How Much Does Car Insurance Cost in the USA?

Car insurance is one of those unavoidable expenses that can make or break your monthly budget, especially when rates seem to climb faster than gas prices. If you're wondering how much does car insuran...

The Lifetimes America editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes America readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Car insurance is one of those unavoidable expenses that can make or break your monthly budget, especially when rates seem to climb faster than gas prices. If you're wondering how much does car insurance cost in the USA, the short answer is it varies widely—but the national average for full coverage in 2026 sits around $2,297 per year, or about $191 monthly. Whether you're a new driver in California or a seasoned commuter in Ohio, understanding these costs empowers you to shop smarter and save hundreds.

In this guide, we'll break down the latest 2026 figures, explore what drives up your premium, and share practical tips tailored for American drivers. From state-by-state breakdowns to bundling hacks, you'll walk away ready to get the best deal without skimping on protection.

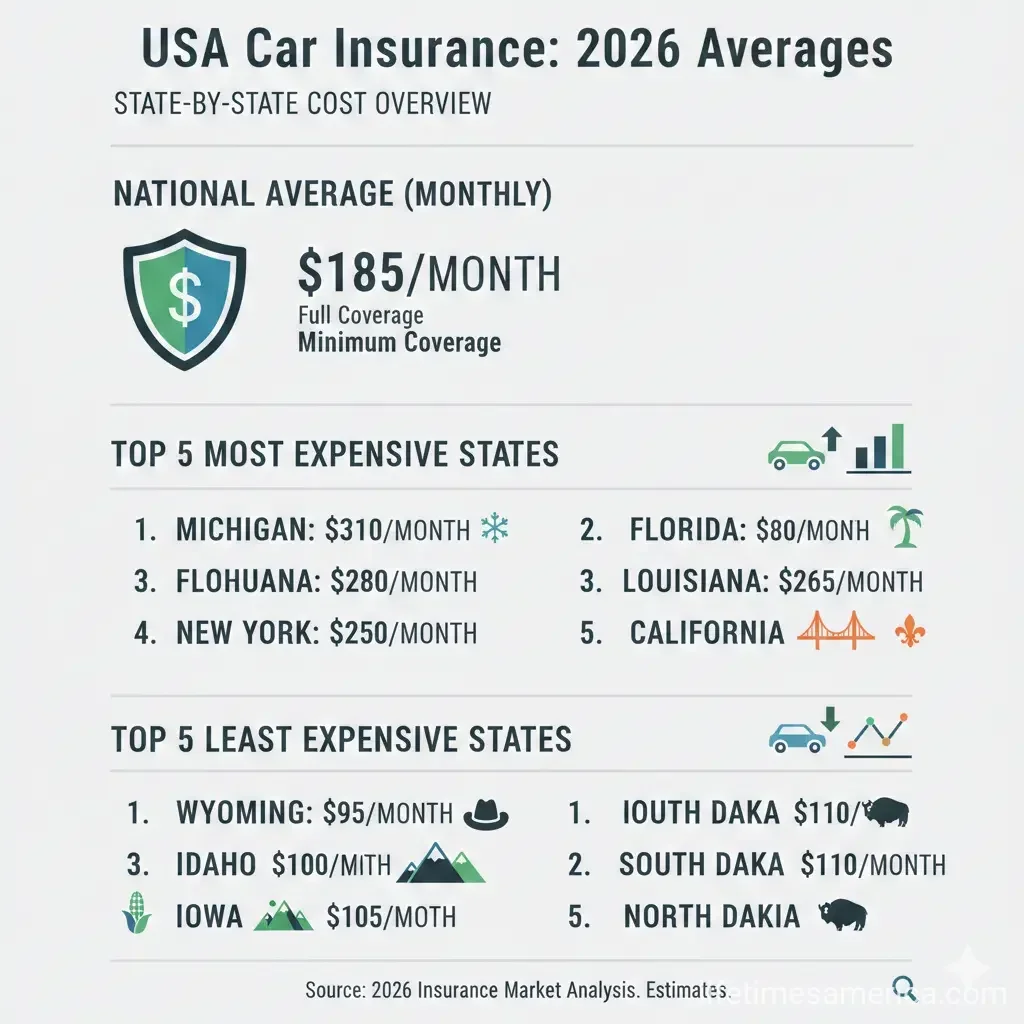

Average Car Insurance Costs Across the USA in 2026

The cost of car insurance isn't one-size-fits-all—it's shaped by everything from your zip code to your driving record. Nationally, full coverage policies (including liability, collision, and comprehensive) average $2,297 annually as of January 2026, down slightly from peaks in recent years thanks to stabilizing claims and competition among insurers. Minimum coverage, which meets state legal requirements, runs much cheaper at about $912 yearly or $76 monthly.

