HMO vs PPO vs EPO: Which Health Insurance Plan Should You Choose?

Choosing the right health insurance plan can feel overwhelming, especially when you're comparing HMO vs PPO vs EPO. With premiums, networks, and out-of-network coverage on the line, one wrong pick cou...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Choosing the right health insurance plan can feel overwhelming, especially when you're comparing HMO vs PPO vs EPO. With premiums, networks, and out-of-network coverage on the line, one wrong pick could cost you thousands in 2026. This guide breaks it down simply so you can select the best option for your family's needs and budget.

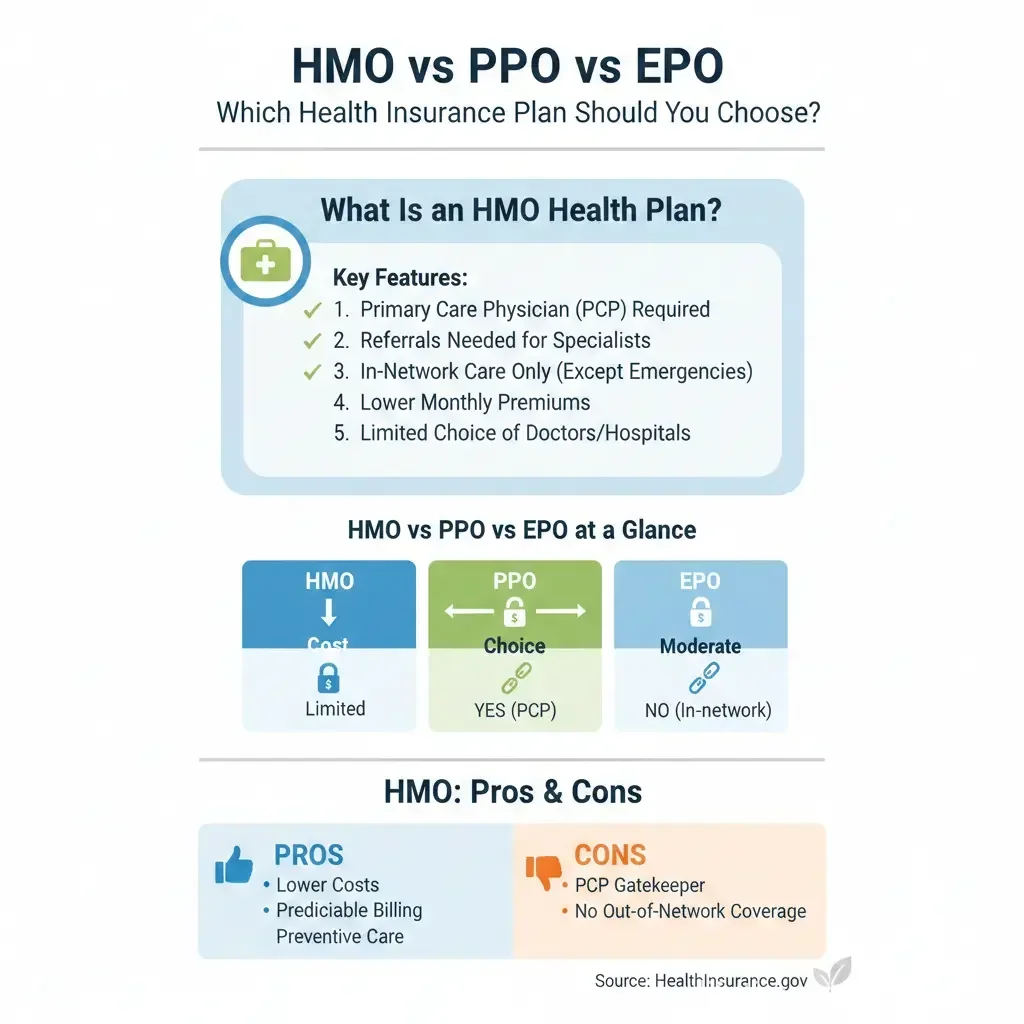

What Is an HMO Health Plan?

Health Maintenance Organizations (HMOs) emphasize coordinated care through a tight-knit network of doctors and hospitals. You'll select a primary care provider (PCP) who acts as your main point of contact, handling routine checkups and issuing referrals for specialists.

HMOs shine for their affordability. They typically offer the lowest monthly premiums and out-of-pocket costs, like copays and deductibles, because they limit care to in-network providers—except in emergencies. No out-of-network coverage means predictable expenses, ideal if you stick to local providers.

Pros and Cons of HMO Plans

- Pros: Lower premiums and copays; coordinated care reduces unnecessary tests; no deductibles in some plans, like certain CalPERS options.

- Cons: Smaller networks limit doctor choices; referrals required for specialists; not travel-friendly.

In 2026, HMOs remain popular in Medicare Advantage plans for their cost control amid rising healthcare expenses.

