2026

Expect these standard rates, with higher-income adjustments via IRMAA (Income-Related Monthly Adjustment Amount):

High earners pay more: For example, individuals with 2024 income over $109,000 face surcharges up to hundreds extra monthly. Social Security notifies you of your exact amount.

Medicare Part A vs. Part B: Key Differences

Here's a side-by-side to clarify Medicare Part A vs. Part B:

| Aspect | Part A (Hospital) | Part B (Medical) |

|---|---|---|

| Main Coverage | Inpatient hospital, SNF, hospice. | Outpatient, doctors, preventive. |

| Premium | $0 for most; up to $563 if needed. | $202.90 standard; income-based add-ons. |

| Deductible (2026) | $1,736 per benefit period. | $283 annual. |

| Coinsurance | Daily after 60 days ($434/day days 61-90). | 20% after deductible. |

| Enrollment | Automatic if eligible. | Automatic but can decline; penalties for late sign-up. |

Part A focuses on big hospital events; Part B on routine care. Together, they cover 80% of approved costs—you handle the rest unless supplemented.

When and How to Enroll in Parts A and B

Your Initial Enrollment Period (IEP) spans the 3 months before your 65th birthday month, the birthday month, and 3 after. Coverage starts the first of your birthday month (or prior if birthday is the 1st).

Under 65 with disability? Part A/B starts after 24 months of Social Security disability benefits. Live in Puerto Rico? Sign up for Part B manually.

Actionable tip: Use the General Enrollment Period (Jan 1-Mar 31) if you miss IEP, but expect penalties. Check eligibility at ssa.gov/medicare or call 1-800-MEDICARE.

Costs and Ways to Save on Parts A and B

2026 hikes—Part A deductible up 3.58%, Part B premium up 9.68%—mean planning ahead. Strategies:

- Medigap (Medicare Supplement): Private plans cover deductibles/coinsurance. Shop during Open Enrollment (6 months from Part B start) for guaranteed issue—no medical underwriting.

- Medicare Advantage (Part C): Bundles A/B with extras; 32% offer Part B rebates (paying part of your $202.90 premium). But networks may limit doctors.

- Low-Income Help: Medicare Savings Programs or Extra Help via SSA if income-eligible.

- HSAs/Employer Coverage: If still working, weigh keeping group plans—coordinate with Medicare.

High costs? Appeal denials or request financial help at medicare.gov/claims-appeals.

Common Mistakes to Avoid

- Dropping Part B too soon—late penalties are 10% per year delayed, permanent.

- Ignoring IRMAA—report income changes to IRS/SSA.

- Not comparing Advantage plans—check star ratings and networks at Medicare Plan Finder.

- Forgetting preventive care—Part B covers 100% of many screenings.

Next Steps for Smarter Medicare Choices

Review your Medicare Summary Notice yearly and use the Plan Finder tool at medicare.gov/plan-compare during Open Enrollment (Oct 15-Dec 7). Contact State Health Insurance Assistance Program (SHIP) for free counseling—find yours at shiphelp.org. With rising 2026 costs, act now: enroll properly, explore supplements, and save thousands in potential expenses. You're in control—get covered right.

Frequently Asked Questions

Sources & References

-

1

2026 Medicare Parts A & B Premiums and Deductibles - CMS — www.cms.gov

- 2

- 3

-

4

Medicare and You Handbook 2026 — www.medicare.gov

-

5

Fact sheet: 2026 Medicare costs — www.medicare.gov

-

6

Costs | Medicare — www.medicare.gov

-

7

2026 Medicare Premiums Announced — www.medicarerights.org