What Is Disability Insurance and Why Is It Often Overlooked?

Imagine waking up one day unable to do the job you've trained for years to perform, your income suddenly gone due to illness or injury. For one in four 20-year-olds, this reality hits before age 67, l...

Imagine waking up one day unable to do the job you've trained for years to perform, your income suddenly gone due to illness or injury. For one in four 20-year-olds, this reality hits before age 67, leaving families scrambling to cover bills.Disability insurance steps in as a financial lifeline, replacing a portion of your lost income when you can't work—but it's surprisingly overlooked by most Americans.

This coverage isn't just for manual laborers; it protects professionals like teachers, accountants, and surgeons too. Yet, despite the odds, only about 30% of private-sector workers have access to it through employers, and far fewer buy individual policies.Why is disability insurance so often ignored? We'll break it down, explore how it works in the U.S., and share practical steps to get protected in 2026.

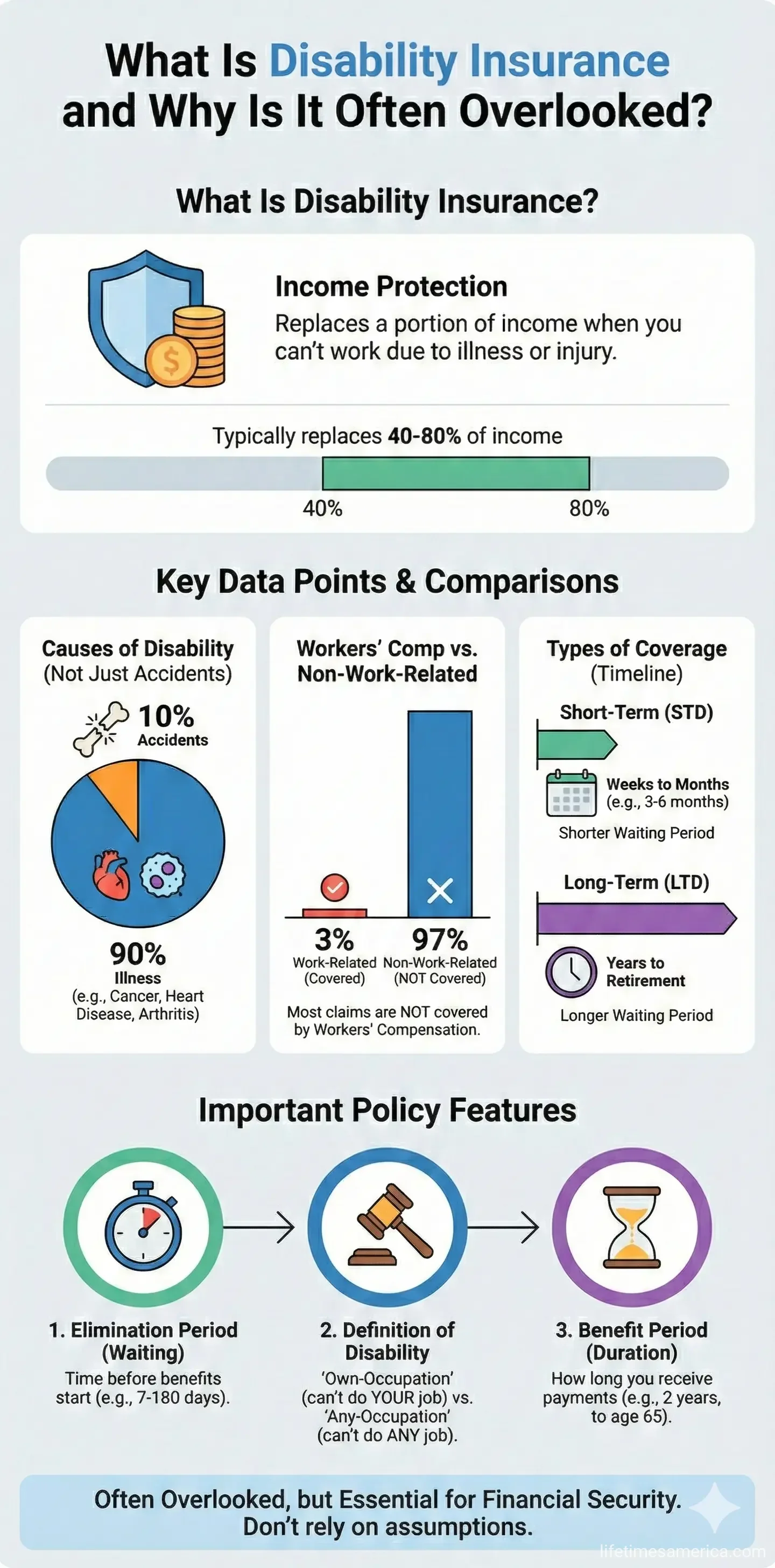

What Is Disability Insurance?

Disability insurance is a policy that pays you a monthly benefit if a sickness, injury, or medical condition—like pregnancy complications or chronic illness—prevents you from working.[3][5] It replaces 40-60% of your pre-disability income, helping cover essentials like mortgage payments, groceries, and 401(k) contributions while you recover.[3][4]

Unlike life insurance, which pays out after death, disability insurance focuses on your most valuable asset: your ability to earn.[6] Policies come in two main types: short-term and long-term, each serving different needs.

Short-Term Disability (STD) Insurance

Short-term disability kicks in after a brief waiting period (often 7-14 days) and covers temporary conditions lasting weeks to months.[2][3] Benefits typically last 3-6 months, up to two years in some cases, replacing 40-60% of your income.[3][4]

It's ideal for recovery from surgery, severe flu, or postpartum issues—but not on-the-job injuries, which fall under workers' compensation.[6] Five states mandate STD coverage: California, Hawaii, New Jersey, New York, Rhode Island, and Puerto Rico require employers to provide it via state programs or private plans.[2][6]

