What Is a Wire Transfer and When Should You Use It?

Imagine you're closing on a new home in Texas, and the seller needs funds wired by noon to seal the deal—or you're supporting family overseas and want money in their account today. In these high-stake...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine you're closing on a new home in Texas, and the seller needs funds wired by noon to seal the deal—or you're supporting family overseas and want money in their account today. In these high-stakes moments, a wire transfer steps in as the fastest, most reliable way to move money electronically across banks in the U.S. or beyond. Whether you're handling a large real estate transaction or urgent business payment, understanding what a wire transfer is and when to use it can save you time, stress, and unexpected fees.

Wire transfers have been a banking staple for decades, powering everything from home purchases to international remittances. In 2026, with digital banking at our fingertips, they're more accessible than ever—but they come with fees, security rules, and specifics tied to U.S. regulations. This guide breaks it all down, so you can decide if a wire is right for your next big money move.

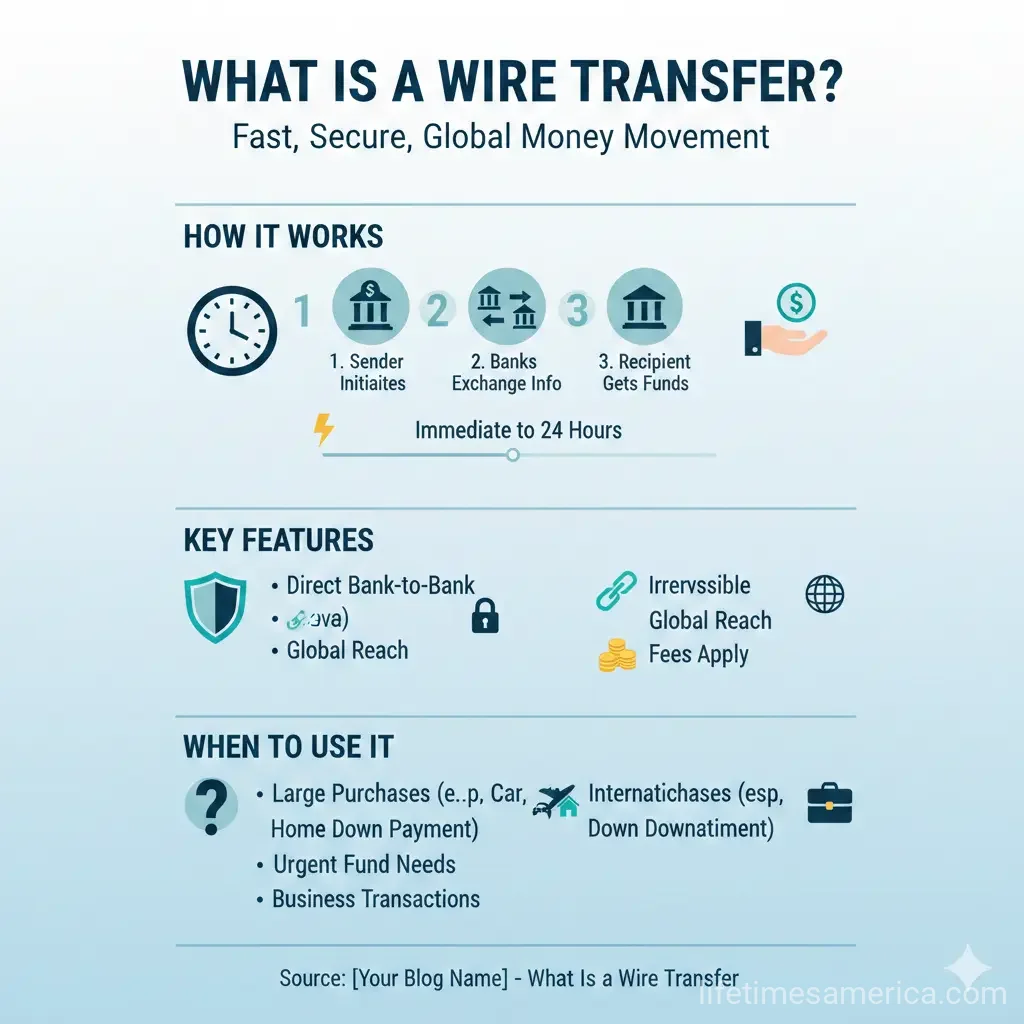

What Is a Wire Transfer?

A wire transfer is an electronic method to send money directly from one bank account to another, either domestically or internationally, without physical cash or checks changing hands. It's like an instant digital courier for funds, instructed by you through your bank or a service like Western Union.

Unlike slower options like ACH transfers—which batch payments through the Automated Clearing House network—wires offer real-time or same-day settlement. In the U.S., domestic wires typically zip through the Federal Reserve's Fedwire network, a secure system handling trillions daily for banks, businesses, and consumers.

Key Features of Wire Transfers

- Speed: Domestic wires often settle same-day; international ones take 1-5 business days.

- Security: Funds are verified before sending, and transfers can't be easily reversed—making them ideal for trusted recipients.

- High Limits: No strict caps like some apps; you can send over $10,000 easily.

- Irrevocable: Once sent, it's final, so double-check details.

Legally, wire transfers fall under U.S. banking laws, including the Bank Secrecy Act, which requires banks to report transactions over $10,000 to the IRS for anti-money laundering efforts.

