Malpractice Insurance Explained: Who Needs It and What It Covers

Imagine performing life-saving surgery only to face a lawsuit years later that threatens your career and savings. That's the reality for many healthcare professionals without proper malpractice insura...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine performing life-saving surgery only to face a lawsuit years later that threatens your career and savings. That's the reality for many healthcare professionals without proper malpractice insurance. In the United States, where lawsuits are on the rise and premiums are climbing in 2026, understanding this essential coverage is crucial for doctors, nurses, and other providers.

This guide breaks down malpractice insurance explained: who needs it and what it covers, with practical tips tailored for American professionals navigating a tough liability landscape.

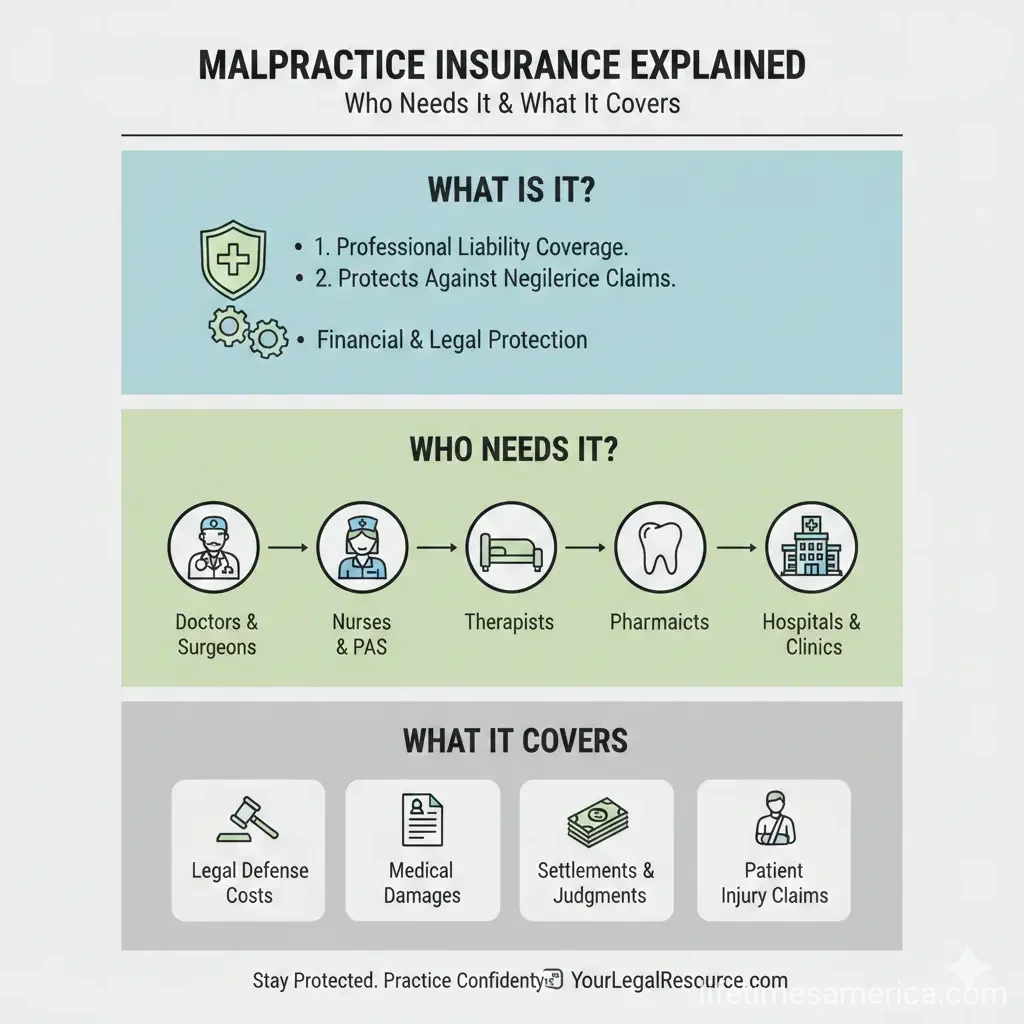

What Is Malpractice Insurance?

Medical malpractice insurance, also called professional liability insurance, protects healthcare providers from financial losses due to claims of negligence or errors in patient care. It covers legal defense costs, settlements, and judgments when patients allege harm from substandard treatment.

In 2026, this coverage is more vital than ever amid rising "nuclear verdicts"—awards exceeding $10 million—and top 50 malpractice awards averaging $56 million in 2024, up 14% from 2023. Policies typically include claims-made or occurrence coverage: claims-made responds to lawsuits filed during the policy period, while occurrence covers incidents anytime, regardless of when reported.

Key Components of a Policy

- Defense Costs: Pays attorney fees, expert witnesses, and court costs, even if the claim is baseless.

- Indemnity Limits: Caps payout for settlements or judgments, often $1 million per claim/$3 million aggregate.

