Understanding Social Security: When is the Best Age to Claim?

Imagine standing at a crossroads in your retirement journey, with one path offering immediate cash flow but smaller checks, and another promising larger monthly payments if you wait. Deciding when to...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine standing at a crossroads in your retirement journey, with one path offering immediate cash flow but smaller checks, and another promising larger monthly payments if you wait. Deciding when to claim Social Security benefits is one of the biggest financial choices you'll make, potentially affecting your income for decades. With Full Retirement Age (FRA) now at 67 for those born in 1960 or later, understanding your options in 2026 is crucial for maximizing your benefits.

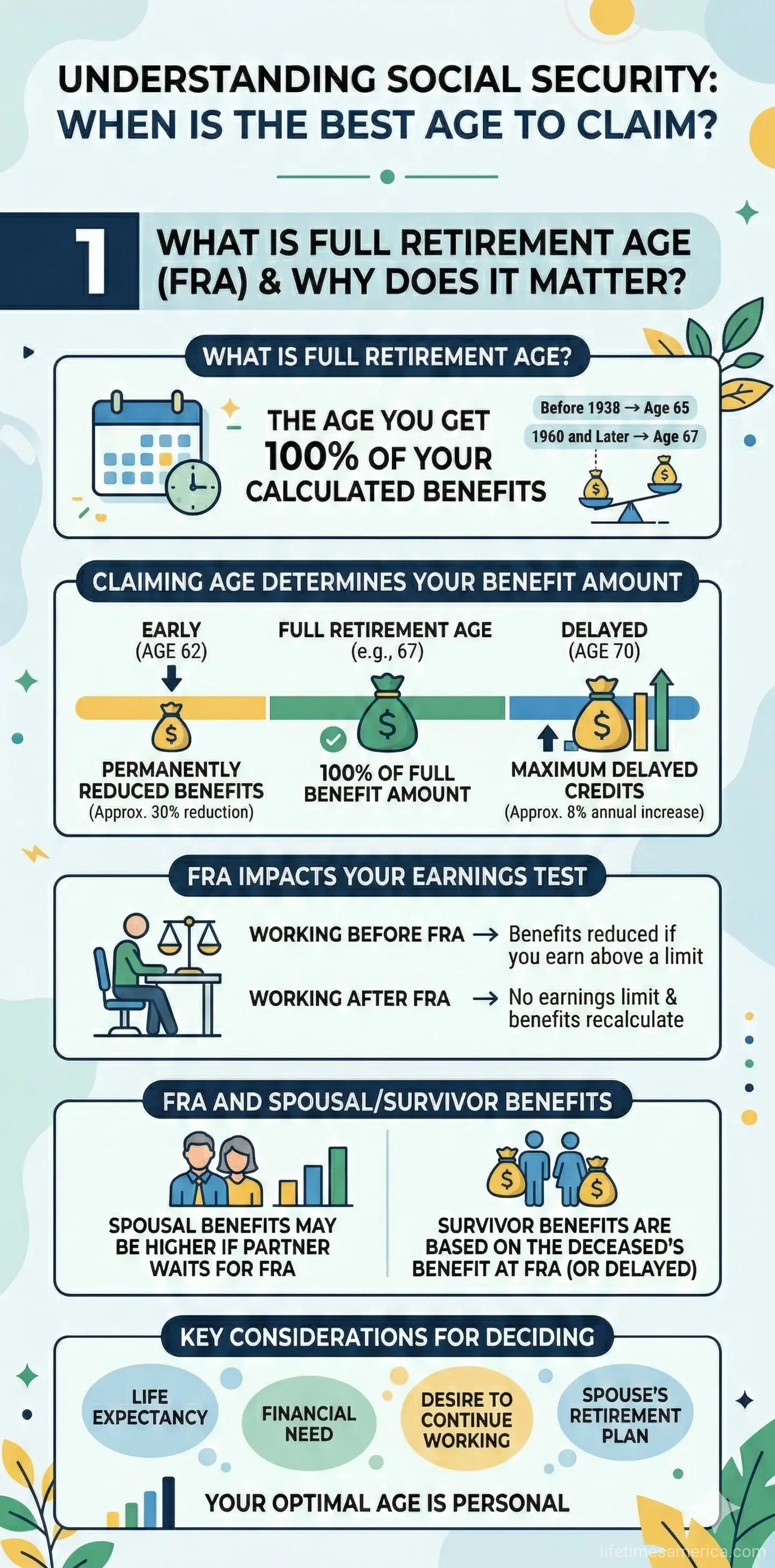

What is Full Retirement Age and Why Does it Matter?

Full Retirement Age (FRA) is the point when you qualify for 100% of your calculated Social Security retirement benefit. It's not a one-size-fits-all number—it depends on your birth year, thanks to changes from the 1983 Social Security Amendments designed to account for longer life expectancies.