Here's a snapshot of how top carriers stack up for average full coverage policies:

| Carrier | Annual Cost | Monthly Cost |

|---|---|---|

| Travelers | $1,793 | $149 |

| Nationwide | $2,249 | $187 |

| Liberty Mutual | $2,297 | $191 |

| Root | $2,524 | $210 |

| Mercury | $2,614 | $218 |

Note: These are quote averages, not final premiums, and can vary based on personal factors. Recent trends show full coverage costs dipping by about $6 since late 2025, a welcome relief amid rising repair costs for tech-heavy vehicles.

Car Insurance Costs by State

Your state plays a huge role due to local laws, accident rates, theft stats, and road conditions. For instance, drivers in low-density states like Ohio pay just $1,842 yearly for full coverage—one of the cheapest—thanks to rural roads and lower traffic. High-risk spots like Florida or Michigan often exceed $3,000 annually.

Key 2026 examples:

- Alabama: $2,155/year—slightly below national average, aided by low living costs despite weather risks.

- Arizona: $2,644/year—2% under average, with middling roads and living expenses.

- Delaware: 10% above average, hit by poor highways and density.

- Oklahoma: Near national average, balanced by low density but offset by fatal crashes.

- Oregon: $2,121/year—21% below average, thanks to mild weather and good roads.

Check your state's minimum requirements via your DMV or usa.gov for exact liability limits—every state mandates at least some coverage, but amounts differ (e.g., 25/50/25 in many places).

Factors That Determine Your Car Insurance Rates

Insurers use a complex formula blending your profile with broader data. Here's what impacts how much does car insurance cost in the USA for you:

Your Personal Profile

- Age and Experience: New drivers pay more due to higher risk—rates drop as you build a clean record.

- Driving History: Tickets, accidents, or DUIs can spike premiums 20-50% or more.

- Credit Score: In most states, better credit means lower rates (banned in California, Hawaii, Massachusetts).

- Location: Urban areas with theft or congestion (e.g., Los Angeles) cost more than rural spots.

Your Vehicle and Coverage Choices

Sports cars or EVs with pricey sensors like radar for safety features drive up costs—think $200+ monthly extras. Opt for minimum coverage on older cars if repairs exceed value, but keep full if financing.

Popular models like the Toyota RAV4 average $1,750/year with State Farm, showing vehicle choice matters.

How to Save Money on Car Insurance in 2026

You don't have to accept average rates—shop around, as carriers' formulas differ based on overhead and risk appetite. Aim to compare quotes from at least three providers annually.

Practical Tips for American Drivers

- Bundle Policies: Pair with homeowners or renters for 10-25% off—check your current insurer first.

- Usage-Based Discounts: Apps or plugs tracking safe habits (no phone, steady braking) can cut 20-40%.

- Increase Deductibles: Bump from $500 to $1,000 to lower premiums, if you can cover out-of-pocket.

- Discounts for Good Behavior: Defensive driving courses (often online, $20-50) qualify you for savings in most states.

- Pay Annually: Avoid monthly fees; some offer 5-10% off upfront.

- Drop Unneeded Coverage: Skip collision on paid-off beaters worth under $4,000.

For leases or loans, lenders require full coverage—don't risk repossession. Use tools from the NAIC (naic.org) to verify insurer ratings.

Understanding Coverage Types: Minimum vs. Full

State laws set minimums (e.g., bodily injury/property damage liability), but full adds collision (your fault accidents) and comprehensive (theft, weather). Minimum saves cash short-term but leaves you exposed—consider UM/UIM for uninsured drivers, common on U.S. roads.

Next Steps to Lower Your Rates Today

Grab quotes from Travelers, State Farm, or bundlers like Progressive—input your details for personalized numbers. Review your policy against state minimums at your DMV site, enroll in a safe driving program, and track habits via an app. With rates stabilizing in 2026, now's the time to save big. Drive safe, and keep more green in your wallet.

Frequently Asked Questions

Sources & References

-

1

Average Cost of Car Insurance in the US for 2026 - Experian — www.experian.com

-

2

Car Insurance Rates by State for 2026 | Bankrate — www.bankrate.com

-

3

Average Cost of Car Insurance Falls - Kelley Blue Book — www.kbb.com

-

4

How Much Does Car Insurance Cost in 2026? - Lemonade — www.lemonade.com

-

5

Car insurance estimate by model 2026 - Insure.com — www.insure.com

Related Articles

The Best "Business Insurance" for E-commerce Sellers in 2026

Running an e-commerce business in 2026 means thriving amid booming online sales, but it also exposes you to unique risks like data breaches, product defects, and shipping mishaps. The best business in...

How to Use "Universal Life" Insurance for Executive Bonus Plans

Imagine rewarding your top executive with a benefit that protects their family, builds retirement wealth, and costs your business next to nothing after taxes. That's the power of using universal life...

How to Use "Infinite Banking" to Buy Your Next Car

Tired of watching your hard-earned money disappear when you buy a car? There's a financial strategy that's gaining traction among savvy Americans who want to keep more money in their own pockets. It's...

How to Use "Life Settlements" to Sell Your Life Insurance for Cash

Imagine holding a life insurance policy that's become more burden than benefit—premiums eating into your retirement savings, or changed family needs making the death benefit unnecessary. A life settle...