- Deductibles: Amount you pay out-of-pocket before coverage kicks in; higher ones lower premiums.

- Consent-to-Settle: Requires your approval before settling a claim.

Providers must review policies for gaps, like exclusions for telemedicine or AI use, which insurers are scrutinizing more closely in 2026.

Who Needs Malpractice Insurance in the US?

Not every American needs it, but most healthcare workers do. It's often required by state laws, hospitals, or licensing boards.

Physicians and Surgeons

Doctors in high-risk specialties like surgery, OB/GYN, and anesthesia face the steepest premiums. For instance, surgical specialists can save 20-30% via RRGs (Risk Retention Groups) in 35 states, but groups of at least five physicians are typically required. Even primary care physicians need it due to rising claims from diagnostic delays.

Advanced Practice Providers (APPs)

Nurse practitioners (NPs), physician assistants (PAs), and certified registered nurse anesthetists (CRNAs) saw rate hikes in 2026 from nuclear verdicts up to $950 million in 2025. Employer coverage might suffice, but independent APPs must buy their own—prioritizing stable carriers over cheap ones to avoid insolvency risks.

Other Professionals

- Dentists, Pharmacists, Therapists: State-specific mandates apply; e.g., many require it for licensure.

- Hospitals and Clinics: Need facility policies covering vicarious liability for staff.

- Telehealth Providers: Extra endorsements needed for interstate care.

Check your state's requirements via the Federation of State Medical Boards or nursing boards. In states like Texas, tort reforms cap non-economic damages at $250,000 per physician, lowering premiums by 35% post-2003.

What Does Malpractice Insurance Cover?

Coverage kicks in for claims alleging negligence causing patient injury, like misdiagnosis, surgical errors, or medication mistakes. It pays regardless of guilt—focusing on settlement to avoid trials.

| Coverage Type | What It Includes | Typical Limits (2026) |

|---|---|---|

| Legal Defense | Attorneys, depositions, trials | Included up to policy limit |

| Settlements/Judgments | Payouts for bodily injury, wrongful death | $1M per claim / $3M aggregate |

| Non-Economic Damages | Pain/suffering (capped by state law) | Varies; e.g., CA longstanding caps |

| Exclusions | Intentional acts, criminal behavior | Not covered |

New in 2026: Some policies address AI tools and cyber risks, but disclose usage during underwriting or risk exclusions. Staffing shortages and handoff errors are common claim triggers amid reimbursement pressures.

2026 Trends Impacting Malpractice Insurance

Expect 5-15% premium increases due to claim severity and inflation. States like Colorado raised wrongful death caps to $1.575 million by 2029 (starting at $875,000 in 2025), while Montana hits $350,000 in 2026.

Reforms in Georgia curb "anchoring" (inflated damage suggestions), and South Carolina eyes joint liability tweaks. Telemedicine and regulatory changes, like federal privacy updates for substance-use records, add complexity.

How to Reduce Premiums

- Join an RRG for 12-35% savings, depending on specialty.

- Implement risk management: Board participation or quality metrics qualify for discounts.

- Shop carriers: Arizona and Pennsylvania 2026 guides show specialty-specific rates.

- Increase deductibles or add "corridor" layers to share risk.

- Advocate for reforms via AMA resources.

State Variations and Reforms

Rates vary wildly: Texas tort reforms slashed premiums via $250,000 caps and strict expert rules. California’s MICRA caps noneconomic damages, a model since the 1970s. Check state insurance departments for mandates—e.g., CMS 2026 recovery thresholds affect liability settlements.

In a "hard market," underwriting tightens, emphasizing claims history and documentation.

Next Steps to Protect Yourself

Review your policy annually for 2026 gaps in AI, telehealth, or staffing risks. Get quotes from multiple carriers, join an RRG if eligible, and track state reforms via AMA updates. Consult an insurance broker specializing in healthcare—your career depends on it. Solid coverage lets you focus on patients, not lawsuits.

Frequently Asked Questions

Sources & References

-

1

How to Reduce Medical Malpractice Insurance Costs as a Doctor 2026 — www.primewayfcu.com

- 2

-

3

Amid signs of hard market, it's time for medical liability reform — www.ama-assn.org

-

4

Seven Omens for Medical Malpractice Insurance in 2026 — homewood.insure

-

5

Medical Malpractice Trends APPs Need to Know in 2026 — www.cmfgroup.com

-

6

Predictions for U.S. Healthcare Through 2026 — www.tdcg.com

-

7

What to expect in the malpractice insurance market in 2026 — www.medicaleconomics.com

-

8

IMR 2026 – Healthcare Professional Liability — www.wtwco.com

-

9

2026 Recovery Thresholds for Certain Liability Insurance — www.cms.gov

-

10

Healthcare Liability Insurance Risks 2026 — protectusbetter.com

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...