How Does a Wire Transfer Work?

Sending a wire starts with you providing precise details to your bank. Here's the step-by-step process for U.S. users in 2026:

- Gather Recipient Info: Full name, address, phone, bank name, routing number (for domestic), account number, and SWIFT/BIC code (for international).

- Fund the Transfer: Pay from your checking, savings, or money market account—funds must be available upfront.

- Initiate at Your Bank: Visit a branch, call, or use online/mobile banking. Your bank sends instructions via Fedwire (domestic) or SWIFT (international).

- Intermediary Verification: Banks confirm funds and details; any issues halt the process.

- Delivery: Recipient's bank credits their account—often same-day for domestic.

For example, wiring $50,000 for a car purchase at a California dealership? Provide their bank details, pay your bank's fee (typically $25-$50 outgoing), and funds land securely that day.

Domestic vs. International Wires

Domestic wires stay within the U.S., using Fedwire or CHIPS networks for quick, low-fee transfers—perfect for real estate closings or lawyer payments. They usually clear in hours.

International wires, or remittances, cross borders via SWIFT. Consumer Financial Protection Bureau (CFPB) rules mandate disclosures: exchange rates, all fees (sender, recipient, intermediaries), and the exact amount received. Expect 1-5 days and higher costs ($40-$75 outgoing).

| Type | Network | Speed | Typical Fees (2026 Est.) |

|---|---|---|---|

| Domestic | Fedwire/CHIPS | Same-day | $25-$50 outgoing |

| International | SWIFT | 1-5 days | $40-$75 + FX markup |

When Should You Use a Wire Transfer?

Use wires when speed and certainty trump cost. They're not for everyday bills—save those for free ACH—but shine in urgent, high-value scenarios.

Top Situations for U.S. Users

- Real Estate Closings: Sellers demand wired funds at closing to ensure availability—common in competitive markets like Florida or New York.

- Business Payments: Paying suppliers, payroll emergencies, or M&A deals need same-day settlement.

- Emergencies: Medical bills, family support abroad, or tuition deadlines.

- Court-Ordered or Legal Fees: Divorce settlements or escrow releases require irrevocable proof.

- Large Purchases: Cars, boats, or investments over $10,000, where cash is risky.

Avoid wires for untrusted parties—scams exploit their irreversibility. The FBI reports billions lost yearly to wire fraud; always verify recipients.

Wire Transfer Fees and Costs in 2026

Expect to pay: outgoing domestic ($25-$50), international ($40-$75 plus 1-3% FX markup), and incoming ($10-$30). Credit unions like Navy Federal often charge less—shop around.

Pro Tip: Ask for fee breakdowns upfront. CFPB rules ensure transparency for international sends.

Alternatives to Wires

- ACH: Cheaper (often free), but 1-3 days.

- Zelle or Venmo: Free for small P2P, instant, but low limits ($2,500/day).

- Wise or Remitly: Low-fee international with mid-market rates.

Security and U.S. Regulations

U.S. banks follow strict protocols: OFAC sanctions checks, IRS reporting over $10,000, and multi-factor authentication. Still, you're the first line—confirm routing numbers verbally.

Red Flags: Urgent demands, changes to wiring instructions, or unverified contacts. Report scams to FTC.gov or your bank immediately.

Practical Tips for Safe Wire Transfers

- Visit your bank in-person for first-timers to avoid errors.

- Use mobile apps from trusted banks like Chase or Bank of America for repeats.

- Keep records: Confirmations, receipts, and chats.

- For international, compare rates on Bankrate.com.

- Schedule during business hours (Fedwire runs 9 PM ET prior day to 7 PM ET).

Next Steps for Your Wire Transfer

Ready to wire? Log into your bank's app, gather recipient details, and compare fees—many offer fee waivers for premium accounts. For frequent needs, explore low-cost apps like Wise. Always prioritize security: if it feels off, walk away. With these tools, you'll handle money moves like a pro, keeping your finances secure across America.

Frequently Asked Questions

Sources & References

-

1

Wire Transfer System: Understanding Its Legal Definition — legal-resources.uslegalforms.com

- 2

-

3

What is a Wire Transfer and How Does It Work? - Tipalti — tipalti.com

- 4

- 5

-

6

What is a wire transfer and how does it work? - Citizens Bank — www.citizensbank.com

-

7

Wire Transfers: How They Work, Security & Fees - J.P. Morgan — www.jpmorgan.com

Related Articles

How to Handle "Identity Theft" in 2026: The First 24 Hours

Imagine checking your bank account on a quiet Saturday evening, only to discover unauthorized charges totaling thousands of dollars—or worse, spotting a new credit card opened in your name. In 2026, i...

The Best "Digital Banking" Apps for US Teens: A Parent's Guide

Imagine handing your teen a debit card that teaches them financial responsibility without the risk of overdrafts or debt. In 2026, digital banking apps make this possible, giving US parents powerful t...

The Best Online Banks with No Monthly Fees in 2026

Imagine ditching those pesky monthly bank fees that quietly eat into your budget every single month. In 2026, online banks make it easier than ever for Americans to enjoy truly free checking accounts...

How to Start an Emergency Fund from Scratch: $1 to $1;000

Picture this: Your car breaks down on the way to work, or an unexpected medical bill lands in your mailbox. Without a safety net, you're scrambling for credit cards or loans with sky-high interest rat...