- California State Disability Insurance (SDI): Up to 52 weeks, 60-90% of wages (income-based).[2]

- New Jersey Temporary Disability Insurance (TDI): Up to 26 weeks, 58% of weekly wages.[2]

- Hawaii TDI: Up to 26 weeks, varies by wages.[2]

In the other 45 states, STD is voluntary, often employer-sponsored with shared premiums.[2][6]

Long-Term Disability (LTD) Insurance

Long-term disability provides extended protection for chronic or severe conditions lasting months, years, or until retirement.[3][8] Benefits start after STD ends (elimination period of 90 days to 6 months) and can pay 40-60% of income up to age 65.[3][4]

No states mandate LTD, but many employers offer group plans. Individual LTD policies give more control and portability if you change jobs.[4]

How Does Disability Insurance Work?

When you file a claim, your doctor verifies the disability. Benefits pay monthly after the waiting period, tax-free if you pay premiums with after-tax dollars.[4] Coverage applies to non-work-related issues; work injuries go through workers' comp or state programs.

Key Definitions of Disability

Policies define "disabled" in three ways, impacting eligibility:[1][4]

- Own Occupation: Can't perform your specific job (best for specialists).[1]

- Any Occupation: Can't work any job suited to your skills (stricter).[1]

- Modified Own Occupation: Own occ for first 2 years, then any occ.[1]

Group policies often use "any occupation" after two years, so review terms carefully.[1]

Government Disability Programs in the U.S.

Federal and state options supplement private insurance:

- Social Security Disability Insurance (SSDI): For severe, long-term disabilities preventing any work. Average benefit: $1,580/month in 2026. Requires work history and Social Security tax payments.[5][7]

- State Programs: Mandatory in CA, HI, NJ, NY, RI, PR for short-term needs.[2][6]

- VA Disability: For veterans with service-related conditions.[5]

These have strict rules and low benefits—SSDI approval takes months, covering just 30-40% of needs. Private insurance bridges the gap.[5]

Why Is Disability Insurance Often Overlooked?