What Is a PPO Health Plan?

Preferred Provider Organizations (PPOs) give you the most flexibility. No PCP or referrals needed—you can see any specialist directly, in-network or out. Networks are larger, and out-of-network care is covered at higher costs, making PPOs great for travelers or those with preferred doctors outside standard networks.

The trade-off? Higher premiums, deductibles, and coinsurance. After meeting your deductible, you pay a percentage of costs, which can add up. In 2026, some insurers are shrinking PPO options due to management costs, potentially limiting choices in certain counties.

Pros and Cons of PPO Plans

- Pros: Broad access to providers; no referrals; nationwide options like PERS Platinum.

- Cons: Highest costs; higher out-of-pocket for out-of-network care; deductibles and coinsurance apply.

What Is an EPO Health Plan?

Exclusive Provider Organizations (EPOs) strike a middle ground. They use a network larger than HMOs but smaller than PPOs, covering only in-network care (emergencies excepted). No referrals or PCP required in most cases, offering specialist access without gatekeepers.

Premiums fall between HMOs and PPOs—more affordable than PPOs but higher than HMOs—balancing cost and choice. EPOs suit those whose doctors are in-network but who want HMO-like savings without referrals.

Pros and Cons of EPO Plans

- Pros: Lower costs than PPOs; direct specialist access; larger networks than HMOs.

- Cons: No out-of-network coverage; network still restricted.

HMO vs PPO vs EPO: Side-by-Side Comparison

Here's a quick table to compare key features based on 2026 standards:

| Feature | HMO | PPO | EPO |

|---|---|---|---|

| Network Size | Smallest | Largest | Mid-sized (larger than HMO) |

| PCP Required | Yes | No | Usually No |

| Referrals for Specialists | Yes | No | No |

| Out-of-Network Coverage | No (emergencies only) | Yes, higher cost | No (emergencies only) |

| Monthly Premiums | Lowest | Highest | Mid-range |

| Out-of-Pocket Costs | Lowest | Highest | Mid-range |

Data synthesized from major providers.

Cost Breakdown: Which Plan Saves You Money in 2026?

Costs vary by location, age, and insurer, but patterns hold. HMOs average the lowest premiums—often 20-30% less than PPOs—due to restricted networks. EPOs save 10-20% over PPOs while offering more freedom.

Factor in total costs: A healthy family might thrive on an HMO's low copays. Frequent travelers or those needing specialists prefer PPOs despite deductibles up to $2,000+ per person. Use the ACA Marketplace at HealthCare.gov to compare personalized quotes during Open Enrollment (November 1, 2025 - January 15, 2026).

2026 Trends Impacting Costs

- Shrinking PPO networks and fewer options in some areas.

- HMOs gaining traction for predictable Medicare Advantage coverage.

- Inflation pushing overall premiums up 5-7%, per industry forecasts.

Who Should Choose HMO, PPO, or EPO?

Pick HMO If:

- You're budget-conscious and healthy with few doctor visits.

- You live near quality in-network providers.

- You want coordinated care, like families or those with chronic conditions.

Pick PPO If:

- You travel often or value flexibility above all.

- Your preferred doctors aren't in narrower networks.

- You're okay with higher premiums for peace of mind.

Pick EPO If:

- You want HMO savings without referrals.

- Your doctors are in a mid-sized network.

- Avoiding out-of-network needs but seeking balance.

Check networks first: Use insurer tools or HealthCare.gov to verify your doctors.

Practical Tips for Choosing Your 2026 Plan

- Review your network: Ensure specialists and hospitals are included—switching doctors mid-year disrupts care.

- Estimate usage: High utilizers benefit from low HMO copays; low utilizers might save with high-deductible PPOs paired with an HSA.

- Factor taxes: HSAs offer triple tax advantages for self-employed Americans (contributions deductible, growth tax-free, qualified withdrawals tax-free).

- Shop the Marketplace: Subsidies via the Affordable Care Act cap premiums at 8.5% of income for many.

- Appeal if needed: All plans allow internal and external appeals under federal law.

Next Steps: Secure Your Coverage Today

Don't delay—log into HealthCare.gov or contact your employer for 2026 plan details. List your top doctors, estimate annual visits, and run quotes for HMO, PPO, and EPO options. Consult a licensed broker for free advice tailored to your state. The right choice saves money and stress, keeping your family protected.

Frequently Asked Questions

Sources & References

-

1

HMO vs. PPO vs. EPO: Which Health Insurance Plan Is Right for You? — differencecard.com — www.differencecard.com

- 2

- 3

- 4

-

5

HMO, PPO, and EPO: What's the Difference and Why Does It Matter? — news.calpers.ca.gov — news.calpers.ca.gov

- 6

-

7

PPO, EPO or HMO? Your Health Plan Choices Explained — primarycareins.com — primarycareins.com

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...