FRA by Birth Year in 2026

For Americans turning 62 in 2026 (born in 1964), your FRA is 67. If you were born in 1960 or later, expect FRA at 67. Earlier birth years have slightly lower ages:

- Born 1943-1954: 66

- Born 1955: 66 and 2 months

- Born 1956: 66 and 4 months

- Born 1957: 66 and 6 months

- Born 1958: 66 and 8 months

- Born 1959: 66 and 10 months

- Born 1960 or later: 67

Note: If you're born on January 1, use the previous year's rules. Medicare eligibility stays at 65, regardless of FRA.

Knowing your FRA is step one. It serves as the baseline for reductions if you claim early or credits if you delay.

Options for Claiming Social Security: Early, On Time, or Delayed

You can start benefits as early as 62, at FRA for full amount, or delay up to 70 for maximum payments. Each choice has trade-offs based on your health, lifespan expectations, and financial needs.

Claiming at Age 62: Pros and Cons

Starting at 62 gives you payments sooner, ideal if you need income now or have health concerns limiting your life expectancy. However, your benefit drops permanently—about 30% less than at FRA of 67 for those born 1960 or later.

The reduction is 5/9 of 1% per month for the first 36 months before FRA, and 5/12 of 1% beyond that. For example, claiming 60 months early (at 62 for FRA 67) means roughly a 30% cut.

- Pro: More years of payments; up to five extra years of income.

- Con: Smaller monthly checks forever, impacting survivor benefits for your spouse.

Waiting Until Full Retirement Age

Claim at FRA (67 for most in 2026) for your full Primary Insurance Amount (PIA)—no reductions, no delays. This balances steady income without penalties.

If you're still working, watch the earnings test: In 2026, if under FRA all year, earnings over $24,480 reduce benefits $1 for every $2 earned. For those reaching FRA in 2026, the limit is $65,160 before FRA months ($1 withheld for every $3 over). Benefits aren't lost—they're recalculated higher later.

Delaying Past FRA to Age 70: The Highest Payout

Delaying earns Delayed Retirement Credits (DRCs): 8% simple increase per year (2/3% per month) from FRA to 70. For FRA 67, waiting to 70 boosts your benefit by 24%.

This maximizes lifetime income if you live past average expectancy (around 84 for men, 87 for women). It also provides stronger survivor benefits. But no payments during the wait, so you'll need other savings like 401(k)s or IRAs.

2026 Updates: What’s New for Social Security Claiming?

The Social Security Administration announced a 2.8% Cost-of-Living Adjustment (COLA) for 2026, up from 2.5% in 2025, boosting benefits for nearly 71 million recipients starting January. Maximum benefit at FRA rises to $4,152 monthly.

FRA solidifies at 67 for 1960+ births, with earnings limits adjusted: $24,480 (under FRA) and $65,160 (reaching FRA). These tweaks help stretch benefits amid inflation, but plan for Medicare Part B premiums rising too—they could eat into 32% of your COLA.

Factors to Consider: Is There a 'Best' Age for You?

No universal best age—it's personal. Run projections using the SSA's online tools.

Health and Longevity

If family history or health suggests shorter lifespan, claim early. Expecting to live to 85+? Delay to 70. Break-even analysis: Claiming at 62 vs. 70 often evens out around age 80.

Financial Situation

Got a pension, spouse's income, or robust 401(k)? Delay. Need cash for debts or healthcare? Go early. Taxes matter: Up to 85% of benefits taxable if combined income exceeds $25,000 (single) or $32,000 (joint). Coordinate with IRS rules.

Working While Claiming

Post-62 work? Earnings test applies pre-FRA. At FRA+, unlimited earnings. For federal employees or FERS, factor TSP withdrawals.

Spousal and Survivor Benefits

Married? Coordinate claims—non-working spouse may get up to 50% of your FRA benefit. Delaying your claim maximizes their survivor benefit (100% of yours).

Practical Tools and Steps to Plan Your Claim

- Create a my Social Security account at ssa.gov—view your estimated benefits by age.

- Use SSA's Quick Calculator or detailed planners for personalized scenarios.

- Consult a financial advisor for tax/estate integration.

- Apply online 3 months before desired start—quickest method.

- Time claims for January to lock in higher COLA base.

Avoid irreversible mistakes: Once claimed early, you can't switch without limited do-overs.

Frequently Asked Questions

Related Articles

The Best States for "Tax-Free" Retirement Income in 2026

Imagine waking up in your dream retirement spot, sipping coffee on a sunny porch, knowing your hard-earned Social Security checks, pensions, and 401(k) withdrawals won't get hit with state income taxe...

How to Use your 401(k) to Buy Your First House: The Hidden Risks

Picture this: You've scrimped and saved for years, eyeing that perfect starter home in your neighborhood. But the down payment feels like an insurmountable hurdle. In a pinch, your 401(k) balance star...

The Hidden Fees of 401(k) Plans: How to Save $100k over 30 Years

Imagine discovering that tiny, unnoticed fees in your 401(k) are quietly siphoning away enough money to buy a vacation home or fund a comfortable retirement. Over 30 years, cutting just 1% in hidden f...

The Best "Self-Directed" IRA Platforms for Real Estate and Private Equity

Imagine unlocking the full potential of your retirement savings by investing in rental properties, private equity deals, or even startups—all tax-deferred or tax-free within a self-directed IRA. For A...