Despite stats showing a 25% chance of disability before retirement, most Americans skip it.[4] Here's why:

- "It Won't Happen to Me": People overestimate job security and underestimate illness risks. Cancer, back injuries, and mental health issues sideline 90% of claims.[3]

- Focus on Life and Health Insurance: Life insurance gets attention for family protection, but living longer without income is scarier for many.[5]

- Employer Coverage Seems Enough: Group plans cap at 60% income replacement and aren't portable.[4]

- Cost Concerns: Premiums run 1-3% of income ($30-100/month), but cheaper than lost earnings.[3]

- Complexity: Confusing definitions and riders scare buyers off.[1]

In 2026, rising healthcare costs and hybrid work amplify risks—remote pros still need protection.[3]

Benefits of Disability Insurance for Americans

It safeguards your lifestyle:

- Maintains cash flow for IRS payments, Medicare premiums, and Medicaid eligibility if needed.

- Protects savings and retirement—no raiding 401(k)s early.

- Covers family needs during recovery.

- Offers riders like cost-of-living adjustments (COLA) or future increase options for career growth.[4]

Real U.S. Examples

A New York teacher with cancer gets 60% pay via state TDI, then LTD.[6] A California freelancer buys individual own-occ policy after group STD ends.[2] SSDI helps a Michigan worker, but private LTD covers the rest.[5]

How to Choose the Right Disability Insurance in 2026

Assess needs: Calculate 60-70% income replacement for 5+ years.

| Factor | What to Look For |

|---|---|

| Benefit Amount | 50-60% of gross income |

| Waiting Period | 90 days for LTD to align with savings/STD |

Shop individual policies from carriers like Guardian or MetLife for portability.[4][8] Use USA.gov for SSDI info and DOL.gov for state mandates.[7]

Practical Tips to Get Started

- Check employer benefits—enroll in group LTD if offered.

- Buy individual policy if self-employed or high earner.

- Opt for own-occ definition.

- Add riders: COLA, partial disability, student loan protection.

- Compare quotes via independent brokers.

- Review annually—update for salary bumps.

FAQ

1. Does disability insurance cover mental health?

Yes, conditions like depression or anxiety qualify if they prevent work, per policy terms.[3]

2. What's the difference between STD and LTD?

STD covers short gaps (weeks-months); LTD handles long-term (years).[2][4]

3. Is disability insurance tax-free?

Yes, if premiums are after-tax; employer-paid benefits may be taxable.[4]

4. Can I get disability insurance if I'm healthy?

Best time—underwriting is easier pre-existing conditions.[3]

5. How much does it cost?

1-3% of income; a $60,000 earner pays ~$20-50/month.[3]

6. Does SSDI replace private insurance?

No—it's a supplement with lower benefits and strict rules.[5][7]

Protect Your Income Today

Disability insurance isn't optional—it's essential for financial security in unpredictable times. Start by reviewing your employer plan or getting quotes for an individual policy. Visit SSA.gov for SSDI details and consult a broker for personalized advice. Take action now to avoid regret later.

Sources & References

- What is the Definition of Disability in Disability Insurance? — emgbrokerage.com

- Long Term vs Short Term Disability Insurance in the USA — footholdamerica.com

- What is Disability Insurance? 2026 Guide - Breeze — meetbreeze.com

- Disability Insurance Definitions and Terms - Guardian Life — guardianlife.com

- What is Disability Insurance and How Does It Work? — schwab.com

- Short-Term Disability vs. Long-Term Disability Insurance — paychex.com

- Who Can Get Disability — ssa.gov

- What Is Long-Term Disability Insurance? - MetLife — metlife.com

Related Articles

The Truth About Term Life vs. Whole Life Insurance

Choosing the right life insurance can feel overwhelming, but understanding the core differences between term life and whole life insurance empowers you to protect your family's future without overpayi...

The Best Term Life Insurance for Parents with Young Kids

As parents with young kids, you're juggling diapers, daycare drop-offs, and dreams for their future—all while knowing one unexpected event could upend everything. Term life insurance steps in as your...

How to Save Money on Homeowners Insurance in 2026

With home insurance premiums climbing due to inflation, climate risks, and rising rebuilding costs, American homeowners are feeling the pinch in 2026.Saving money on homeowners insurance doesn't mean...

How to Lower Your Car Insurance Premiums in 2026

Car insurance premiums have surged in recent years, with national rates jumping about 20% from 2024 to 2025 alone, leaving even safe drivers stunned by renewal notices.But in 2026, you can fight back...